LRS vs. Heavy CapEx: The Strategic Divergence of CATL and Samsung SDI in 2025

Date : 2026-03-12

Reading : 335

The global lithium-ion battery sector has definitively exited its era of blind capacity expansion, entering a ruthless phase of structural adjustment defined by "high-quality growth." According to the latest 2025 financial report analysis conducted by HDIN Research, the strategic divergence between industry giants CATL and Samsung SDI illustrates a stark contrast in capital allocation efficiency, sector positioning, and resilience against cyclical headwinds.

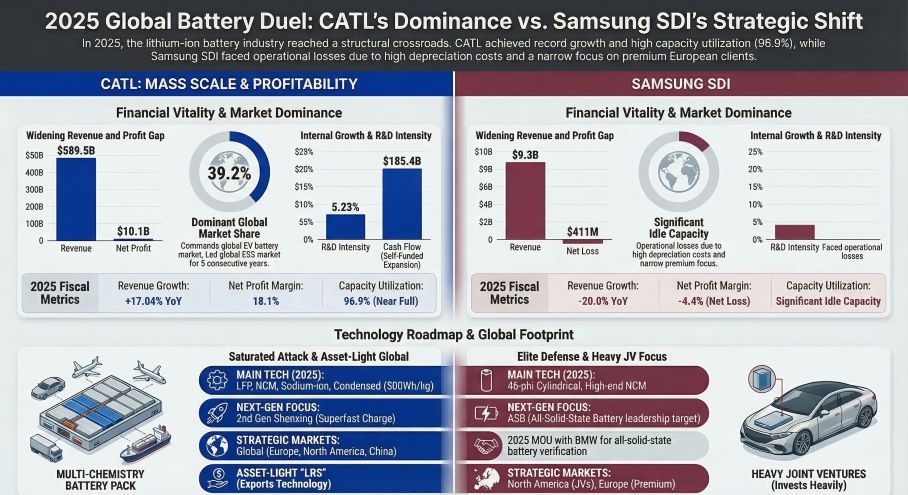

While CATL has leveraged extreme scale and a closed-loop ecosystem to achieve a 42.28% surge in net profit ($10.04 billion), Samsung SDI’s heavy reliance on premium European automotive OEMs and high-cost North American joint ventures resulted in a $411 million net loss. The data reveals a critical market reality: surviving the current geopolitical and macroeconomic headwinds requires more than just energy density—it demands comprehensive value chain sovereignty.

Figure 2025 Global Battery Duel: CATL's Dominance vs. Samsung SDl's Strategic Shift

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

The financial divergence between the two firms is rooted not merely in sales volume, but in structural operational efficiency. CATL reported 2025 revenues of $58.95 billion (a 17.04% increase), underpinned by an astonishing 96.9% capacity utilization rate. This near-maximum utilization dilutes fixed costs, enabling a highly defensive comprehensive unit cost of approximately $65.75/kWh.

Conversely, Samsung SDI’s energy solutions division suffered a 20.0% revenue contraction, pulling total revenues down to $9.33 billion. The strategic implication is clear: SDI is currently trapped in a structural CapEx dilemma. To comply with the U.S. Inflation Reduction Act (IRA), SDI is funneling massive capital into heavy-asset joint ventures with Stellantis and GM. However, a slowdown in Western EV adoption has left SDI grappling with unabsorbed fixed costs and severe asset impairment pressures. To fund this costly localized expansion, SDI was forced to liquidate non-core assets, including its polarizer business, to generate $788 million in liquidity.

Sector Positioning: The ESS "Safety Net" and Scenario Proliferation

The pure-play EV narrative is decelerating, shifting the battleground to Energy Storage Systems (ESS) and niche commercial applications. Here, CATL’s "full-domain increment" strategy has proven highly effective. Driven by the explosive power demands of AI data centers, CATL’s ESS battery sales hit 121 GWh (up 29.13% year-over-year), capitalizing on high-margin UPS and BBU deployments. Furthermore, CATL has successfully diversified into heavy-duty trucks, eVTOLs (electric vertical takeoff and landing aircraft) with its 500Wh/kg condensed battery, and marine applications, effectively insulating itself from passenger EV cyclicality.

Samsung SDI is attempting to pivot, accelerating the conversion of certain U.S. production lines to ESS formats to dilute idle capacity. However, SDI’s historical positioning as a "boutique" supplier to premium European automakers (like BMW and Volvo) means its product mix lacks the immediate, diversified scale required to fully offset the automotive downturn.

Strategic Moats: Geopolitical Navigation and Supply Chain Sovereignty

In 2025, geopolitical compliance is as critical as electrochemistry. The European Union’s carbon footprint regulations and U.S. localized manufacturing mandates have forced both companies to innovate their global expansion models.

CATL has engineered a sophisticated "LRS" (Licensing, Royalty, Service) model. By exporting patents and operational expertise to automakers like Ford and GM rather than taking direct equity stakes, CATL bypasses Foreign Entity of Concern (FEOC) restrictions. This asset-light approach secures high-margin royalty streams without the geopolitical risk of stranded CapEx. Simultaneously, CATL’s vertical integration—recovering 210,000 tons of battery materials in 2025—creates a closed-loop supply chain that inherently satisfies the EU’s strict zero-carbon and recycled material mandates.

Samsung SDI has opted for a "deep embedding" strategy, tying its fortunes to multi-billion-dollar localized JVs. While this ensures direct access to U.S. subsidies, it exposes the company to severe margin compression caused by elevated Western labor and energy costs, exacerbated by its reliance on external suppliers for up to 58% of its cathode materials.

HDIN Viewpoint: The Next 12 Months

From the perspective of HDIN Research, the 2025 landscape highlights a transition where profit pools are consolidating toward players with "full-domain ecosystem sovereignty." CATL is no longer just a battery manufacturer; it is evolving into a global zero-carbon infrastructure platform. Its ability to generate $18.53 billion in operating cash flow provides an insurmountable moat for aggressive R&D and multi-chemistry dominance (LFP, NCM, Sodium-ion).

Samsung SDI, meanwhile, is executing a high-stakes defensive strategy. By betting heavily on its upcoming 46-phi large cylindrical formats and All-Solid-State Batteries (ASB), SDI is attempting to leapfrog the current cost-war via technological disruption. However, until ASB reaches commercial maturity, SDI faces a precarious transitional period. For investors and industry stakeholders, the critical metric to watch over the next 12 months is not just GWh output, but the ratio of CapEx to actualized cash flow in localized Western facilities.

Presentation Download & Media Access

To dive deeper into the financial models and strategic frameworks discussed in this article:

* Presentation Download: Click the PDF download link under “Related Topics” to access the presentation of this report.

* Video Analysis: Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

While CATL has leveraged extreme scale and a closed-loop ecosystem to achieve a 42.28% surge in net profit ($10.04 billion), Samsung SDI’s heavy reliance on premium European automotive OEMs and high-cost North American joint ventures resulted in a $411 million net loss. The data reveals a critical market reality: surviving the current geopolitical and macroeconomic headwinds requires more than just energy density—it demands comprehensive value chain sovereignty.

Figure 2025 Global Battery Duel: CATL's Dominance vs. Samsung SDl's Strategic Shift

Financial Health & Capital Allocation EfficiencyThe financial divergence between the two firms is rooted not merely in sales volume, but in structural operational efficiency. CATL reported 2025 revenues of $58.95 billion (a 17.04% increase), underpinned by an astonishing 96.9% capacity utilization rate. This near-maximum utilization dilutes fixed costs, enabling a highly defensive comprehensive unit cost of approximately $65.75/kWh.

Conversely, Samsung SDI’s energy solutions division suffered a 20.0% revenue contraction, pulling total revenues down to $9.33 billion. The strategic implication is clear: SDI is currently trapped in a structural CapEx dilemma. To comply with the U.S. Inflation Reduction Act (IRA), SDI is funneling massive capital into heavy-asset joint ventures with Stellantis and GM. However, a slowdown in Western EV adoption has left SDI grappling with unabsorbed fixed costs and severe asset impairment pressures. To fund this costly localized expansion, SDI was forced to liquidate non-core assets, including its polarizer business, to generate $788 million in liquidity.

Sector Positioning: The ESS "Safety Net" and Scenario Proliferation

The pure-play EV narrative is decelerating, shifting the battleground to Energy Storage Systems (ESS) and niche commercial applications. Here, CATL’s "full-domain increment" strategy has proven highly effective. Driven by the explosive power demands of AI data centers, CATL’s ESS battery sales hit 121 GWh (up 29.13% year-over-year), capitalizing on high-margin UPS and BBU deployments. Furthermore, CATL has successfully diversified into heavy-duty trucks, eVTOLs (electric vertical takeoff and landing aircraft) with its 500Wh/kg condensed battery, and marine applications, effectively insulating itself from passenger EV cyclicality.

Samsung SDI is attempting to pivot, accelerating the conversion of certain U.S. production lines to ESS formats to dilute idle capacity. However, SDI’s historical positioning as a "boutique" supplier to premium European automakers (like BMW and Volvo) means its product mix lacks the immediate, diversified scale required to fully offset the automotive downturn.

Strategic Moats: Geopolitical Navigation and Supply Chain Sovereignty

In 2025, geopolitical compliance is as critical as electrochemistry. The European Union’s carbon footprint regulations and U.S. localized manufacturing mandates have forced both companies to innovate their global expansion models.

CATL has engineered a sophisticated "LRS" (Licensing, Royalty, Service) model. By exporting patents and operational expertise to automakers like Ford and GM rather than taking direct equity stakes, CATL bypasses Foreign Entity of Concern (FEOC) restrictions. This asset-light approach secures high-margin royalty streams without the geopolitical risk of stranded CapEx. Simultaneously, CATL’s vertical integration—recovering 210,000 tons of battery materials in 2025—creates a closed-loop supply chain that inherently satisfies the EU’s strict zero-carbon and recycled material mandates.

Samsung SDI has opted for a "deep embedding" strategy, tying its fortunes to multi-billion-dollar localized JVs. While this ensures direct access to U.S. subsidies, it exposes the company to severe margin compression caused by elevated Western labor and energy costs, exacerbated by its reliance on external suppliers for up to 58% of its cathode materials.

HDIN Viewpoint: The Next 12 Months

From the perspective of HDIN Research, the 2025 landscape highlights a transition where profit pools are consolidating toward players with "full-domain ecosystem sovereignty." CATL is no longer just a battery manufacturer; it is evolving into a global zero-carbon infrastructure platform. Its ability to generate $18.53 billion in operating cash flow provides an insurmountable moat for aggressive R&D and multi-chemistry dominance (LFP, NCM, Sodium-ion).

Samsung SDI, meanwhile, is executing a high-stakes defensive strategy. By betting heavily on its upcoming 46-phi large cylindrical formats and All-Solid-State Batteries (ASB), SDI is attempting to leapfrog the current cost-war via technological disruption. However, until ASB reaches commercial maturity, SDI faces a precarious transitional period. For investors and industry stakeholders, the critical metric to watch over the next 12 months is not just GWh output, but the ratio of CapEx to actualized cash flow in localized Western facilities.

Presentation Download & Media Access

To dive deeper into the financial models and strategic frameworks discussed in this article:

* Presentation Download: Click the PDF download link under “Related Topics” to access the presentation of this report.

* Video Analysis: Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com