Samsung Electronics 2025 Financial Review: AI Supply Chain Realignment and Silicon Supremacy

Date : 2026-03-12

Reading : 6324

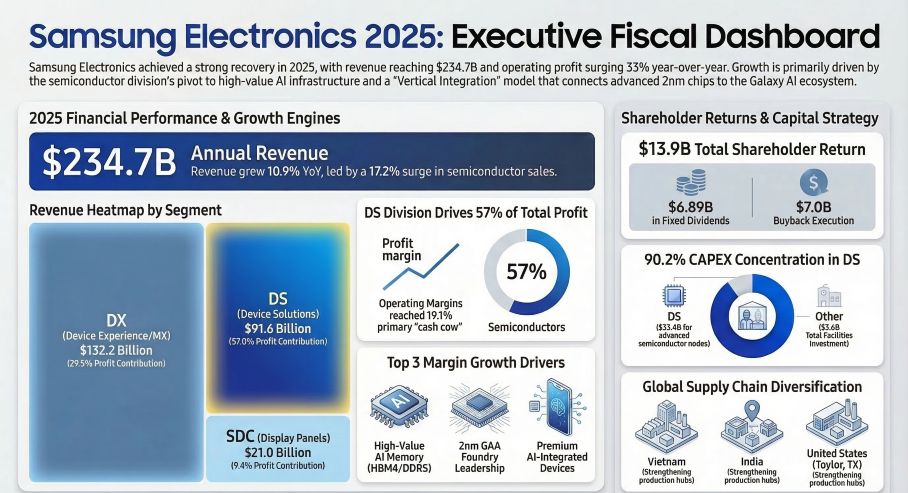

Following a period of cyclical industry adjustments, Samsung Electronics has engineered a robust financial recovery in FY2025, posting $234.7 billion in total revenue (up 10.9% YoY) and a formidable 33.2% surge in operating profit to $30.67 billion. According to HDIN Research, this performance is not merely a cyclical rebound, but the result of a deliberate strategic pivot. By leveraging its vertical integration capabilities, Samsung is capturing new value pools in the AI infrastructure boom, aggressively defending its silicon moats while rearchitecting its global supply chain.

Figure Samsung Electronics 2025: Executive Fiscal Dashboard

Capital Allocation Efficiency: The $37 Billion Pivot

Capital Allocation Efficiency: The $37 Billion Pivot

From a capital efficiency standpoint, Samsung has successfully transitioned from inventory crisis management to aggressive forward-looking investments. The company’s Free Cash Flow (FCF) experienced a dramatic turnaround, reaching $23.33 billion in 2025.

Instead of broad-based expansion, management exhibited extreme strategic concentration in its capital allocation. Of the $37.04 billion total capital expenditure (CAPEX) for the year, a staggering 90.2% was directed to the Device Solutions (DS) segment. This high-intensity funding is specifically targeted at breaking technological bottlenecks—namely, the mass production of next-generation HBM4 base-dies and 2nm Gate-All-Around (GAA) advanced foundry nodes. This concentrated CAPEX forms a robust financial moat, enabling Samsung to accelerate its R&D cycle (backed by a record $26.56 billion R&D budget) and challenge competitors like TSMC and SK Hynix in the advanced compute arena.

Sector Positioning: Profit Pools Shift from Devices to Components

An analysis of Samsung’s segment performance reveals a stark divergence in value capture between hardware assembly and core components.

The Device eXperience (DX) division remained the topline revenue driver, contributing 56.3% of total sales. However, margin compression—driven by rising mobile AP chip costs and aggressive market competition—pushed the DX operating margin down to 6.8%. Conversely, the Device Solutions (DS) division emerged as the definitive profit engine. Generating 57.0% of the corporate operating profit on just 39.0% of total revenue, the DS segment achieved a lucrative 19.1% margin.

The "So What" factor here lies in the pricing power dynamics. While smartphone Average Selling Prices (ASP) contracted by 3% due to mid-tier volume shifts and inventory clearing, memory chip ASPs surged by 14%. This asymmetry underscores how data center demand for high-density DDR5 and enterprise SSDs is currently dictating the semiconductor value chain, vindicating Samsung's heavy CAPEX tilt toward silicon.

Strategic Moats: Vertical Integration in the AI Era

Samsung is redefining its sector positioning from a component manufacturer to a full-stack AI hardware ecosystem provider. Its strategic moat lies in end-to-end vertical integration—a capability unmatched by pure-play foundries or fabless designers.

In 2025, Samsung fortified this moat through synergistic M&A and product integration. The acquisition of Rainbow Robotics (20.3% stake) and US digital health platform Xealth Inc. signals an aggressive push into multi-modal AI and connected care. At the device level, the proprietary "Samsung Gauss" generative AI model has been deeply embedded into the Galaxy S25 series and AI home appliances. By internally supplying the 2nm Exynos 2600 processors and 9th-generation V-NAND required to run these on-device AI operations, Samsung effectively insulates its hardware margins from external supply chain shocks.

Cyclical Headwinds and Geopolitical Realignment

Despite a fortress-like balance sheet featuring $70.78 billion in net cash, Samsung faces distinct cyclical headwinds and geopolitical risks.

Competitively, Samsung’s DRAM market share contracted from 41.5% in 2024 to 34.0% in 2025. This erosion highlights the intense first-mover advantage seized by rivals in the high-margin HBM3E space, indicating that Samsung must flawlessly execute its 2026 HBM4 rollout to reclaim market dominance.

Simultaneously, the company is navigating a complex geopolitical landscape. To mitigate risks of trade protectionism and tariff volatility, Samsung is solidifying a geographically diverse operational triangle: "Korea R&D - Vietnam/India Assembly - Americas Consumption". The aggressive build-out of the Taylor, Texas foundry—backed by a $6.4 billion payment guarantee from the parent company—demonstrates a strategic nearshoring effort to secure US HPC and AI chip clients amid rising geopolitical fragmentation.

HDIN Viewpoint

HDIN Research assesses that Samsung Electronics is currently in a transitional phase of "premiumization" across its portfolio. The 2025 financial data proves that its core operations are highly resilient, but the structural drop in DRAM market share serves as a warning sign regarding technology-to-market execution speeds. Looking ahead to 2026, Samsung's valuation multiple will largely depend on two catalysts: the commercial validation of its 2nm GAA yields to capture external foundry market share, and its ability to close the HBM interposer technology gap. For institutional investors and supply chain partners, Samsung’s $70 billion net cash position provides an exceptionally wide margin of safety as the company finances its way back to silicon supremacy.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Samsung Electronics 2025: Executive Fiscal Dashboard

Capital Allocation Efficiency: The $37 Billion PivotFrom a capital efficiency standpoint, Samsung has successfully transitioned from inventory crisis management to aggressive forward-looking investments. The company’s Free Cash Flow (FCF) experienced a dramatic turnaround, reaching $23.33 billion in 2025.

Instead of broad-based expansion, management exhibited extreme strategic concentration in its capital allocation. Of the $37.04 billion total capital expenditure (CAPEX) for the year, a staggering 90.2% was directed to the Device Solutions (DS) segment. This high-intensity funding is specifically targeted at breaking technological bottlenecks—namely, the mass production of next-generation HBM4 base-dies and 2nm Gate-All-Around (GAA) advanced foundry nodes. This concentrated CAPEX forms a robust financial moat, enabling Samsung to accelerate its R&D cycle (backed by a record $26.56 billion R&D budget) and challenge competitors like TSMC and SK Hynix in the advanced compute arena.

Sector Positioning: Profit Pools Shift from Devices to Components

An analysis of Samsung’s segment performance reveals a stark divergence in value capture between hardware assembly and core components.

The Device eXperience (DX) division remained the topline revenue driver, contributing 56.3% of total sales. However, margin compression—driven by rising mobile AP chip costs and aggressive market competition—pushed the DX operating margin down to 6.8%. Conversely, the Device Solutions (DS) division emerged as the definitive profit engine. Generating 57.0% of the corporate operating profit on just 39.0% of total revenue, the DS segment achieved a lucrative 19.1% margin.

The "So What" factor here lies in the pricing power dynamics. While smartphone Average Selling Prices (ASP) contracted by 3% due to mid-tier volume shifts and inventory clearing, memory chip ASPs surged by 14%. This asymmetry underscores how data center demand for high-density DDR5 and enterprise SSDs is currently dictating the semiconductor value chain, vindicating Samsung's heavy CAPEX tilt toward silicon.

Strategic Moats: Vertical Integration in the AI Era

Samsung is redefining its sector positioning from a component manufacturer to a full-stack AI hardware ecosystem provider. Its strategic moat lies in end-to-end vertical integration—a capability unmatched by pure-play foundries or fabless designers.

In 2025, Samsung fortified this moat through synergistic M&A and product integration. The acquisition of Rainbow Robotics (20.3% stake) and US digital health platform Xealth Inc. signals an aggressive push into multi-modal AI and connected care. At the device level, the proprietary "Samsung Gauss" generative AI model has been deeply embedded into the Galaxy S25 series and AI home appliances. By internally supplying the 2nm Exynos 2600 processors and 9th-generation V-NAND required to run these on-device AI operations, Samsung effectively insulates its hardware margins from external supply chain shocks.

Cyclical Headwinds and Geopolitical Realignment

Despite a fortress-like balance sheet featuring $70.78 billion in net cash, Samsung faces distinct cyclical headwinds and geopolitical risks.

Competitively, Samsung’s DRAM market share contracted from 41.5% in 2024 to 34.0% in 2025. This erosion highlights the intense first-mover advantage seized by rivals in the high-margin HBM3E space, indicating that Samsung must flawlessly execute its 2026 HBM4 rollout to reclaim market dominance.

Simultaneously, the company is navigating a complex geopolitical landscape. To mitigate risks of trade protectionism and tariff volatility, Samsung is solidifying a geographically diverse operational triangle: "Korea R&D - Vietnam/India Assembly - Americas Consumption". The aggressive build-out of the Taylor, Texas foundry—backed by a $6.4 billion payment guarantee from the parent company—demonstrates a strategic nearshoring effort to secure US HPC and AI chip clients amid rising geopolitical fragmentation.

HDIN Viewpoint

HDIN Research assesses that Samsung Electronics is currently in a transitional phase of "premiumization" across its portfolio. The 2025 financial data proves that its core operations are highly resilient, but the structural drop in DRAM market share serves as a warning sign regarding technology-to-market execution speeds. Looking ahead to 2026, Samsung's valuation multiple will largely depend on two catalysts: the commercial validation of its 2nm GAA yields to capture external foundry market share, and its ability to close the HBM interposer technology gap. For institutional investors and supply chain partners, Samsung’s $70 billion net cash position provides an exceptionally wide margin of safety as the company finances its way back to silicon supremacy.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com