Taeyang Corporation 2025 Annual Analysis: Defensive Contraction, Strategic Moats, and Supply Chain Pivots

Date : 2026-03-12

Reading : 281

Taeyang Corporation continues to exercise formidable market dominance in the global portable butane gas sector, commanding a 60% worldwide market share. However, a deep-dive analysis of its 2025 financial year reveals a business model in transition. Characterized by defensive balance sheet contraction and a stark divergence in capacity utilization, Taeyang’s latest performance highlights the tension between maximizing a legacy "cash cow" and navigating the cyclical headwinds of a saturated market.

Figure Taeyang Corporation 2025: Global Dominance & Defensive Financial Resilience

Below, HDIN Research unpacks the strategic implications behind the data, evaluating the company's capital allocation efficiency, global supply chain restructuring, and core profitability drivers.

Below, HDIN Research unpacks the strategic implications behind the data, evaluating the company's capital allocation efficiency, global supply chain restructuring, and core profitability drivers.

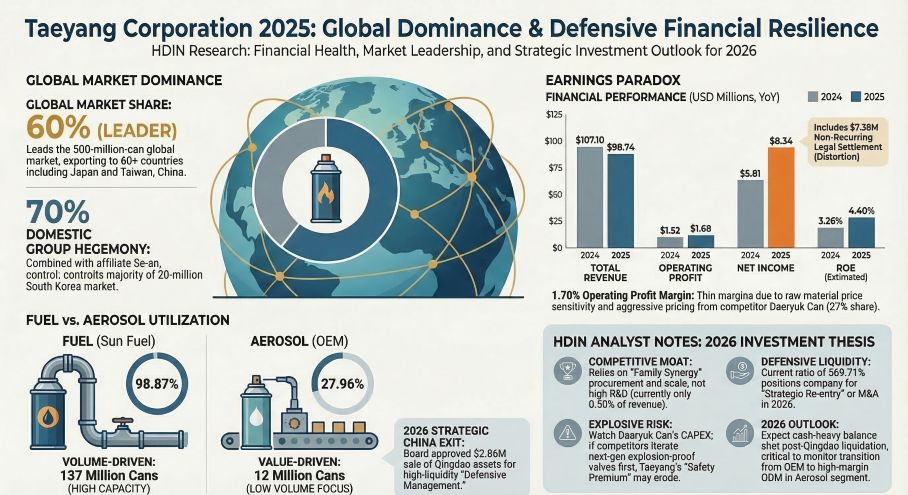

Sector Positioning and Strategic Moats

Taeyang’s economic moat is fundamentally built on extreme scale economies and group-level synergies. Operating the world’s largest automated production lines, the company’s fuel tube (butane gas) division is running at a near-maximum capacity utilization rate of 98.87%.

In its domestic South Korean market, Taeyang and its affiliated entities (such as Se-an) maintain a combined 70% oligopolistic share. This entrenched positioning allows the company to absorb raw material price shocks better than its primary domestic rival, Daeryuk Can (27% share). While Chinese competitors have historically attempted to undercut pricing, Taeyang’s stringent adherence to ISO safety standards and proprietary anti-explosion technology has successfully defended its premium brand positioning ("SUN Fuel") across 60 global markets.

Financial Health & Capital Allocation Efficiency

On the surface, Taeyang reported a striking 43.48% year-over-year surge in net profit, reaching $8.34 million. However, a forensic look at the income statement reveals a different operational reality. Top-line revenue actually contracted by 7.8% to $98.74 million due to shrinking end-market demand. The bottom-line inflation was heavily distorted by $7.55 million in non-recurring miscellaneous income derived from shareholder lawsuit compensations.

Stripping away this anomaly, the core operating margin hovered at a fragile 1.71%. The modest 85-basis-point expansion in gross margin (14.13%) was entirely driven by cyclical relief in raw material costs—specifically a 1.44% drop in tinplate prices—rather than volume expansion or premium pricing power.

Crucially, Taeyang's capital allocation points to a highly conservative, defensive posture. The company's CAPEX-to-Depreciation ratio sits at a low 0.45x. According to institutional capital productivity frameworks, a ratio persistently below 1.0x indicates a management team focused strictly on maintenance expenditures rather than capacity expansion or technological upgrades. With a current ratio of 569.7% and zero interest-bearing debt, Taeyang suffers from inefficient capital hoarding rather than deploying excess liquidity toward high-yield growth avenues.

Strategic Pivots: Supply Chain Restructuring

To counter cyclical headwinds, Taeyang is executing a major strategic retreat from heavy-asset manufacturing in China. The board has approved the divestment of its 49.04% stake in Qingdao Seian for approximately $2.87 million—a transaction expected to close in 2026 at a substantial premium to its book value.

This asset liquidation marks a definitive shift toward a capital-light export model. Going forward, the company intends to service global demand directly from its South Korean hub while utilizing its U.S. subsidiary (Sun America Inc.) to penetrate the high-margin North American outdoor leisure market.

Simultaneously, Taeyang faces an urgent need to revitalize its aerosol division, which languished at a severe 27.96% capacity utilization rate in 2025. Management is attempting to pivot this segment from a low-margin OEM model to a high-value ODM (Original Design Manufacturing) structure, targeting the medical and cosmetics sectors. However, with R&D spending capped at a mere 0.5% of total revenue, the execution speed of this transition remains a critical uncertainty.

Cyclical Headwinds and Governance Risks

Taeyang operates without financial hedging instruments, relying entirely on operational maneuvers—such as dynamic pricing adjustments and bulk synergistic procurement—to offset commodity fluctuations. This exposes the firm to severe margin compression if global LPG or tinplate prices spike unexpectedly. Furthermore, as a family-controlled enterprise (62.48% insider ownership), heavy reliance on related-party transactions for raw material sourcing necessitates a high degree of investor scrutiny regarding long-term governance and minority shareholder alignment.

HDIN Viewpoint

As an independent market consulting firm, HDIN Research views Taeyang Corporation at a critical strategic crossroads. The company has masterfully defended its legacy oligopoly, but its current valuation logic remains tethered to slow-growth traditional manufacturing. The true test for Taeyang’s management will arrive in 2026 following the cash infusion from the Qingdao divestment. If this liquidity is deployed to aggressively accelerate the Aerosol ODM transition and upgrade automated production, a structural re-rating is possible. Conversely, if the capital is merely parked in short-term financial instruments, the company risks long-term stagnation in a mature market.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Taeyang Corporation 2025: Global Dominance & Defensive Financial Resilience

Below, HDIN Research unpacks the strategic implications behind the data, evaluating the company's capital allocation efficiency, global supply chain restructuring, and core profitability drivers.Sector Positioning and Strategic Moats

Taeyang’s economic moat is fundamentally built on extreme scale economies and group-level synergies. Operating the world’s largest automated production lines, the company’s fuel tube (butane gas) division is running at a near-maximum capacity utilization rate of 98.87%.

In its domestic South Korean market, Taeyang and its affiliated entities (such as Se-an) maintain a combined 70% oligopolistic share. This entrenched positioning allows the company to absorb raw material price shocks better than its primary domestic rival, Daeryuk Can (27% share). While Chinese competitors have historically attempted to undercut pricing, Taeyang’s stringent adherence to ISO safety standards and proprietary anti-explosion technology has successfully defended its premium brand positioning ("SUN Fuel") across 60 global markets.

Financial Health & Capital Allocation Efficiency

On the surface, Taeyang reported a striking 43.48% year-over-year surge in net profit, reaching $8.34 million. However, a forensic look at the income statement reveals a different operational reality. Top-line revenue actually contracted by 7.8% to $98.74 million due to shrinking end-market demand. The bottom-line inflation was heavily distorted by $7.55 million in non-recurring miscellaneous income derived from shareholder lawsuit compensations.

Stripping away this anomaly, the core operating margin hovered at a fragile 1.71%. The modest 85-basis-point expansion in gross margin (14.13%) was entirely driven by cyclical relief in raw material costs—specifically a 1.44% drop in tinplate prices—rather than volume expansion or premium pricing power.

Crucially, Taeyang's capital allocation points to a highly conservative, defensive posture. The company's CAPEX-to-Depreciation ratio sits at a low 0.45x. According to institutional capital productivity frameworks, a ratio persistently below 1.0x indicates a management team focused strictly on maintenance expenditures rather than capacity expansion or technological upgrades. With a current ratio of 569.7% and zero interest-bearing debt, Taeyang suffers from inefficient capital hoarding rather than deploying excess liquidity toward high-yield growth avenues.

Strategic Pivots: Supply Chain Restructuring

To counter cyclical headwinds, Taeyang is executing a major strategic retreat from heavy-asset manufacturing in China. The board has approved the divestment of its 49.04% stake in Qingdao Seian for approximately $2.87 million—a transaction expected to close in 2026 at a substantial premium to its book value.

This asset liquidation marks a definitive shift toward a capital-light export model. Going forward, the company intends to service global demand directly from its South Korean hub while utilizing its U.S. subsidiary (Sun America Inc.) to penetrate the high-margin North American outdoor leisure market.

Simultaneously, Taeyang faces an urgent need to revitalize its aerosol division, which languished at a severe 27.96% capacity utilization rate in 2025. Management is attempting to pivot this segment from a low-margin OEM model to a high-value ODM (Original Design Manufacturing) structure, targeting the medical and cosmetics sectors. However, with R&D spending capped at a mere 0.5% of total revenue, the execution speed of this transition remains a critical uncertainty.

Cyclical Headwinds and Governance Risks

Taeyang operates without financial hedging instruments, relying entirely on operational maneuvers—such as dynamic pricing adjustments and bulk synergistic procurement—to offset commodity fluctuations. This exposes the firm to severe margin compression if global LPG or tinplate prices spike unexpectedly. Furthermore, as a family-controlled enterprise (62.48% insider ownership), heavy reliance on related-party transactions for raw material sourcing necessitates a high degree of investor scrutiny regarding long-term governance and minority shareholder alignment.

HDIN Viewpoint

As an independent market consulting firm, HDIN Research views Taeyang Corporation at a critical strategic crossroads. The company has masterfully defended its legacy oligopoly, but its current valuation logic remains tethered to slow-growth traditional manufacturing. The true test for Taeyang’s management will arrive in 2026 following the cash infusion from the Qingdao divestment. If this liquidity is deployed to aggressively accelerate the Aerosol ODM transition and upgrade automated production, a structural re-rating is possible. Conversely, if the capital is merely parked in short-term financial instruments, the company risks long-term stagnation in a mature market.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com