Decoding Hanwha Ocean’s 2025 Financial Reversal: Strategic Moats in High-Value LNG and Global Defense MRO

Date : 2026-03-16

Reading : 123

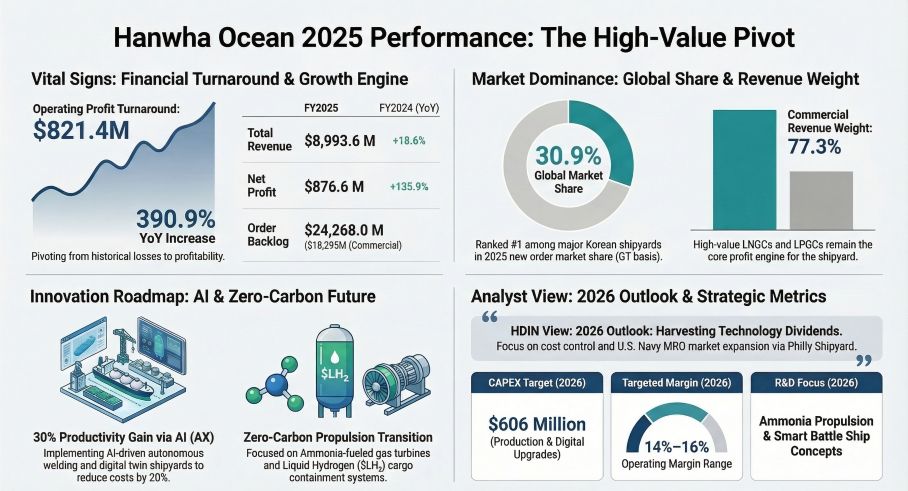

Hanwha Ocean has definitively completed its structural pivot from a legacy shipbuilder to a comprehensive "Global Ocean Solution Provider." According to the latest financial analysis by HDIN Research, the company’s 2025 turnaround—marked by a robust $821 million (1.17 trillion KRW) operating profit—was not merely the result of a cyclical rebound. Rather, it underscores a calculated strategic shift toward high-margin Liquefied Natural Gas Carriers (LNGC), aggressive penetration into the U.S. naval Maintenance, Repair, and Overhaul (MRO) market, and a highly synergized global supply chain.

Figure Hanwha Ocean 2025 Performance: The High-Value Pivot

Sector Positioning: Margin Expansion Through High-Value Assets

Sector Positioning: Margin Expansion Through High-Value Assets

The primary catalyst for Hanwha Ocean’s financial reversal is its strict adherence to a "Selective High-Price Ordering" strategy. In 2025, the commercial vessel division contributed a staggering 98.9% of the company’s total operating profit.

The "so what" behind these figures lies in the asset mix. By phasing out low-margin historical contracts and concentrating on LNGCs—maintaining an average vessel price of $248 million—the company has successfully insulated its margins from broader shipbuilding cyclical headwinds. With a massive $24.26 billion backlog extending beyond 2028, Hanwha Ocean has locked in long-term revenue visibility. Furthermore, the Engineering & Infrastructure (E&I) division emerged as a high-growth pillar, with revenue surging 143.3% following the strategic absorption of Hanwha Group's offshore wind and plant assets, effectively transforming the company into an end-to-end energy developer.

Strategic Moats: Global Defense Synergies and Tech Premium

Hanwha Ocean is actively constructing insurmountable strategic moats across both defense and commercial sectors:

* Defense Market Penetration: The company is leveraging internal Hanwha Group synergies (integrating radar and combat systems from Hanwha Systems) to build a "Smart Navy" portfolio. Crucially, the December 2024 acquisition of a 40% stake in Philly Shipyard establishes a vital U.S. manufacturing footprint, allowing Hanwha Ocean to capture lucrative U.S. Navy MRO contracts and capture early market share in the world’s largest defense market.

* Technological Premium: To maintain pricing power against low-cost regional competitors, Hanwha Ocean is pushing the boundaries of zero-carbon shipping. The deployment of proprietary Sub-cooling Reliquefaction Systems (SRS) significantly reduces the Boil-Off Rate (BOR) in LNGCs, directly translating to energy savings for shipowners. Concurrently, the firm is advancing ammonia-fueled gas turbines and immersion-cooling Energy Storage Systems (ESS), positioning itself ahead of tightening IMO decarbonization mandates.

Capital Allocation Efficiency and Operational Synergy

To support its $24.26 billion backlog, Hanwha Ocean is operating its core Geoje shipyard at 100.5% capacity. To mitigate the risks of labor shortages and capacity bottlenecks, management has demonstrated exceptional capital allocation efficiency by utilizing its Shandong, China facility (running at 99.0% capacity) for cost-effective block and component manufacturing.

Furthermore, to hedge against raw material volatility—specifically steel plate prices averaging $643/ton in 2025—the company has initiated a sweeping AI Transformation (AX). By integrating autonomous welding and digital twin technologies, Hanwha Ocean targets a 30% increase in productivity and a 20% reduction in manufacturing costs, building a formidable buffer against future supply chain shocks.

HDIN Viewpoint: Navigating Hidden Leverage and Estimation Risks

While Hanwha Ocean's operational pivot is highly successful, HDIN Research analysts advise institutional investors to look beyond the top-line recovery and monitor underlying balance sheet vulnerabilities.

Through our internal "Red Teaming" financial analysis, two critical risk vectors emerge:

1. Percentage of Completion (POC) Exposure: The company's turnaround relies heavily on "input method" accounting. With unbilled contract assets soaring to $3.87 billion, profit margins remain hyper-sensitive to material cost overruns. A mere 5% increase in estimated residual costs could wipe out approximately $387 million in pre-tax profits.

2. Disguised Financial Leverage: Hanwha Ocean currently classifies $1.64 billion (2.33 trillion KRW) in perpetual hybrid securities as equity. If reclassified as debt, the company’s true debt-to-equity ratio would spike from the reported 226% to over 362%.

Ultimately, Hanwha Ocean’s transition from liquidating historical baggage to reaping the rewards of a technological premium is complete. However, sustaining this valuation into the 2026-2027 delivery super-cycle will require flawless execution in cost control, FX hedging, and the successful scaling of its U.S. defense operations.

Access the Full Analysis

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Hanwha Ocean 2025 Performance: The High-Value Pivot

Sector Positioning: Margin Expansion Through High-Value AssetsThe primary catalyst for Hanwha Ocean’s financial reversal is its strict adherence to a "Selective High-Price Ordering" strategy. In 2025, the commercial vessel division contributed a staggering 98.9% of the company’s total operating profit.

The "so what" behind these figures lies in the asset mix. By phasing out low-margin historical contracts and concentrating on LNGCs—maintaining an average vessel price of $248 million—the company has successfully insulated its margins from broader shipbuilding cyclical headwinds. With a massive $24.26 billion backlog extending beyond 2028, Hanwha Ocean has locked in long-term revenue visibility. Furthermore, the Engineering & Infrastructure (E&I) division emerged as a high-growth pillar, with revenue surging 143.3% following the strategic absorption of Hanwha Group's offshore wind and plant assets, effectively transforming the company into an end-to-end energy developer.

Strategic Moats: Global Defense Synergies and Tech Premium

Hanwha Ocean is actively constructing insurmountable strategic moats across both defense and commercial sectors:

* Defense Market Penetration: The company is leveraging internal Hanwha Group synergies (integrating radar and combat systems from Hanwha Systems) to build a "Smart Navy" portfolio. Crucially, the December 2024 acquisition of a 40% stake in Philly Shipyard establishes a vital U.S. manufacturing footprint, allowing Hanwha Ocean to capture lucrative U.S. Navy MRO contracts and capture early market share in the world’s largest defense market.

* Technological Premium: To maintain pricing power against low-cost regional competitors, Hanwha Ocean is pushing the boundaries of zero-carbon shipping. The deployment of proprietary Sub-cooling Reliquefaction Systems (SRS) significantly reduces the Boil-Off Rate (BOR) in LNGCs, directly translating to energy savings for shipowners. Concurrently, the firm is advancing ammonia-fueled gas turbines and immersion-cooling Energy Storage Systems (ESS), positioning itself ahead of tightening IMO decarbonization mandates.

Capital Allocation Efficiency and Operational Synergy

To support its $24.26 billion backlog, Hanwha Ocean is operating its core Geoje shipyard at 100.5% capacity. To mitigate the risks of labor shortages and capacity bottlenecks, management has demonstrated exceptional capital allocation efficiency by utilizing its Shandong, China facility (running at 99.0% capacity) for cost-effective block and component manufacturing.

Furthermore, to hedge against raw material volatility—specifically steel plate prices averaging $643/ton in 2025—the company has initiated a sweeping AI Transformation (AX). By integrating autonomous welding and digital twin technologies, Hanwha Ocean targets a 30% increase in productivity and a 20% reduction in manufacturing costs, building a formidable buffer against future supply chain shocks.

HDIN Viewpoint: Navigating Hidden Leverage and Estimation Risks

While Hanwha Ocean's operational pivot is highly successful, HDIN Research analysts advise institutional investors to look beyond the top-line recovery and monitor underlying balance sheet vulnerabilities.

Through our internal "Red Teaming" financial analysis, two critical risk vectors emerge:

1. Percentage of Completion (POC) Exposure: The company's turnaround relies heavily on "input method" accounting. With unbilled contract assets soaring to $3.87 billion, profit margins remain hyper-sensitive to material cost overruns. A mere 5% increase in estimated residual costs could wipe out approximately $387 million in pre-tax profits.

2. Disguised Financial Leverage: Hanwha Ocean currently classifies $1.64 billion (2.33 trillion KRW) in perpetual hybrid securities as equity. If reclassified as debt, the company’s true debt-to-equity ratio would spike from the reported 226% to over 362%.

Ultimately, Hanwha Ocean’s transition from liquidating historical baggage to reaping the rewards of a technological premium is complete. However, sustaining this valuation into the 2026-2027 delivery super-cycle will require flawless execution in cost control, FX hedging, and the successful scaling of its U.S. defense operations.

Access the Full Analysis

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com