Jiadeli’s Strategic Pivot: Navigating Ultra-Thin Film Moats and Supply Chain Headwinds

Date : 2026-03-16

Reading : 203

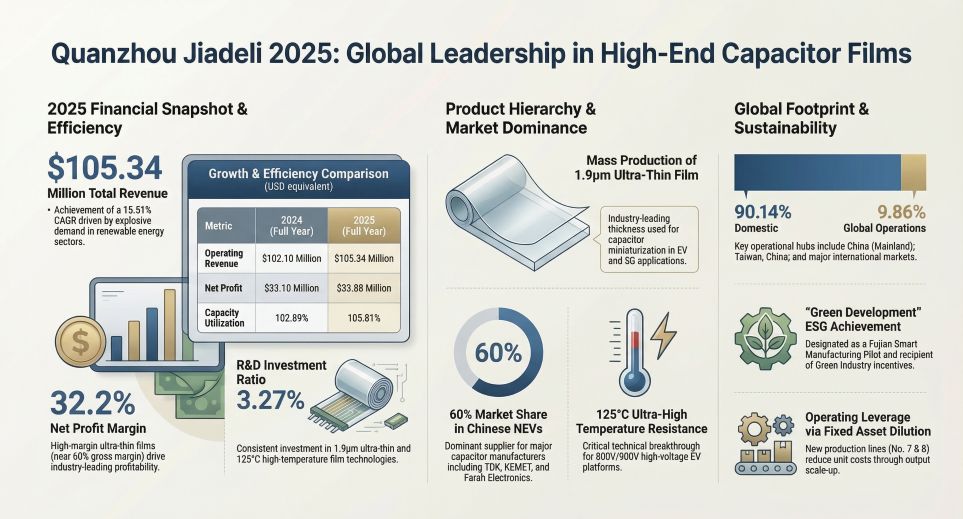

Quanzhou Jiadeli Electronic Materials Co., Ltd. has firmly established itself as a hidden champion within the global BOPP (Biaxially Oriented Polypropylene) capacitor film sector. Operating at a relentless 102.89% capacity utilization rate, the company has transformed its revenue profile by pivoting toward ultra-thin films engineered for the electric vehicle (EV) and renewable energy markets. However, beneath its robust 15.51% revenue compound annual growth rate (CAGR) lies a complex strategic narrative. HDIN Research’s latest analysis reveals that while Jiadeli commands immense pricing power through domestic substitution, its long-term capital allocation efficiency must be carefully balanced against highly concentrated, cyclical supply chain vulnerabilities.

Figure Quanzhou Jiadeli 2025: Clobal Leadership in High-End Capacitor Films

Sector Positioning: The "Substitution Premium" and Strategic Moats

Sector Positioning: The "Substitution Premium" and Strategic Moats

Jiadeli has successfully transcended the "low-cost alternative" phase, establishing formidable strategic moats in the high-end materials space. By achieving stable mass production of 1.9µm ultra-thin films and pioneering the commercialization of 125℃ ultra-temperature resistant films for Silicon Carbide (SiC) modules, Jiadeli has effectively disrupted the oligopoly historically held by international giants like Japan’s Toray.

The strategic implication of this technological leap is profound pricing power. In 2024, Jiadeli’s ultra-thin film (≤3.4μm) commanded an average selling price of approximately $9,280 per ton, yielding a staggering 57.71% gross margin—far exceeding the domestic industry average of 32.88%. This premium indicates that Jiadeli is no longer competing on price; rather, it is capturing value through physical limit manufacturing that enables downstream clients to miniaturize capacitors and reduce overall material volume.

Financial Health and Capital Allocation Efficiency

Financially, Jiadeli demonstrates high-quality earnings, with 2024 revenue reaching $102.10 million and a core operating profit margin of roughly 37.77%. A critical driver of its future profitability lies in operating leverage. Currently, fixed asset depreciation accounts for nearly 10.93% of the company's Cost of Goods Sold (COGS).

To alleviate its capacity bottlenecks, Jiadeli is executing a massive capital allocation strategy, aiming to raise approximately $100.87 million primarily for its Xiamen New Material Base (adding 7,500 tons of capacity). While this aggressive Capex cycle poses a short-term risk of ROE dilution over the three-year construction phase, the strategic payoff is significant. As new production lines ramp up, the marginal increase in output will aggressively dilute unit fixed costs. HDIN Research projects that every 10% increase in capacity utilization on the new lines could directly inject a 1-2 percentage point net increase in gross profit, assuming raw material stability.

Cyclical Headwinds and Supply Chain Vulnerabilities

Despite its technological dominance, Jiadeli’s cost structure reveals acute exposure to cyclical headwinds. Direct materials—primarily electrical-grade polypropylene resin—constitute nearly 74% of its COGS. Compounding this risk is an extreme vendor concentration: over 90% of its critical resin is imported from a single European supplier (Borouge/Borealis) via the Cape of Good Hope.

To mitigate these geopolitical and logistical black swans, Jiadeli maintains a strategic inventory buffer of 120-140 days. While this long-cycle inventory strategy provides a robust shock absorber during early-stage price surges in the petroleum-linked resin market, it creates a lagging "scissor effect" during price downturns, inevitably compressing gross margins as high-cost inventory is cleared against lowered product selling prices.

Furthermore, yield rate optimization—rather than downstream price hikes—serves as Jiadeli’s ultimate cost hedge. Because the ultra-thin film manufacturing process is prone to high breakage rates, any marginal improvement in production yield directly offsets raw material inflation while simultaneously diluting fixed manufacturing overhead.

HDIN Viewpoint: The Profitability vs. Resilience Paradox

From an institutional perspective, HDIN Research views Jiadeli as a company characterized by a "technological stronghold but a supply chain paradox." It commands exceptional profit margins from tier-one EV and renewable energy clients, yet it remains financially passive in the broader value chain. This is evidenced by extending accounts receivable turnover (dropping to 5.20x in 2024) as downstream automotive giants enforce supply chain finance settlement terms.

Jiadeli’s ultimate test will not be its ability to sell ultra-thin films—the market demand is structurally guaranteed by the EV transition. Rather, its long-term valuation will be dictated by how swiftly it can localize its upstream resin supply (e.g., its ongoing initiatives with the State Grid) and reduce its reliance on imported European production equipment. Until full supply chain autonomy is achieved, investors must weigh its exceptional operating leverage against the unquantifiable risks of global shipping disruptions.

Presentation download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Quanzhou Jiadeli 2025: Clobal Leadership in High-End Capacitor Films

Sector Positioning: The "Substitution Premium" and Strategic MoatsJiadeli has successfully transcended the "low-cost alternative" phase, establishing formidable strategic moats in the high-end materials space. By achieving stable mass production of 1.9µm ultra-thin films and pioneering the commercialization of 125℃ ultra-temperature resistant films for Silicon Carbide (SiC) modules, Jiadeli has effectively disrupted the oligopoly historically held by international giants like Japan’s Toray.

The strategic implication of this technological leap is profound pricing power. In 2024, Jiadeli’s ultra-thin film (≤3.4μm) commanded an average selling price of approximately $9,280 per ton, yielding a staggering 57.71% gross margin—far exceeding the domestic industry average of 32.88%. This premium indicates that Jiadeli is no longer competing on price; rather, it is capturing value through physical limit manufacturing that enables downstream clients to miniaturize capacitors and reduce overall material volume.

Financial Health and Capital Allocation Efficiency

Financially, Jiadeli demonstrates high-quality earnings, with 2024 revenue reaching $102.10 million and a core operating profit margin of roughly 37.77%. A critical driver of its future profitability lies in operating leverage. Currently, fixed asset depreciation accounts for nearly 10.93% of the company's Cost of Goods Sold (COGS).

To alleviate its capacity bottlenecks, Jiadeli is executing a massive capital allocation strategy, aiming to raise approximately $100.87 million primarily for its Xiamen New Material Base (adding 7,500 tons of capacity). While this aggressive Capex cycle poses a short-term risk of ROE dilution over the three-year construction phase, the strategic payoff is significant. As new production lines ramp up, the marginal increase in output will aggressively dilute unit fixed costs. HDIN Research projects that every 10% increase in capacity utilization on the new lines could directly inject a 1-2 percentage point net increase in gross profit, assuming raw material stability.

Cyclical Headwinds and Supply Chain Vulnerabilities

Despite its technological dominance, Jiadeli’s cost structure reveals acute exposure to cyclical headwinds. Direct materials—primarily electrical-grade polypropylene resin—constitute nearly 74% of its COGS. Compounding this risk is an extreme vendor concentration: over 90% of its critical resin is imported from a single European supplier (Borouge/Borealis) via the Cape of Good Hope.

To mitigate these geopolitical and logistical black swans, Jiadeli maintains a strategic inventory buffer of 120-140 days. While this long-cycle inventory strategy provides a robust shock absorber during early-stage price surges in the petroleum-linked resin market, it creates a lagging "scissor effect" during price downturns, inevitably compressing gross margins as high-cost inventory is cleared against lowered product selling prices.

Furthermore, yield rate optimization—rather than downstream price hikes—serves as Jiadeli’s ultimate cost hedge. Because the ultra-thin film manufacturing process is prone to high breakage rates, any marginal improvement in production yield directly offsets raw material inflation while simultaneously diluting fixed manufacturing overhead.

HDIN Viewpoint: The Profitability vs. Resilience Paradox

From an institutional perspective, HDIN Research views Jiadeli as a company characterized by a "technological stronghold but a supply chain paradox." It commands exceptional profit margins from tier-one EV and renewable energy clients, yet it remains financially passive in the broader value chain. This is evidenced by extending accounts receivable turnover (dropping to 5.20x in 2024) as downstream automotive giants enforce supply chain finance settlement terms.

Jiadeli’s ultimate test will not be its ability to sell ultra-thin films—the market demand is structurally guaranteed by the EV transition. Rather, its long-term valuation will be dictated by how swiftly it can localize its upstream resin supply (e.g., its ongoing initiatives with the State Grid) and reduce its reliance on imported European production equipment. Until full supply chain autonomy is achieved, investors must weigh its exceptional operating leverage against the unquantifiable risks of global shipping disruptions.

Presentation download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com