2025 Global Energy Giants: Strategic Moats, Capital Allocation, and Structural Divergence

Date : 2026-03-16

Reading : 346

The global energy sector in 2025 has officially transitioned from a period of high-commodity-price dividends to an era dictated by operational efficiency and asset optimization. Amidst a complex macroeconomic backdrop—characterized by Brent crude prices resetting to an average of $69.10 per barrel and a global supply surplus of approximately 2.2 million barrels per day—industry leaders are experiencing extreme structural divergence.

Based on an exhaustive forensic and strategic analysis of 2025 financial disclosures from Saudi Aramco, Chevron, BP, Phillips 66, and IRPC, HDIN Research reveals that top-line revenue no longer guarantees bottom-line resilience. Instead, sector positioning, absolute cost advantages, and ruthless capital discipline are separating the resilient cash cows from the vulnerable regional players.

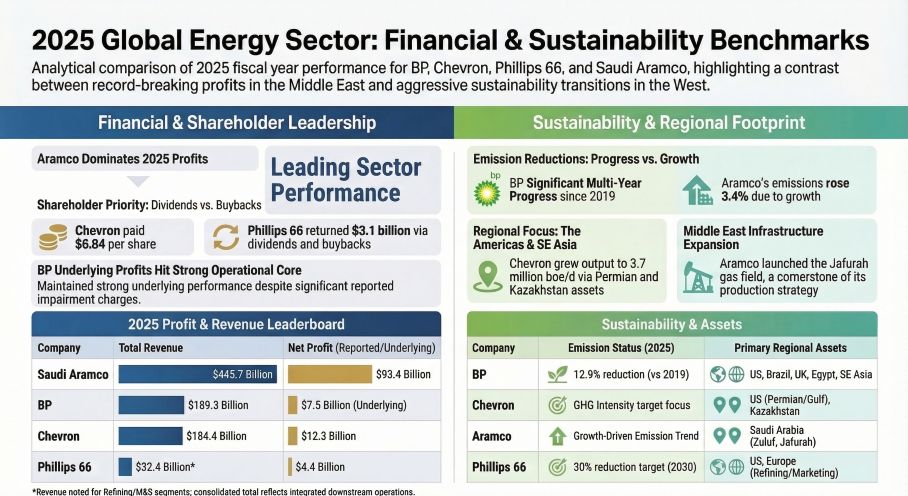

Figure 2025 Global Energy Sector: Financial & Sustainability Benchmarks

Sector Positioning and Cyclical Headwinds

Sector Positioning and Cyclical Headwinds

In 2025, macroeconomic realities and stringent policy frameworks have coalesced into severe cyclical headwinds, particularly for downstream operators. Global demand reached a record 1.04–1.06 million barrels per day, yet the simultaneous production surge from non-OPEC+ and OPEC+ members has compressed baseline pricing.

Simultaneously, regional policy disparities are reshaping sector positioning. In Europe and the UK, punitive tax structures—such as the UK’s 78% Energy Profits Levy (EPL) and the EU’s Carbon Border Adjustment Mechanism (CBAM)—are placing hard ceilings on operational margins. In the Asia-Pacific region, massive petrochemical capacity expansions, particularly from China, have resulted in a structural oversupply. This dynamic has severely squeezed refining margins, pushing regional players like Thailand’s IRPC into negative territory with a net margin of -0.92%.

Strategic Moats: Resource Monopoly vs. Value Chain Integration

To navigate the energy transition and cyclical volatility, energy giants are relying on vastly different strategic moats.

* Absolute Cost Leadership (Saudi Aramco): Aramco maintains an unparalleled defensive moat. With a global-low lifting cost of just $3.51 per barrel of oil equivalent (boe) and a Maximum Sustainable Capacity (MSC) of 12 million barrels per day, the company generated a staggering $85.4 billion in free cash flow. By vertically integrating 53% of its upstream output into its proprietary downstream network, Aramco successfully insulates itself against raw crude volatility, cementing its status as the industry's ultimate cash cow.

* M&A-Driven Volume and Resilience (Chevron): Chevron has leveraged strategic acquisitions, notably the integration of Hess, to secure top-tier market share in the Permian Basin and Guyana. This aggressive upstream expansion drove a 12% year-over-year production increase to 3.7 million barrels per day, lowering its breakeven threshold and ensuring robust cash flow generation even at a $60/bbl stress-test level.

* Midstream and Downstream Synergies (Phillips 66): Lacking an upstream buffer, Phillips 66 relies entirely on its "wellhead-to-market" natural gas liquids (NGL) value chain. While it successfully captures crack spread premiums, its 2025 profit growth was heavily distorted by a $2.9 billion one-off gain from European asset disposals, highlighting the inherent vulnerabilities of a pure downstream model during inflationary cycles.

Capital Allocation Efficiency and Financial Health

A critical forensic review of 2025 financials by HDIN Research indicates a sector-wide pivot away from "growth-at-all-costs" green investments toward rigorous capital allocation efficiency and balance sheet optimization.

* Strategic Write-Downs and Transition Pains (BP): BP’s statutory profit of just $100 million in 2025 was masked by a massive $5.4 billion net impairment, primarily targeting renewable assets like Lightsource bp and Archaea Energy. This aggressive "big bath" accounting approach under new leadership reflects a strategic reset—clearing out overvalued early-stage transition assets to artificially reduce future depreciation burdens and boost long-term Return on Average Capital Employed (ROACE). Furthermore, BP’s suspension of share buybacks underscores the intense capital demands required to manage its $22.2 billion net debt.

* Balance Sheet Fortresses: Conversely, Saudi Aramco boasts an ultra-low gearing ratio of 3.8%, while Chevron maintains a highly manageable 17.9% gearing despite assuming $10 billion in debt from the Hess acquisition. Chevron's operating cash flow-to-net profit ratio of 2.76x demonstrates the highest earnings quality among Western peers, driven by genuine operational cash generation rather than paper gains.

HDIN Viewpoint: The Imperative of Upstream Resilience

From the perspective of HDIN Research, 2025 is a watershed year that punishes structural exposure. The market has bifurcated: companies with deep upstream cost moats and cross-regional asset portfolios are insulated from localized geopolitical shocks (such as potential Strait of Hormuz disruptions) and demand destruction.

Conversely, downstream refiners lacking distinct technological barriers or specialty chemical integration are facing an existential margin crisis. As the energy transition matures, capital allocation efficiency—specifically the ability to balance high-yield hydrocarbon defense with selective, value-accretive low-carbon investments—will be the sole determinant of premium valuations over the next three to five years.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Based on an exhaustive forensic and strategic analysis of 2025 financial disclosures from Saudi Aramco, Chevron, BP, Phillips 66, and IRPC, HDIN Research reveals that top-line revenue no longer guarantees bottom-line resilience. Instead, sector positioning, absolute cost advantages, and ruthless capital discipline are separating the resilient cash cows from the vulnerable regional players.

Figure 2025 Global Energy Sector: Financial & Sustainability Benchmarks

Sector Positioning and Cyclical HeadwindsIn 2025, macroeconomic realities and stringent policy frameworks have coalesced into severe cyclical headwinds, particularly for downstream operators. Global demand reached a record 1.04–1.06 million barrels per day, yet the simultaneous production surge from non-OPEC+ and OPEC+ members has compressed baseline pricing.

Simultaneously, regional policy disparities are reshaping sector positioning. In Europe and the UK, punitive tax structures—such as the UK’s 78% Energy Profits Levy (EPL) and the EU’s Carbon Border Adjustment Mechanism (CBAM)—are placing hard ceilings on operational margins. In the Asia-Pacific region, massive petrochemical capacity expansions, particularly from China, have resulted in a structural oversupply. This dynamic has severely squeezed refining margins, pushing regional players like Thailand’s IRPC into negative territory with a net margin of -0.92%.

Strategic Moats: Resource Monopoly vs. Value Chain Integration

To navigate the energy transition and cyclical volatility, energy giants are relying on vastly different strategic moats.

* Absolute Cost Leadership (Saudi Aramco): Aramco maintains an unparalleled defensive moat. With a global-low lifting cost of just $3.51 per barrel of oil equivalent (boe) and a Maximum Sustainable Capacity (MSC) of 12 million barrels per day, the company generated a staggering $85.4 billion in free cash flow. By vertically integrating 53% of its upstream output into its proprietary downstream network, Aramco successfully insulates itself against raw crude volatility, cementing its status as the industry's ultimate cash cow.

* M&A-Driven Volume and Resilience (Chevron): Chevron has leveraged strategic acquisitions, notably the integration of Hess, to secure top-tier market share in the Permian Basin and Guyana. This aggressive upstream expansion drove a 12% year-over-year production increase to 3.7 million barrels per day, lowering its breakeven threshold and ensuring robust cash flow generation even at a $60/bbl stress-test level.

* Midstream and Downstream Synergies (Phillips 66): Lacking an upstream buffer, Phillips 66 relies entirely on its "wellhead-to-market" natural gas liquids (NGL) value chain. While it successfully captures crack spread premiums, its 2025 profit growth was heavily distorted by a $2.9 billion one-off gain from European asset disposals, highlighting the inherent vulnerabilities of a pure downstream model during inflationary cycles.

Capital Allocation Efficiency and Financial Health

A critical forensic review of 2025 financials by HDIN Research indicates a sector-wide pivot away from "growth-at-all-costs" green investments toward rigorous capital allocation efficiency and balance sheet optimization.

* Strategic Write-Downs and Transition Pains (BP): BP’s statutory profit of just $100 million in 2025 was masked by a massive $5.4 billion net impairment, primarily targeting renewable assets like Lightsource bp and Archaea Energy. This aggressive "big bath" accounting approach under new leadership reflects a strategic reset—clearing out overvalued early-stage transition assets to artificially reduce future depreciation burdens and boost long-term Return on Average Capital Employed (ROACE). Furthermore, BP’s suspension of share buybacks underscores the intense capital demands required to manage its $22.2 billion net debt.

* Balance Sheet Fortresses: Conversely, Saudi Aramco boasts an ultra-low gearing ratio of 3.8%, while Chevron maintains a highly manageable 17.9% gearing despite assuming $10 billion in debt from the Hess acquisition. Chevron's operating cash flow-to-net profit ratio of 2.76x demonstrates the highest earnings quality among Western peers, driven by genuine operational cash generation rather than paper gains.

HDIN Viewpoint: The Imperative of Upstream Resilience

From the perspective of HDIN Research, 2025 is a watershed year that punishes structural exposure. The market has bifurcated: companies with deep upstream cost moats and cross-regional asset portfolios are insulated from localized geopolitical shocks (such as potential Strait of Hormuz disruptions) and demand destruction.

Conversely, downstream refiners lacking distinct technological barriers or specialty chemical integration are facing an existential margin crisis. As the energy transition matures, capital allocation efficiency—specifically the ability to balance high-yield hydrocarbon defense with selective, value-accretive low-carbon investments—will be the sole determinant of premium valuations over the next three to five years.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com