Samsung Electro-Mechanics 2025: Transitioning from Component Supplier to AI & xEV Solutions Powerhouse

Date : 2026-03-14

Reading : 3175

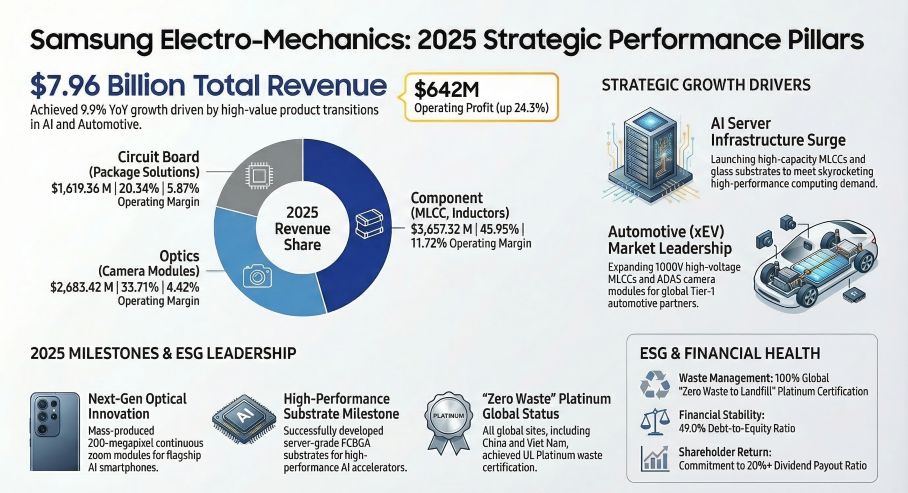

In 2025, Samsung Electro-Mechanics (SEMCO) successfully validated its multi-year strategic pivot, transforming from a commoditized mobile component supplier into a high-value system solution provider driven by Artificial Intelligence (AI) and electrified vehicles (xEV). Generating $7.96 billion (11.31 trillion KRW) in revenue—a 9.9% year-over-year increase—and surging operating profits by 24.3% to $643 million, the company has demonstrated robust capital allocation efficiency. By systematically shedding low-margin units and aggressively deploying capital into high-barrier AI servers and advanced automotive driver-assistance systems (ADAS), SEMCO has built a formidable strategic moat against volatile consumer electronics cycles.

Figure Samsung Electro-Mechanics: 2025 Strategic Performance Pillars

Capital Allocation Efficiency and Portfolio Optimization

Capital Allocation Efficiency and Portfolio Optimization

The core driver behind SEMCO’s robust financial health is not merely volume growth, but highly disciplined product mix enhancement. Management has executed a ruthless strategic contraction of non-core operations, divesting legacy RFPCB, Wi-Fi, and communication module businesses over recent years. By redirecting these resources into frontier technologies, SEMCO has secured substantial pricing power across its core segments.

This strategic recalibration is evident in the upward trajectory of its Average Selling Prices (ASP) in 2025. The Optical Solutions division saw ASP surge by 14.0%, fueled by the integration of 200MP sensors, continuous zoom, and hybrid lenses for automotive applications. Simultaneously, the Package Solutions (substrates) ASP grew by 4.1%, driven by the transition from mobile to high-end Flip-Chip Ball Grid Array (FC-BGA) substrates required for high-performance computing (HPC). Even in the highly competitive MLCC (Component) segment, a shift toward ultra-small, high-capacity IT and highly reliable automotive products allowed SEMCO to maintain a positive ASP growth of 0.9%.

Sector Positioning: Fortifying Strategic Moats in MLCC and Advanced Substrates

SEMCO’s sector positioning reveals a deliberate move to challenge incumbent leaders in high-margin niches. In the MLCC market, the company expanded its global share to 23%, firmly consolidating its position at the top of the second tier and closing the gap with the industry leader, Murata. Rather than competing purely on scale, SEMCO is encroaching on the core profit zones of Murata and Taiyo Yuden by mastering high-temperature (150℃+) and high-voltage MLCCs essential for AI servers and EV powertrains.

In the advanced substrate sector, SEMCO is engineering a strategic bypass. Facing formidable scale from Taiwanese leaders like Unimicron, SEMCO is leveraging heavy R&D to pioneer next-generation Glass Substrate technology. This forward-looking approach aims to solve the warpage control and embedding bottlenecks inherent in modern Chiplet and AI accelerator packaging. While high R&D and aggressive CapEx deployment ($813 million in 2025) caused a short-term 14% dip in the substrate division's operating profit due to depreciation amortization, this is a necessary cyclical headwind to secure long-term architectural dominance in AI infrastructure.

Navigating Cyclical Headwinds and Supply Chain Dependencies

Despite its technological leadership, SEMCO’s structural ecosystem presents critical dependencies that require continuous risk management. The most pronounced vulnerability is customer concentration: approximately 27% of its total revenue is derived from Samsung Electronics and its affiliates. To mitigate this internal procurement risk, SEMCO is aggressively diversifying its global client base, securing strategic partnerships with Google, Intel, Tesla, and Bosch.

Furthermore, the company faces exposure to raw material supply chain concentration, heavily relying on Japanese suppliers for core pastes, powders, and CCL/PPG materials. To counter these geopolitical and macro-economic headwinds, SEMCO has internalized the manufacturing of critical sub-components—such as optical lenses and ultra-precision actuators—creating a vertical integration model rarely seen in the optical module industry. Coupled with a globally distributed manufacturing footprint across China, Vietnam, the Philippines, and Mexico, SEMCO has engineered significant supply chain resilience.

HDIN Viewpoint: The Institutional Perspective

HDIN Research views Samsung Electro-Mechanics as a premier proxy for the AI hardware infrastructure and electrification supercycles. The company's 2025 performance underscores a textbook execution of value migration: sacrificing low-yield volume for high-barrier technological leadership.

The company's R&D intensity—scaling to 7.0% of revenue ($554 million)—and a formidable portfolio of over 11,200 patents form an impenetrable barrier to entry for new market participants. Furthermore, SEMCO’s proactive corporate governance, featuring a 57% independent board, a commitment to a minimum 20% dividend payout ratio, and a net-cash balance sheet, provides a highly defensive foundation against the projected 2026 macroeconomic slowdown.

Looking ahead, HDIN Research advises investors to closely monitor SEMCO’s integration of "Agentic AI" across its development and manufacturing pipelines targeted for 2026. This operational digitization, combined with their first-mover advantage in glass substrates, will likely serve as the critical catalyst for expanding operating leverage and securing permanent pricing power in the next decade of advanced electronics.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Samsung Electro-Mechanics: 2025 Strategic Performance Pillars

Capital Allocation Efficiency and Portfolio OptimizationThe core driver behind SEMCO’s robust financial health is not merely volume growth, but highly disciplined product mix enhancement. Management has executed a ruthless strategic contraction of non-core operations, divesting legacy RFPCB, Wi-Fi, and communication module businesses over recent years. By redirecting these resources into frontier technologies, SEMCO has secured substantial pricing power across its core segments.

This strategic recalibration is evident in the upward trajectory of its Average Selling Prices (ASP) in 2025. The Optical Solutions division saw ASP surge by 14.0%, fueled by the integration of 200MP sensors, continuous zoom, and hybrid lenses for automotive applications. Simultaneously, the Package Solutions (substrates) ASP grew by 4.1%, driven by the transition from mobile to high-end Flip-Chip Ball Grid Array (FC-BGA) substrates required for high-performance computing (HPC). Even in the highly competitive MLCC (Component) segment, a shift toward ultra-small, high-capacity IT and highly reliable automotive products allowed SEMCO to maintain a positive ASP growth of 0.9%.

Sector Positioning: Fortifying Strategic Moats in MLCC and Advanced Substrates

SEMCO’s sector positioning reveals a deliberate move to challenge incumbent leaders in high-margin niches. In the MLCC market, the company expanded its global share to 23%, firmly consolidating its position at the top of the second tier and closing the gap with the industry leader, Murata. Rather than competing purely on scale, SEMCO is encroaching on the core profit zones of Murata and Taiyo Yuden by mastering high-temperature (150℃+) and high-voltage MLCCs essential for AI servers and EV powertrains.

In the advanced substrate sector, SEMCO is engineering a strategic bypass. Facing formidable scale from Taiwanese leaders like Unimicron, SEMCO is leveraging heavy R&D to pioneer next-generation Glass Substrate technology. This forward-looking approach aims to solve the warpage control and embedding bottlenecks inherent in modern Chiplet and AI accelerator packaging. While high R&D and aggressive CapEx deployment ($813 million in 2025) caused a short-term 14% dip in the substrate division's operating profit due to depreciation amortization, this is a necessary cyclical headwind to secure long-term architectural dominance in AI infrastructure.

Navigating Cyclical Headwinds and Supply Chain Dependencies

Despite its technological leadership, SEMCO’s structural ecosystem presents critical dependencies that require continuous risk management. The most pronounced vulnerability is customer concentration: approximately 27% of its total revenue is derived from Samsung Electronics and its affiliates. To mitigate this internal procurement risk, SEMCO is aggressively diversifying its global client base, securing strategic partnerships with Google, Intel, Tesla, and Bosch.

Furthermore, the company faces exposure to raw material supply chain concentration, heavily relying on Japanese suppliers for core pastes, powders, and CCL/PPG materials. To counter these geopolitical and macro-economic headwinds, SEMCO has internalized the manufacturing of critical sub-components—such as optical lenses and ultra-precision actuators—creating a vertical integration model rarely seen in the optical module industry. Coupled with a globally distributed manufacturing footprint across China, Vietnam, the Philippines, and Mexico, SEMCO has engineered significant supply chain resilience.

HDIN Viewpoint: The Institutional Perspective

HDIN Research views Samsung Electro-Mechanics as a premier proxy for the AI hardware infrastructure and electrification supercycles. The company's 2025 performance underscores a textbook execution of value migration: sacrificing low-yield volume for high-barrier technological leadership.

The company's R&D intensity—scaling to 7.0% of revenue ($554 million)—and a formidable portfolio of over 11,200 patents form an impenetrable barrier to entry for new market participants. Furthermore, SEMCO’s proactive corporate governance, featuring a 57% independent board, a commitment to a minimum 20% dividend payout ratio, and a net-cash balance sheet, provides a highly defensive foundation against the projected 2026 macroeconomic slowdown.

Looking ahead, HDIN Research advises investors to closely monitor SEMCO’s integration of "Agentic AI" across its development and manufacturing pipelines targeted for 2026. This operational digitization, combined with their first-mover advantage in glass substrates, will likely serve as the critical catalyst for expanding operating leverage and securing permanent pricing power in the next decade of advanced electronics.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com