Solta vs InMode: Navigating Cyclical Headwinds and Strategic Moats in the Aesthetics Duopoly

Date : 2026-03-11

Reading : 114

As the global medical aesthetics sector navigates macroeconomic friction and shifting consumer credit environments in 2025, a structural divergence is emerging between industry heavyweights Solta Medical (a Bausch Health company) and InMode. While both manufacturers leverage stringent regulatory approvals as competitive moats, their distinct revenue models and capital allocation efficiencies dictate contrasting trajectories for 2026.

HDIN Research provides a comparative analysis of how these aesthetic giants are fortifying their sector positioning against macroeconomic volatility, highlighting the strategic implications behind their recent financial data.

Figure SOLTA MEDICAL VS INMODE: 2026 STRATEGIC BRIEFING

Strategic Moats and Revenue Resilience

Strategic Moats and Revenue Resilience

The divergence in revenue durability between the two firms highlights the strategic premium of recurring revenue in a high-interest-rate environment.

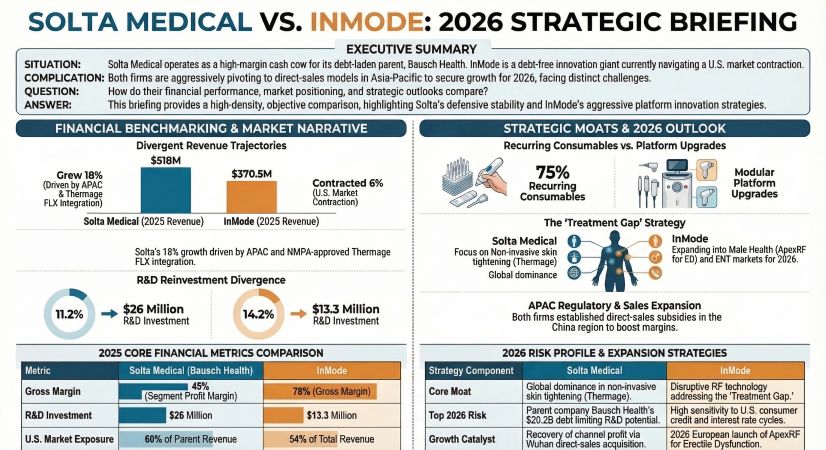

Solta Medical operates a highly defensive "razor-and-blade" model, with over 75% of its historical revenue derived from consumables. This structural stickiness successfully hedges against the cyclicality of capital equipment sales, generating a robust 45% profit margin ($232 million) in 2025. The brand's defensibility was further cemented by the January 2024 NMPA medical device approval for Thermage FLX in China, clearing the path for aggressive, compliant expansion.

Conversely, InMode’s revenue mix is heavily skewed toward capital equipment, which accounted for approximately 78% of its 2025 revenue. Because aesthetic procedures are largely out-of-pocket, this reliance on big-ticket platform sales exposes InMode to consumer down-trading and elevated financing costs. However, InMode’s strategic moat lies in its modular, "plug-and-play" architecture. By allowing physicians to upgrade capabilities via new handpieces rather than purchasing entirely new systems, InMode lowers the barrier to entry and drives cross-selling within its global installed base of nearly 30,900 platforms.

The Pivot to Direct Sales and APAC Expansion

To offset North American market saturation and reclaim channel margins, both companies executed aggressive strategic pivots toward direct distribution in the Asia-Pacific (APAC) region in 2025.

Solta executed a masterstroke in vertical integration by acquiring its Chinese full-service distributor, Wuhan Shibo Zhenmei Technology, in December 2025. By absorbing the distribution tier, Solta reclaims full control over marketing, channel margins, and inventory management for its Thermage FLX line.

Similarly, InMode is accelerating its direct sales capabilities in Asia via its Guangzhou subsidiary. This pivot to direct channels in APAC is a critical compensation mechanism for InMode, serving to offset severe cyclical headwinds in its primary U.S. market, where revenue contracted sharply from $245 million to $199 million in 2025.

Capital Allocation Efficiency and Macro Risks

A deeper look into the balance sheets reveals starkly different capital allocation strategies dictated by corporate structures.

Despite operating as a cash cow, Solta’s R&D reinvestment rate is artificially capped (estimated at 11.2% internally) due to the immense financial strain of its parent company, Bausch Health. Burdened by over $20.2 billion in corporate debt and $1.6 billion in 2025 interest expenses, Bausch’s mandate to deleverage restricts Solta’s capacity for disruptive M&A. Furthermore, Bausch faces a looming $1.4 billion goodwill impairment in Q1 2026, creating a defensive corporate posture that limits Solta's capital flexibility.

InMode presents the exact opposite financial profile. Maintaining a pristine, near-zero debt balance sheet, InMode has prioritized returning capital to shareholders, executing aggressive stock buybacks totaling $285 million in 2024 and $127 million in 2025. While this optimizes the capital structure, InMode's R&D expenditure—while proportionally higher at 14.2% of net income—indicates a conservative approach to massive capital expenditures (CAPEX), capped at just $1 million for 2026.

2026 Industry Outlook: Innovation vs. Integration

Looking toward 2026, the growth blueprints of both firms diverge based on their respective sector positioning. Solta’s primary growth catalyst will be the operational integration of its newly acquired Chinese direct-sales network and the global commercialization of Fraxel FTX.

InMode, recognizing the ceiling of pure dermatological aesthetics, is executing a cross-disciplinary expansion strategy. The company is actively penetrating the men's health and urology sectors with the planned 2026 European launch of ApexRF—a non-invasive device targeting erectile dysfunction (ED). Coupled with the rollout of upgraded platforms like OptimasMAX and Solaria, InMode is systematically expanding its total addressable market into ENT, ophthalmology, and general practice to insulate itself from pure-play aesthetic volatility.

HDIN Viewpoint

HDIN Research assesses that the 2026 medical aesthetics landscape will disproportionately reward business models with high revenue durability over pure installed-base growth. Solta’s structural advantage in consumable stickiness, paired with its vertical integration in the highly regulated Chinese market, provides superior earnings visibility. However, its parent-level financial distress poses a latent risk to long-term disruptive innovation.

InMode’s nimble cost structure and aggressive diversification into therapeutic indications demonstrate high strategic agility. Yet, its near-term valuation remains tethered to the cyclical recovery of North American capital equipment spending. For institutional investors and market entrants, the core calculus rests on weighing Solta's structural debt drag against InMode's macro-cyclical exposure.

Get Presentation & Video

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

HDIN Research provides a comparative analysis of how these aesthetic giants are fortifying their sector positioning against macroeconomic volatility, highlighting the strategic implications behind their recent financial data.

Figure SOLTA MEDICAL VS INMODE: 2026 STRATEGIC BRIEFING

Strategic Moats and Revenue ResilienceThe divergence in revenue durability between the two firms highlights the strategic premium of recurring revenue in a high-interest-rate environment.

Solta Medical operates a highly defensive "razor-and-blade" model, with over 75% of its historical revenue derived from consumables. This structural stickiness successfully hedges against the cyclicality of capital equipment sales, generating a robust 45% profit margin ($232 million) in 2025. The brand's defensibility was further cemented by the January 2024 NMPA medical device approval for Thermage FLX in China, clearing the path for aggressive, compliant expansion.

Conversely, InMode’s revenue mix is heavily skewed toward capital equipment, which accounted for approximately 78% of its 2025 revenue. Because aesthetic procedures are largely out-of-pocket, this reliance on big-ticket platform sales exposes InMode to consumer down-trading and elevated financing costs. However, InMode’s strategic moat lies in its modular, "plug-and-play" architecture. By allowing physicians to upgrade capabilities via new handpieces rather than purchasing entirely new systems, InMode lowers the barrier to entry and drives cross-selling within its global installed base of nearly 30,900 platforms.

The Pivot to Direct Sales and APAC Expansion

To offset North American market saturation and reclaim channel margins, both companies executed aggressive strategic pivots toward direct distribution in the Asia-Pacific (APAC) region in 2025.

Solta executed a masterstroke in vertical integration by acquiring its Chinese full-service distributor, Wuhan Shibo Zhenmei Technology, in December 2025. By absorbing the distribution tier, Solta reclaims full control over marketing, channel margins, and inventory management for its Thermage FLX line.

Similarly, InMode is accelerating its direct sales capabilities in Asia via its Guangzhou subsidiary. This pivot to direct channels in APAC is a critical compensation mechanism for InMode, serving to offset severe cyclical headwinds in its primary U.S. market, where revenue contracted sharply from $245 million to $199 million in 2025.

Capital Allocation Efficiency and Macro Risks

A deeper look into the balance sheets reveals starkly different capital allocation strategies dictated by corporate structures.

Despite operating as a cash cow, Solta’s R&D reinvestment rate is artificially capped (estimated at 11.2% internally) due to the immense financial strain of its parent company, Bausch Health. Burdened by over $20.2 billion in corporate debt and $1.6 billion in 2025 interest expenses, Bausch’s mandate to deleverage restricts Solta’s capacity for disruptive M&A. Furthermore, Bausch faces a looming $1.4 billion goodwill impairment in Q1 2026, creating a defensive corporate posture that limits Solta's capital flexibility.

InMode presents the exact opposite financial profile. Maintaining a pristine, near-zero debt balance sheet, InMode has prioritized returning capital to shareholders, executing aggressive stock buybacks totaling $285 million in 2024 and $127 million in 2025. While this optimizes the capital structure, InMode's R&D expenditure—while proportionally higher at 14.2% of net income—indicates a conservative approach to massive capital expenditures (CAPEX), capped at just $1 million for 2026.

2026 Industry Outlook: Innovation vs. Integration

Looking toward 2026, the growth blueprints of both firms diverge based on their respective sector positioning. Solta’s primary growth catalyst will be the operational integration of its newly acquired Chinese direct-sales network and the global commercialization of Fraxel FTX.

InMode, recognizing the ceiling of pure dermatological aesthetics, is executing a cross-disciplinary expansion strategy. The company is actively penetrating the men's health and urology sectors with the planned 2026 European launch of ApexRF—a non-invasive device targeting erectile dysfunction (ED). Coupled with the rollout of upgraded platforms like OptimasMAX and Solaria, InMode is systematically expanding its total addressable market into ENT, ophthalmology, and general practice to insulate itself from pure-play aesthetic volatility.

HDIN Viewpoint

HDIN Research assesses that the 2026 medical aesthetics landscape will disproportionately reward business models with high revenue durability over pure installed-base growth. Solta’s structural advantage in consumable stickiness, paired with its vertical integration in the highly regulated Chinese market, provides superior earnings visibility. However, its parent-level financial distress poses a latent risk to long-term disruptive innovation.

InMode’s nimble cost structure and aggressive diversification into therapeutic indications demonstrate high strategic agility. Yet, its near-term valuation remains tethered to the cyclical recovery of North American capital equipment spending. For institutional investors and market entrants, the core calculus rests on weighing Solta's structural debt drag against InMode's macro-cyclical exposure.

Get Presentation & Video

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com