Miwon Chemicals 2025 Strategic Review: Niche Market Dominance Amid Cyclical Headwinds

Date : 2026-03-14

Reading : 100

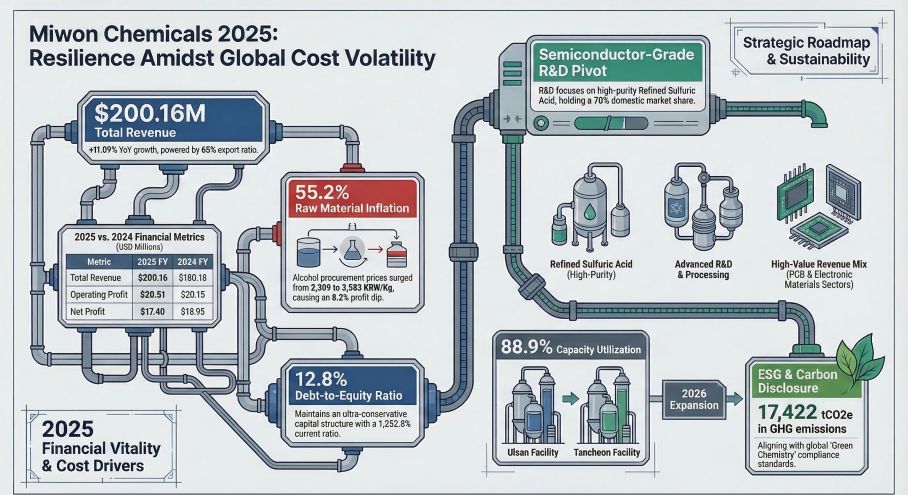

Despite severe cyclical headwinds and a 55% surge in core raw material costs, Miwon Chemicals leveraged its strategic moat in the fine chemicals sector to deliver robust top-line growth in 2025. According to the latest analysis by HDIN Research, the company generated $200 million in total revenue—an 11.09% year-over-year increase—fueled largely by an aggressive export strategy. However, the true narrative lies beneath the top line: a textbook case of how extreme capital allocation efficiency and a monopolistic grip on niche markets can insulate a manufacturer against global supply chain volatility.

Figure Miwon Chemicals 2025: Resilience Amidst Global Cost Volatility

Below, HDIN Research dissects the strategic implications behind Miwon Chemicals' 2025 financial and operational metrics.

Below, HDIN Research dissects the strategic implications behind Miwon Chemicals' 2025 financial and operational metrics.

Sector Positioning: The Power of Strategic Moats

Miwon Chemicals does not rely on disruptive, high-premium innovation; rather, it thrives on "niche market scale monopoly." The company commands a staggering 70% of the South Korean refined sulfuric acid market and 60% of the powder sulfur market.

The "So What" Factor: This absolute dominance establishes an asymmetric barrier to entry. For global giants, penetrating this localized market is economically unviable due to Miwon's entrenched scale economies and logistics optimization. Furthermore, Miwon’s refined sulfuric acid and functional sulfur chemicals act as the "underlying primer" for the high-end electronics industry, particularly in PCB (Printed Circuit Board) manufacturing and semiconductor plating. By securing long-term technology stickiness with global electronics makers, Miwon has effectively insulated its core revenue streams from macroeconomic shocks.

Operational Efficiency Amid Cyclical Headwinds

While revenue surged, Miwon's net profit experienced an 8.18% decline, settling at $17.40 million. This margin compression was directly driven by external supply chain risks, most notably a 55.2% spike in the procurement price of alcohols (from 2,309 KRW/Kg to 3,583 KRW/Kg), tied to global oil fluctuations.

Despite this rigid cost squeeze, operating profit grew marginally by 1.81% to $20.54 million. This resilience stems from exceptional operational efficiency. The company maintained an inventory turnover rate of 11.3x. A deeper dive into the $15.13 million ending inventory reveals that the slight increase was not channel stuffing, but rather a defensive, strategic stockpiling of raw materials to hedge against further price volatility.

Capital Allocation Efficiency & Governance

Miwon Chemicals exhibits a fortress-like balance sheet. Closing 2025 with an astronomical current ratio of 1,252.8% and a debt ratio of merely 12.8%, the company operates with a highly conservative financial posture.

The "So What" Factor: This ultra-low leverage is not a limitation; it is strategic leverage hoarding. It allows the company to execute a "cash cow" shareholder return policy—distributing nearly 60% of its net profit back to investors through a 35.97% dividend payout ratio ($6.26 million) and aggressive stock buybacks ($4.01 million).

From a governance perspective, Miwon utilizes an asset-light, highly integrated related-party network to manage its international footprint. In the Greater China region, rather than deploying capital-heavy direct investments, Miwon utilizes entities like Miwon Nantong Chemical and Miwon Guangzhou Chemical to optimize its distribution network while maintaining strict adherence to global ESG and chemical compliance standards (e.g., K-REACH equivalents).

Strategic Pivots: The Capacity and R&D Conundrum

As Miwon enters 2026, it faces two critical strategic inflection points:

1. Capacity Ceilings: The company is currently operating at an 88.89% capacity utilization rate. To prevent revenue growth from hitting a physical ceiling, HDIN Research anticipates that Miwon must deploy its ample cash reserves toward significant capital expenditures (CAPEX) in the next 12-24 months.

2. R&D Intensity: The company’s R&D expenditure remains persistently low at 0.5% of revenue ($0.94 million). The current focus is strictly on applied modifications and high-value surfactant improvements. While sufficient for maintaining current client relationships, this lack of forward-looking R&D poses a long-term risk of market share erosion in the advanced semiconductor materials sector.

HDIN Viewpoint

HDIN Research views Miwon Chemicals as a premier "value-defensive" asset. The company has successfully weaponized its market share and conservative balance sheet to absorb severe inflationary pressures. While complex family-led governance and related-party transactions warrant standard investor scrutiny, the sheer volume of shareholder returns provides a substantial premium to offset these structural risks. Moving forward, the true test for Miwon’s management will be successfully executing a CAPEX cycle to break through its current capacity constraints without compromising its pristine capital allocation metrics.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Video Analysis

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Miwon Chemicals 2025: Resilience Amidst Global Cost Volatility

Below, HDIN Research dissects the strategic implications behind Miwon Chemicals' 2025 financial and operational metrics.Sector Positioning: The Power of Strategic Moats

Miwon Chemicals does not rely on disruptive, high-premium innovation; rather, it thrives on "niche market scale monopoly." The company commands a staggering 70% of the South Korean refined sulfuric acid market and 60% of the powder sulfur market.

The "So What" Factor: This absolute dominance establishes an asymmetric barrier to entry. For global giants, penetrating this localized market is economically unviable due to Miwon's entrenched scale economies and logistics optimization. Furthermore, Miwon’s refined sulfuric acid and functional sulfur chemicals act as the "underlying primer" for the high-end electronics industry, particularly in PCB (Printed Circuit Board) manufacturing and semiconductor plating. By securing long-term technology stickiness with global electronics makers, Miwon has effectively insulated its core revenue streams from macroeconomic shocks.

Operational Efficiency Amid Cyclical Headwinds

While revenue surged, Miwon's net profit experienced an 8.18% decline, settling at $17.40 million. This margin compression was directly driven by external supply chain risks, most notably a 55.2% spike in the procurement price of alcohols (from 2,309 KRW/Kg to 3,583 KRW/Kg), tied to global oil fluctuations.

Despite this rigid cost squeeze, operating profit grew marginally by 1.81% to $20.54 million. This resilience stems from exceptional operational efficiency. The company maintained an inventory turnover rate of 11.3x. A deeper dive into the $15.13 million ending inventory reveals that the slight increase was not channel stuffing, but rather a defensive, strategic stockpiling of raw materials to hedge against further price volatility.

Capital Allocation Efficiency & Governance

Miwon Chemicals exhibits a fortress-like balance sheet. Closing 2025 with an astronomical current ratio of 1,252.8% and a debt ratio of merely 12.8%, the company operates with a highly conservative financial posture.

The "So What" Factor: This ultra-low leverage is not a limitation; it is strategic leverage hoarding. It allows the company to execute a "cash cow" shareholder return policy—distributing nearly 60% of its net profit back to investors through a 35.97% dividend payout ratio ($6.26 million) and aggressive stock buybacks ($4.01 million).

From a governance perspective, Miwon utilizes an asset-light, highly integrated related-party network to manage its international footprint. In the Greater China region, rather than deploying capital-heavy direct investments, Miwon utilizes entities like Miwon Nantong Chemical and Miwon Guangzhou Chemical to optimize its distribution network while maintaining strict adherence to global ESG and chemical compliance standards (e.g., K-REACH equivalents).

Strategic Pivots: The Capacity and R&D Conundrum

As Miwon enters 2026, it faces two critical strategic inflection points:

1. Capacity Ceilings: The company is currently operating at an 88.89% capacity utilization rate. To prevent revenue growth from hitting a physical ceiling, HDIN Research anticipates that Miwon must deploy its ample cash reserves toward significant capital expenditures (CAPEX) in the next 12-24 months.

2. R&D Intensity: The company’s R&D expenditure remains persistently low at 0.5% of revenue ($0.94 million). The current focus is strictly on applied modifications and high-value surfactant improvements. While sufficient for maintaining current client relationships, this lack of forward-looking R&D poses a long-term risk of market share erosion in the advanced semiconductor materials sector.

HDIN Viewpoint

HDIN Research views Miwon Chemicals as a premier "value-defensive" asset. The company has successfully weaponized its market share and conservative balance sheet to absorb severe inflationary pressures. While complex family-led governance and related-party transactions warrant standard investor scrutiny, the sheer volume of shareholder returns provides a substantial premium to offset these structural risks. Moving forward, the true test for Miwon’s management will be successfully executing a CAPEX cycle to break through its current capacity constraints without compromising its pristine capital allocation metrics.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Video Analysis

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com