Strategic Moats in Next-Gen Batteries: A Deep-Dive Analysis of Amprius vs. SES AI

Date : 2026-03-13

Reading : 131

The next-generation lithium battery sector has reached a critical inflection point. The era of pure laboratory-driven technological narratives has ended, replaced by an industry-wide mandate for commercial validation, capital allocation efficiency, and geopolitical supply chain restructuring. Based on a comprehensive MECE (Mutually Exclusive, Collectively Exhaustive) analysis of the 2025 Form 10-K filings from Amprius Technologies, Inc. (AMPX) and SES AI Corporation (SES), HDIN Research has identified a profound strategic divergence between the two entities. While Amprius is aggressively scaling commercialization through an asset-light hardware model, SES AI is pivoting heavily toward an "AI-plus-materials" service paradigm.

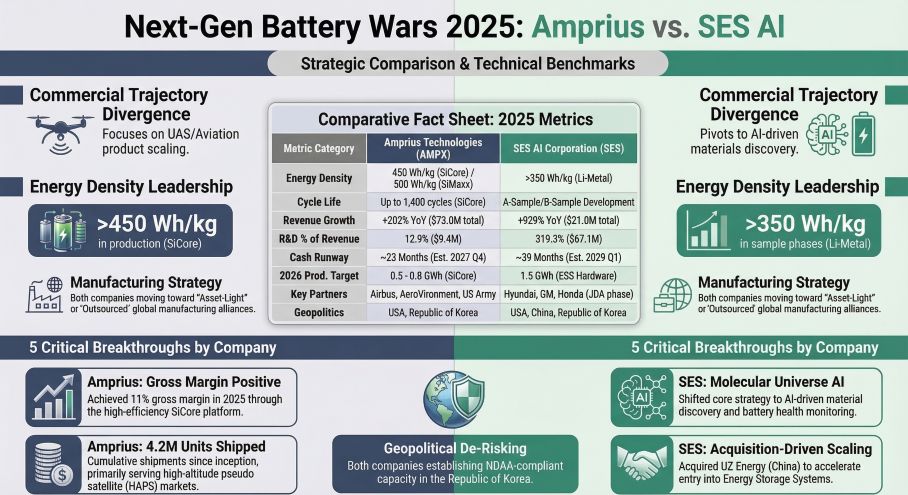

Figure Next-Gen Battery Wars 2025: Amprius vs SES AI

Here is our authoritative breakdown of their operational leverage, sector positioning, and the cyclical headwinds shaping the future of advanced energy storage.

Here is our authoritative breakdown of their operational leverage, sector positioning, and the cyclical headwinds shaping the future of advanced energy storage.

Financial Health & Revenue Quality: Hardware Execution vs. Service Premiums

A granular look at revenue streams reveals stark contrasts in business model maturity and earnings quality.

Amprius delivered a 202% revenue surge to $73.01 million in 2025. This was not merely top-line inflation; it was driven by the operational scale-up of its SiCore platform and deep market penetration into the Unmanned Aerial Systems (UAS) and High-Altitude Pseudo-Satellite (HAPS) aviation sectors. More importantly, Amprius achieved a paradigm shift in unit economics, flipping its gross margin from -76% to +11%. This margin expansion was directly catalyzed by turning fixed depreciation into variable costs through contract manufacturing.

Conversely, SES AI reported a staggering 929% revenue growth to $21 million. However, a structural dissection reveals that this growth relies heavily on service revenue ($13.6 million) and the "consolidation effect" of acquiring Chinese Energy Storage System (ESS) subsidiary UZ Energy, rather than organic growth in its core Li-Metal EV battery business. While SES boasts a nominal 53.8% gross margin, this is propped up by high-margin software/service contracts and obscures the inherent margin pressures of its unscaled hardware manufacturing.

Capital Allocation Efficiency: The Asset-Light Imperative

Faced with cyclical headwinds and a tightening capital environment, both companies are executing aggressive CapEx optimizations, abandoning the traditional "gigafactory" cash-burn model.

Amprius demonstrated exceptional capital discipline in 2025 by terminating its GWh factory lease in Brighton, Colorado. Although taking a short-term $19.1 million impairment hit and a $20 million termination fee, management effectively insulated the balance sheet from massive future fixed-asset depreciation. Amprius is now capitalizing on an outsourced manufacturing strategy via the "Amprius Korea Battery Alliance," securing over 2.0 GWh of capacity without the heavy capital expenditure.

SES AI, meanwhile, is redirecting its capital allocation from traditional mechanical depreciation to digital infrastructure. With R&D expenditures hitting $67.05 million (seven times that of Amprius), SES is aggressively leasing GPU computing power to train its "Molecular Universe" AI platform. By converting EV A-sample lines into drone battery production and seeking joint ventures (e.g., with Hisun) for electrolyte materials, SES is attempting to bypass heavy manufacturing constraints and position itself as an AI-driven materials licensor and ESS integrator.

Supply Chain Resilience & The NDAA Hurdle

The most pressing exogenous shock for both companies is geopolitical. Compliance with the US National Defense Authorization Act (NDAA)—specifically bypassing restrictions on "Foreign Entities of Concern"—is the ultimate barrier to entry for lucrative US Department of Defense and government contracts.

Currently, both companies face substantial China-dependency risks: Amprius relies on Berzelius for its core silicon anode materials, while SES's ESS footprint is heavily tied to UZ Energy.

To build resilient, NDAA-compliant supply chains, both firms are heavily leveraging South Korea. Amprius is already utilizing its Korean alliance for cell assembly to bypass direct sourcing restrictions, a move validated by a $14.8 million contract from the US Defense Innovation Unit (DIU). SES is similarly planning to establish NDAA-compliant production lines for high-energy-density drone cells within its South Korean facilities. Failure to execute this localized supply chain pivot will directly threaten their survival in the North American market.

HDIN Viewpoint

From an institutional perspective, HDIN Research views the 2025 fiscal year as a definitive "return to rationality" for the next-generation battery sector. The strategic moats of tomorrow are no longer built purely on theoretical energy density (Wh/kg), but on commercial pragmatism.

Amprius has proven the viability of an outsourced, asset-light model, establishing a dominant beachhead in the premium aviation/UAS sector. However, investors must monitor its soaring Accounts Receivable (up 325% in 2025), which vastly outpaced revenue growth, signaling potential credit risk or channel stuffing. SES AI, buoyed by a robust ~$200 million liquidity cushion, is effectively operating as a high-leverage "AI + Battery" call option. Its long-term viability will depend not on hardware scale, but on whether its Molecular Universe platform can monetize material discovery faster than its digital CapEx burn rate. Ultimately, victory in this space will belong to the players who successfully wed technological superiority with impenetrable, NDAA-compliant supply chain architectures.

---

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Next-Gen Battery Wars 2025: Amprius vs SES AI

Here is our authoritative breakdown of their operational leverage, sector positioning, and the cyclical headwinds shaping the future of advanced energy storage.Financial Health & Revenue Quality: Hardware Execution vs. Service Premiums

A granular look at revenue streams reveals stark contrasts in business model maturity and earnings quality.

Amprius delivered a 202% revenue surge to $73.01 million in 2025. This was not merely top-line inflation; it was driven by the operational scale-up of its SiCore platform and deep market penetration into the Unmanned Aerial Systems (UAS) and High-Altitude Pseudo-Satellite (HAPS) aviation sectors. More importantly, Amprius achieved a paradigm shift in unit economics, flipping its gross margin from -76% to +11%. This margin expansion was directly catalyzed by turning fixed depreciation into variable costs through contract manufacturing.

Conversely, SES AI reported a staggering 929% revenue growth to $21 million. However, a structural dissection reveals that this growth relies heavily on service revenue ($13.6 million) and the "consolidation effect" of acquiring Chinese Energy Storage System (ESS) subsidiary UZ Energy, rather than organic growth in its core Li-Metal EV battery business. While SES boasts a nominal 53.8% gross margin, this is propped up by high-margin software/service contracts and obscures the inherent margin pressures of its unscaled hardware manufacturing.

Capital Allocation Efficiency: The Asset-Light Imperative

Faced with cyclical headwinds and a tightening capital environment, both companies are executing aggressive CapEx optimizations, abandoning the traditional "gigafactory" cash-burn model.

Amprius demonstrated exceptional capital discipline in 2025 by terminating its GWh factory lease in Brighton, Colorado. Although taking a short-term $19.1 million impairment hit and a $20 million termination fee, management effectively insulated the balance sheet from massive future fixed-asset depreciation. Amprius is now capitalizing on an outsourced manufacturing strategy via the "Amprius Korea Battery Alliance," securing over 2.0 GWh of capacity without the heavy capital expenditure.

SES AI, meanwhile, is redirecting its capital allocation from traditional mechanical depreciation to digital infrastructure. With R&D expenditures hitting $67.05 million (seven times that of Amprius), SES is aggressively leasing GPU computing power to train its "Molecular Universe" AI platform. By converting EV A-sample lines into drone battery production and seeking joint ventures (e.g., with Hisun) for electrolyte materials, SES is attempting to bypass heavy manufacturing constraints and position itself as an AI-driven materials licensor and ESS integrator.

Supply Chain Resilience & The NDAA Hurdle

The most pressing exogenous shock for both companies is geopolitical. Compliance with the US National Defense Authorization Act (NDAA)—specifically bypassing restrictions on "Foreign Entities of Concern"—is the ultimate barrier to entry for lucrative US Department of Defense and government contracts.

Currently, both companies face substantial China-dependency risks: Amprius relies on Berzelius for its core silicon anode materials, while SES's ESS footprint is heavily tied to UZ Energy.

To build resilient, NDAA-compliant supply chains, both firms are heavily leveraging South Korea. Amprius is already utilizing its Korean alliance for cell assembly to bypass direct sourcing restrictions, a move validated by a $14.8 million contract from the US Defense Innovation Unit (DIU). SES is similarly planning to establish NDAA-compliant production lines for high-energy-density drone cells within its South Korean facilities. Failure to execute this localized supply chain pivot will directly threaten their survival in the North American market.

HDIN Viewpoint

From an institutional perspective, HDIN Research views the 2025 fiscal year as a definitive "return to rationality" for the next-generation battery sector. The strategic moats of tomorrow are no longer built purely on theoretical energy density (Wh/kg), but on commercial pragmatism.

Amprius has proven the viability of an outsourced, asset-light model, establishing a dominant beachhead in the premium aviation/UAS sector. However, investors must monitor its soaring Accounts Receivable (up 325% in 2025), which vastly outpaced revenue growth, signaling potential credit risk or channel stuffing. SES AI, buoyed by a robust ~$200 million liquidity cushion, is effectively operating as a high-leverage "AI + Battery" call option. Its long-term viability will depend not on hardware scale, but on whether its Molecular Universe platform can monetize material discovery faster than its digital CapEx burn rate. Ultimately, victory in this space will belong to the players who successfully wed technological superiority with impenetrable, NDAA-compliant supply chain architectures.

---

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com