UBS 2025 Annual Report Analysis: Credit Suisse Integration Synergies and the Evolution of Strategic Moats

Date : 2026-03-13

Reading : 1015

In its first full fiscal year following the historic legal merger with Credit Suisse, UBS Group AG has demonstrated formidable operational execution, with net profit attributable to shareholders surging 139% year-over-year to $3.54 billion. However, as analyzed by HDIN Research, this headline figure is not merely a byproduct of prolonged consolidation timelines; rather, it reflects a profound structural transformation. By accelerating infrastructure decommissioning and optimizing its global footprint, UBS is rapidly converting integration costs into long-term operational efficiency, solidifying its position as the world's only truly global wealth manager.

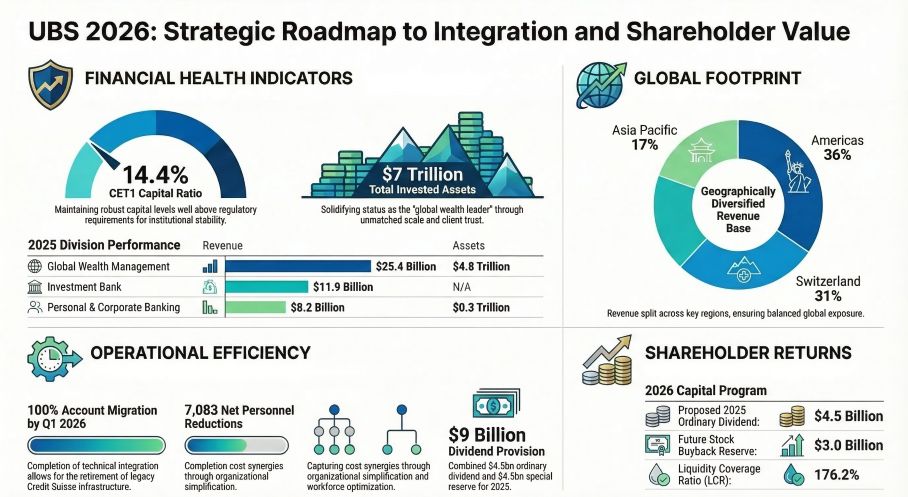

Figure UBS 2026: Strategic Roadmap to Integration and Shareholder Value

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

UBS’s 2025 financial posture illustrates a delicate balance between aggressive restructuring and robust shareholder returns. The bank improved its Cost/Income ratio to 90.2% (down from 93.0% in 2024), indicating that top-line revenue growth (13%) is beginning to outpace the sheer weight of its expanded operational footprint.

From a Capital Allocation Efficiency perspective, UBS’s Common Equity Tier 1 (CET1) capital ratio contracted slightly by 50 basis points to 14.4%. This contraction was not a signal of deteriorating fundamentals, but a deliberate allocation strategy: the bank earmarked a substantial $9 billion provision for dividends ($4.5 billion ordinary and a proposed $4.5 billion special dividend reserve) alongside a $3 billion share buyback reserve. While Return on Tangible Equity (RoTE) doubled to 4.0%, it remains suppressed by elevated short-term expenditures, pointing to significant upside potential as integration costs roll off in the coming years.

Strategic Pivots & Integration Synergies

The 2025 fiscal year was defined by critical Strategic Pivots aimed at capturing hard synergies. UBS actively engineered a leaner organizational structure, reducing its internal full-time equivalent (FTE) headcount by 7,083 and consolidating 95 domestic branches in Switzerland.

These personnel and physical footprint optimizations are the linchpins of UBS's cost synergy strategy. However, these gains required heavy upfront investment. The group absorbed $5.04 billion in net integration-related expenses in 2025. While these high integration costs temporarily dilute operating margins, they are accelerating the retirement of legacy IT architecture—evidenced by the successful migration of 85% of Swiss-booked Credit Suisse accounts. This decisive infrastructure sunsetting is expected to structurally lower the bank's long-term cost base.

Sector Positioning & The "Barbell" Moat

In terms of Sector Positioning, UBS has structured its operations into a highly effective "Barbell" model. On one end is the Global Wealth Management (GWM) division, a capital-light, highly recurrent fee-generating engine that contributed over 53% of group revenues ($25.4 billion) and manages an unprecedented $4.75 trillion in invested assets. On the other end are the Investment Bank (IB) and Personal & Corporate Banking (P&C) divisions, which act as capital-driven growth engines supporting the broader wealth ecosystem.

This model fortifies UBS's Strategic Moats in two distinct ways:

1. Unrivaled Geographic Diversification: Unlike its primary US-based rivals (such as Morgan Stanley and JPMorgan), which suffer from high Americas concentration, UBS boasts a highly balanced global footprint (Americas 36%, Switzerland 31%, EMEA 18%, APAC 17%). This geographic distribution significantly insulates the bank from regional macroeconomic shocks.

2. Domestic Monopoly Power: Within Switzerland, UBS has cemented absolute dominance over local cantonal banks (e.g., ZKB) and cooperative banks (e.g., Raiffeisen). As the sole remaining Swiss universal bank with unparalleled cross-border corporate capabilities, UBS serves over 90% of large Swiss corporations, creating high switching costs and formidable barriers to entry.

Cyclical Headwinds & Regulatory Pressures

Despite its dominant market position, UBS must navigate significant Cyclical Headwinds and emerging regulatory risks. The transition from a rising interest rate environment to a stabilized low-rate paradigm presents challenges to Net Interest Income (NII) growth. While UBS maintains positive rate sensitivity, the normalization of the Swiss National Bank's rate policies is steadily eroding deposit margins.

More critically, the bank faces a looming regulatory "gray rhino." Proposed revisions to the Swiss "Too Big To Fail" (TBTF) framework—specifically the requirement to fully deduct capital backing foreign subsidiaries—could mandate an estimated $22 billion to $37 billion in additional CET1 capital. If enacted, these stringent regulatory capital requirements could structurally cap UBS’s global Return on Equity (RoE) relative to its international peers.

HDIN Viewpoint

HDIN Research assesses that UBS’s 2025 performance is a masterclass in trading short-term profitability for long-term unassailable market dominance. The absorption of $5 billion in integration costs is a calculated investment to purge legacy inefficiencies and achieve an end-to-end global wealth platform. As the bank enters 2026—the stated deadline for substantive integration completion—the true barometer of success will not just be cost reduction, but client retention post-platform migration. Investors and institutional stakeholders must closely monitor the unfolding Swiss regulatory landscape, as this will ultimately dictate the ceiling for UBS's future capital distribution and structural profitability.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure UBS 2026: Strategic Roadmap to Integration and Shareholder Value

Financial Health & Capital Allocation EfficiencyUBS’s 2025 financial posture illustrates a delicate balance between aggressive restructuring and robust shareholder returns. The bank improved its Cost/Income ratio to 90.2% (down from 93.0% in 2024), indicating that top-line revenue growth (13%) is beginning to outpace the sheer weight of its expanded operational footprint.

From a Capital Allocation Efficiency perspective, UBS’s Common Equity Tier 1 (CET1) capital ratio contracted slightly by 50 basis points to 14.4%. This contraction was not a signal of deteriorating fundamentals, but a deliberate allocation strategy: the bank earmarked a substantial $9 billion provision for dividends ($4.5 billion ordinary and a proposed $4.5 billion special dividend reserve) alongside a $3 billion share buyback reserve. While Return on Tangible Equity (RoTE) doubled to 4.0%, it remains suppressed by elevated short-term expenditures, pointing to significant upside potential as integration costs roll off in the coming years.

Strategic Pivots & Integration Synergies

The 2025 fiscal year was defined by critical Strategic Pivots aimed at capturing hard synergies. UBS actively engineered a leaner organizational structure, reducing its internal full-time equivalent (FTE) headcount by 7,083 and consolidating 95 domestic branches in Switzerland.

These personnel and physical footprint optimizations are the linchpins of UBS's cost synergy strategy. However, these gains required heavy upfront investment. The group absorbed $5.04 billion in net integration-related expenses in 2025. While these high integration costs temporarily dilute operating margins, they are accelerating the retirement of legacy IT architecture—evidenced by the successful migration of 85% of Swiss-booked Credit Suisse accounts. This decisive infrastructure sunsetting is expected to structurally lower the bank's long-term cost base.

Sector Positioning & The "Barbell" Moat

In terms of Sector Positioning, UBS has structured its operations into a highly effective "Barbell" model. On one end is the Global Wealth Management (GWM) division, a capital-light, highly recurrent fee-generating engine that contributed over 53% of group revenues ($25.4 billion) and manages an unprecedented $4.75 trillion in invested assets. On the other end are the Investment Bank (IB) and Personal & Corporate Banking (P&C) divisions, which act as capital-driven growth engines supporting the broader wealth ecosystem.

This model fortifies UBS's Strategic Moats in two distinct ways:

1. Unrivaled Geographic Diversification: Unlike its primary US-based rivals (such as Morgan Stanley and JPMorgan), which suffer from high Americas concentration, UBS boasts a highly balanced global footprint (Americas 36%, Switzerland 31%, EMEA 18%, APAC 17%). This geographic distribution significantly insulates the bank from regional macroeconomic shocks.

2. Domestic Monopoly Power: Within Switzerland, UBS has cemented absolute dominance over local cantonal banks (e.g., ZKB) and cooperative banks (e.g., Raiffeisen). As the sole remaining Swiss universal bank with unparalleled cross-border corporate capabilities, UBS serves over 90% of large Swiss corporations, creating high switching costs and formidable barriers to entry.

Cyclical Headwinds & Regulatory Pressures

Despite its dominant market position, UBS must navigate significant Cyclical Headwinds and emerging regulatory risks. The transition from a rising interest rate environment to a stabilized low-rate paradigm presents challenges to Net Interest Income (NII) growth. While UBS maintains positive rate sensitivity, the normalization of the Swiss National Bank's rate policies is steadily eroding deposit margins.

More critically, the bank faces a looming regulatory "gray rhino." Proposed revisions to the Swiss "Too Big To Fail" (TBTF) framework—specifically the requirement to fully deduct capital backing foreign subsidiaries—could mandate an estimated $22 billion to $37 billion in additional CET1 capital. If enacted, these stringent regulatory capital requirements could structurally cap UBS’s global Return on Equity (RoE) relative to its international peers.

HDIN Viewpoint

HDIN Research assesses that UBS’s 2025 performance is a masterclass in trading short-term profitability for long-term unassailable market dominance. The absorption of $5 billion in integration costs is a calculated investment to purge legacy inefficiencies and achieve an end-to-end global wealth platform. As the bank enters 2026—the stated deadline for substantive integration completion—the true barometer of success will not just be cost reduction, but client retention post-platform migration. Investors and institutional stakeholders must closely monitor the unfolding Swiss regulatory landscape, as this will ultimately dictate the ceiling for UBS's future capital distribution and structural profitability.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com