Auddia Inc. 2025 Strategic Analysis: Navigating the B2B SaaS Pivot Amid Severe Liquidity Constraints

Date : 2026-03-13

Reading : 172

Auddia Inc. is currently navigating an extreme corporate inflection point characterized by a complete structural overhaul. Based on a penetrative analysis of the company's 2025 Form 10-K, HDIN Research reveals an enterprise caught in a precarious revenue vacuum. While the company is orchestrating a highly logical strategic pivot from a capital-intensive B2C subscription model to a B2B SaaS framework, this transition is fundamentally overshadowed by existential liquidity headwinds, severe equity dilution risks, and heavy reliance on an impending related-party merger.

Figure Auddia Inc 2025 Strategic Overview: Pivot, Merger, and Financial Risk

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

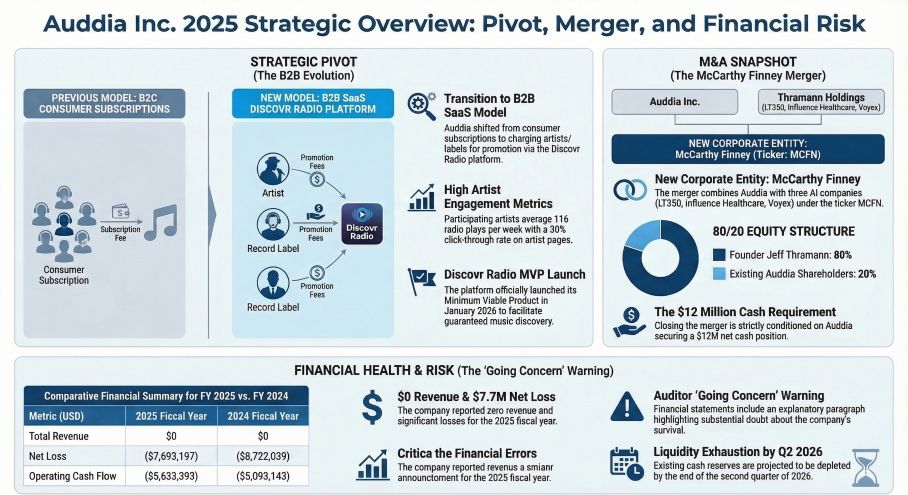

Auddia’s 2025 financial posture exhibits the classic distress signals of an early-stage, asset-light R&D entity undergoing a deep transition. The company reported zero revenue for both the 2024 and 2025 fiscal years, highlighting a commercialization vacuum as it abandons its legacy platforms.

While the net loss narrowed by 11.8% year-over-year to $7.69 million—driven primarily by a 27.4% reduction in General & Administrative (G&A) expenses—this optical improvement masks underlying cash burn realities. Operating cash flow (OCF) outflows widened by 10.6% to $5.63 million. With only $3.18 million in cash equivalents at the close of 2025 and an estimated monthly burn rate of $470,000, capital allocation efficiency is critically strained. The "So What" here is unequivocal: independent auditors have issued a "going concern" warning, projecting that current liquidity will only sustain operations through the second quarter of 2026 without aggressive, highly dilutive external financing.

Strategic Pivots: Reshaping CAC and LTV via "Discovr Radio"

Operationally, Auddia’s strategic pivot is a calculated attempt to fundamentally alter its Customer Acquisition Cost (CAC) and Lifetime Value (LTV) profiles. Recognizing the prohibitive costs of competing with streaming giants for consumer subscriptions, management has repositioned its core AI technology toward a B2B SaaS model named *Discovr Radio*.

This model targets independent artists and record labels, offering them "guaranteed plays" by seamlessly injecting their tracks into the ad-breaks of traditional AM/FM radio streams via the proprietary *faidr* app. By transitioning the consumer-facing app to a free model, Auddia aims to drastically lower CAC to build an expansive "listener pool." Simultaneously, it captures higher-margin, sticky recurring revenue from B2B clients. Early pilot metrics are promising—yielding an average of 116 weekly plays per artist and an exceptional 30% Click-Through Rate (CTR) on artist pages—yet these remain unproven at a macroeconomic scale.

Strategic Moats and Technological Execution Risks

Auddia’s strategic moat is anchored in its edge-computing AI architecture, built on Google TensorFlow. The technology enables real-time, distributed inference on consumer devices to identify and time-shift audio segments (ads, DJ talks, music). Holding critical patents for the seamless integration of broadcast and streaming audio, the company possesses a moderate-to-high technical barrier to entry.

However, the sector positioning is fraught with execution and legal risks. The foundational legality of caching and replacing broadcast content relies heavily on the "Fair Use" doctrine (specifically time-shifting precedents). Any adverse regulatory shifts in statutory royalty rates or copyright interpretations could instantly neutralize this technological moat. Furthermore, operating with an asset-light workforce of just five full-time employees and heavy reliance on outsourced IT, the company's ability to maintain enterprise-grade SLA (Service Level Agreement) standards for its upcoming SaaS clients remains structurally questionable.

Sector Positioning & The High-Leverage Restructuring

The most critical variable in Auddia’s survival equation is its proposed merger with Thramann Holdings, an entity controlled by Auddia’s recently reinstated CEO, Jeff Thramann. The transaction aims to consolidate three AI-native early-stage companies under a new ticker, McCarthy Finney (MCFN).

Strategically, this associated party M&A is designed to generate AI scale and cross-platform synergies. Financially, it represents a massive dilution event. Existing Auddia shareholders will be compressed to a mere 20% economic interest in the new entity. More alarmingly, the merger is contingent upon Auddia securing $12 million in net cash at closing. This creates a systemic financing dependency, forcing the company to heavily leverage ATM facilities and convertible instruments, thereby triggering aggressive anti-dilution downward spirals for current equity holders.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Auddia as an enterprise in a financial "ICU" state. The strategic clarity of the B2B SaaS pivot is commendable—effectively addressing the systemic exposure problem for independent artists within the 62% of U.S. audio consumption still dominated by traditional radio.

However, the disparity between strategic vision and balance sheet reality is stark. The zero-revenue baseline, combined with the stringent $12 million capital requirement to close the survival-critical McCarthy Finney merger, creates an asymmetric risk profile. The company's future does not currently hinge on its AI algorithmic supremacy, but rather on its immediate capacity to execute highly dilutive capital market maneuvers before the Q2 2026 liquidity cliff.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Auddia Inc 2025 Strategic Overview: Pivot, Merger, and Financial Risk

Financial Health & Capital Allocation EfficiencyAuddia’s 2025 financial posture exhibits the classic distress signals of an early-stage, asset-light R&D entity undergoing a deep transition. The company reported zero revenue for both the 2024 and 2025 fiscal years, highlighting a commercialization vacuum as it abandons its legacy platforms.

While the net loss narrowed by 11.8% year-over-year to $7.69 million—driven primarily by a 27.4% reduction in General & Administrative (G&A) expenses—this optical improvement masks underlying cash burn realities. Operating cash flow (OCF) outflows widened by 10.6% to $5.63 million. With only $3.18 million in cash equivalents at the close of 2025 and an estimated monthly burn rate of $470,000, capital allocation efficiency is critically strained. The "So What" here is unequivocal: independent auditors have issued a "going concern" warning, projecting that current liquidity will only sustain operations through the second quarter of 2026 without aggressive, highly dilutive external financing.

Strategic Pivots: Reshaping CAC and LTV via "Discovr Radio"

Operationally, Auddia’s strategic pivot is a calculated attempt to fundamentally alter its Customer Acquisition Cost (CAC) and Lifetime Value (LTV) profiles. Recognizing the prohibitive costs of competing with streaming giants for consumer subscriptions, management has repositioned its core AI technology toward a B2B SaaS model named *Discovr Radio*.

This model targets independent artists and record labels, offering them "guaranteed plays" by seamlessly injecting their tracks into the ad-breaks of traditional AM/FM radio streams via the proprietary *faidr* app. By transitioning the consumer-facing app to a free model, Auddia aims to drastically lower CAC to build an expansive "listener pool." Simultaneously, it captures higher-margin, sticky recurring revenue from B2B clients. Early pilot metrics are promising—yielding an average of 116 weekly plays per artist and an exceptional 30% Click-Through Rate (CTR) on artist pages—yet these remain unproven at a macroeconomic scale.

Strategic Moats and Technological Execution Risks

Auddia’s strategic moat is anchored in its edge-computing AI architecture, built on Google TensorFlow. The technology enables real-time, distributed inference on consumer devices to identify and time-shift audio segments (ads, DJ talks, music). Holding critical patents for the seamless integration of broadcast and streaming audio, the company possesses a moderate-to-high technical barrier to entry.

However, the sector positioning is fraught with execution and legal risks. The foundational legality of caching and replacing broadcast content relies heavily on the "Fair Use" doctrine (specifically time-shifting precedents). Any adverse regulatory shifts in statutory royalty rates or copyright interpretations could instantly neutralize this technological moat. Furthermore, operating with an asset-light workforce of just five full-time employees and heavy reliance on outsourced IT, the company's ability to maintain enterprise-grade SLA (Service Level Agreement) standards for its upcoming SaaS clients remains structurally questionable.

Sector Positioning & The High-Leverage Restructuring

The most critical variable in Auddia’s survival equation is its proposed merger with Thramann Holdings, an entity controlled by Auddia’s recently reinstated CEO, Jeff Thramann. The transaction aims to consolidate three AI-native early-stage companies under a new ticker, McCarthy Finney (MCFN).

Strategically, this associated party M&A is designed to generate AI scale and cross-platform synergies. Financially, it represents a massive dilution event. Existing Auddia shareholders will be compressed to a mere 20% economic interest in the new entity. More alarmingly, the merger is contingent upon Auddia securing $12 million in net cash at closing. This creates a systemic financing dependency, forcing the company to heavily leverage ATM facilities and convertible instruments, thereby triggering aggressive anti-dilution downward spirals for current equity holders.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Auddia as an enterprise in a financial "ICU" state. The strategic clarity of the B2B SaaS pivot is commendable—effectively addressing the systemic exposure problem for independent artists within the 62% of U.S. audio consumption still dominated by traditional radio.

However, the disparity between strategic vision and balance sheet reality is stark. The zero-revenue baseline, combined with the stringent $12 million capital requirement to close the survival-critical McCarthy Finney merger, creates an asymmetric risk profile. The company's future does not currently hinge on its AI algorithmic supremacy, but rather on its immediate capacity to execute highly dilutive capital market maneuvers before the Q2 2026 liquidity cliff.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com