Glencore 2025 Strategy: The Copper Pivot, Arbitrage Moats, and Pragmatic Energy Transition

Date : 2026-03-16

Reading : 490

Glencore’s 2025 financial and operational performance delivers a masterclass in transitional capital allocation. Rather than succumbing to cyclical headwinds in the global energy market, the commodity giant is successfully leveraging the robust cash flow of its legacy coal assets to bankroll an aggressive pivot toward copper and green energy metals. Coupled with its formidable marketing division, Glencore has engineered a highly resilient "production plus trade" business model that effectively neutralizes macroeconomic volatility.

Figure Glencore 2025: A Global Value Chain in Transition

Here is HDIN Research’s in-depth analysis of Glencore’s 2025 strategic positioning, financial health, and risk architecture.

Here is HDIN Research’s in-depth analysis of Glencore’s 2025 strategic positioning, financial health, and risk architecture.

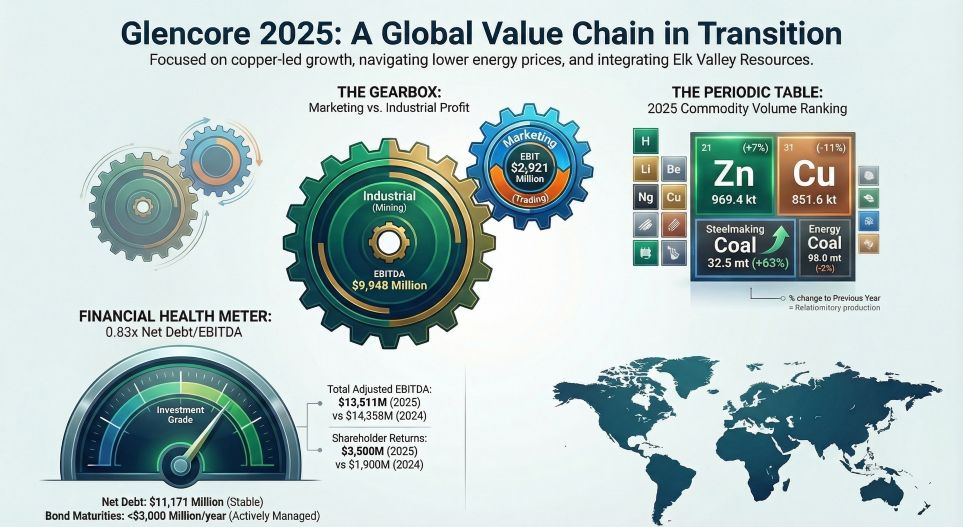

Financial Resilience & The "Marketing" Moat

In 2025, Glencore demonstrated the structural asymmetry of its business model compared to pure-play mining peers like BHP or Rio Tinto. While the Industrial division faced cyclical headwinds—primarily a 23% drop in Newcastle thermal coal benchmark prices—resulting in a 6% year-over-year decline in Adjusted EBITDA to $13.51 billion, the company’s unique architecture provided a critical buffer.

The Marketing division acts as a highly effective hedge against commodity price volatility. Utilizing sophisticated geographical, product, and time arbitrage, the marketing arm delivered $2.92 billion in Adjusted EBIT. When energy margins compressed, metal trading (capitalizing on a 44% intra-year copper price surge and regional supply chain bottlenecks) generated record-level returns. This dual-engine model allows Glencore to earn "fee-like" income during market downturns, maintaining a pristine balance sheet with a net debt-to-Adjusted EBITDA ratio of just 0.83x, well below the company’s 2.0x ceiling.

Strategic Pivots: The Copper Imperative & Pragmatic ESG

Glencore’s capital allocation in 2025 decisively signals a structural shift from a traditional diversified miner to a critical supplier of energy transition metals. Out of the $7.6 billion industrial capital expenditure, approximately 55% was directed toward green metals, with copper alone absorbing 36%.

* The Copper Growth Pipeline: Glencore is actively closing the gap with top-tier copper producers, setting a firm target of 1 million tons of annual copper production by 2028, scaling to 1.6 million tons by 2035. Key derisking moves in 2025 included the acquisition of the Quechua project in Peru and advancing the El Pachón and Agua Rica assets in Argentina under the RIGI incentive framework.

* A Pragmatic Approach to Coal: Rejecting the aggressive divestment trend seen across the sector, Glencore is employing a "managed decline" strategy for thermal coal. It closed seven coal mines between 2019 and 2025, with plans to close at least five more by 2035. Simultaneously, the recent integration of Elk Valley Resources (EVR) boosted its metallurgical coal output by 63% to 32.5 mt, positioning the company to serve long-term global steel demand while using fossil fuel cash flows to self-fund its multi-billion-dollar copper expansion without dilutive equity raises.

Sector Positioning & The AI Infrastructure Supercycle

Glencore’s management has officially identified Artificial Intelligence (AI) and data center infrastructure as structural macroeconomic drivers for base metals. As the locus of global demand shifts, the company’s revenue remains heavily anchored in Asia, which generated $121.57 billion (49.1% of total revenue) in 2025.

China—including the broader Greater China supply chain—remains a critical growth engine. The rapid expansion of AI data centers, grid modernization, and digital transformation across Asia requires unprecedented volumes of copper and cobalt. Glencore’s policy of "value over volume," demonstrated by its willingness to stockpile cobalt amid Democratic Republic of Congo (DRC) export restrictions, cements its pricing power and market leadership in these critical tech-enabling supply chains.

HDIN Viewpoint: Earnings Quality and Impairment Scrutiny

While Glencore’s strategic trajectory is compelling, our institutional perspective at HDIN Research urges investors to scrutinize the company’s earnings quality and contingent liabilities.

In 2025, Glencore recorded approximately $2 billion in project impairments, predominantly targeting the Cerrejón coal mine and South African coal operations. While compliant with accounting standards amidst falling thermal coal prices, there is a strategic possibility that management is executing a "Big Bath" accounting maneuver. By writing down legacy carbon assets during a cyclical trough, the company effectively cleanses its balance sheet, mathematically inflating future Return on Equity (ROE) and net profit margins as its high-margin copper assets come online.

Furthermore, global compliance and geopolitical risks remain tangible. Despite the early termination of the US DOJ compliance monitor—a significant governance milestone—the company still faces a $2.7 billion tax dispute in Chile and ongoing regulatory scrutiny in the DRC. How Glencore provisions for these legal contingencies could serve as a lever for future earnings management.

Ultimately, Glencore’s 2025 performance highlights a masterfully executed transition. If the company can successfully navigate localized geopolitical risks and deliver on its South American copper pipeline, it is poised to command a premium valuation in the impending green infrastructure supercycle.

Presentation Download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Glencore 2025: A Global Value Chain in Transition

Here is HDIN Research’s in-depth analysis of Glencore’s 2025 strategic positioning, financial health, and risk architecture.Financial Resilience & The "Marketing" Moat

In 2025, Glencore demonstrated the structural asymmetry of its business model compared to pure-play mining peers like BHP or Rio Tinto. While the Industrial division faced cyclical headwinds—primarily a 23% drop in Newcastle thermal coal benchmark prices—resulting in a 6% year-over-year decline in Adjusted EBITDA to $13.51 billion, the company’s unique architecture provided a critical buffer.

The Marketing division acts as a highly effective hedge against commodity price volatility. Utilizing sophisticated geographical, product, and time arbitrage, the marketing arm delivered $2.92 billion in Adjusted EBIT. When energy margins compressed, metal trading (capitalizing on a 44% intra-year copper price surge and regional supply chain bottlenecks) generated record-level returns. This dual-engine model allows Glencore to earn "fee-like" income during market downturns, maintaining a pristine balance sheet with a net debt-to-Adjusted EBITDA ratio of just 0.83x, well below the company’s 2.0x ceiling.

Strategic Pivots: The Copper Imperative & Pragmatic ESG

Glencore’s capital allocation in 2025 decisively signals a structural shift from a traditional diversified miner to a critical supplier of energy transition metals. Out of the $7.6 billion industrial capital expenditure, approximately 55% was directed toward green metals, with copper alone absorbing 36%.

* The Copper Growth Pipeline: Glencore is actively closing the gap with top-tier copper producers, setting a firm target of 1 million tons of annual copper production by 2028, scaling to 1.6 million tons by 2035. Key derisking moves in 2025 included the acquisition of the Quechua project in Peru and advancing the El Pachón and Agua Rica assets in Argentina under the RIGI incentive framework.

* A Pragmatic Approach to Coal: Rejecting the aggressive divestment trend seen across the sector, Glencore is employing a "managed decline" strategy for thermal coal. It closed seven coal mines between 2019 and 2025, with plans to close at least five more by 2035. Simultaneously, the recent integration of Elk Valley Resources (EVR) boosted its metallurgical coal output by 63% to 32.5 mt, positioning the company to serve long-term global steel demand while using fossil fuel cash flows to self-fund its multi-billion-dollar copper expansion without dilutive equity raises.

Sector Positioning & The AI Infrastructure Supercycle

Glencore’s management has officially identified Artificial Intelligence (AI) and data center infrastructure as structural macroeconomic drivers for base metals. As the locus of global demand shifts, the company’s revenue remains heavily anchored in Asia, which generated $121.57 billion (49.1% of total revenue) in 2025.

China—including the broader Greater China supply chain—remains a critical growth engine. The rapid expansion of AI data centers, grid modernization, and digital transformation across Asia requires unprecedented volumes of copper and cobalt. Glencore’s policy of "value over volume," demonstrated by its willingness to stockpile cobalt amid Democratic Republic of Congo (DRC) export restrictions, cements its pricing power and market leadership in these critical tech-enabling supply chains.

HDIN Viewpoint: Earnings Quality and Impairment Scrutiny

While Glencore’s strategic trajectory is compelling, our institutional perspective at HDIN Research urges investors to scrutinize the company’s earnings quality and contingent liabilities.

In 2025, Glencore recorded approximately $2 billion in project impairments, predominantly targeting the Cerrejón coal mine and South African coal operations. While compliant with accounting standards amidst falling thermal coal prices, there is a strategic possibility that management is executing a "Big Bath" accounting maneuver. By writing down legacy carbon assets during a cyclical trough, the company effectively cleanses its balance sheet, mathematically inflating future Return on Equity (ROE) and net profit margins as its high-margin copper assets come online.

Furthermore, global compliance and geopolitical risks remain tangible. Despite the early termination of the US DOJ compliance monitor—a significant governance milestone—the company still faces a $2.7 billion tax dispute in Chile and ongoing regulatory scrutiny in the DRC. How Glencore provisions for these legal contingencies could serve as a lever for future earnings management.

Ultimately, Glencore’s 2025 performance highlights a masterfully executed transition. If the company can successfully navigate localized geopolitical risks and deliver on its South American copper pipeline, it is poised to command a premium valuation in the impending green infrastructure supercycle.

Presentation Download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com