Strategic Moats and Profit Benchmarks: A 2025 Financial Evaluation of the Global Flavors & Fragrances Giants

Date : 2026-03-17

Reading : 387

The global Flavors & Fragrances (F&F) industry is undergoing a profound structural transition in 2025, shifting rapidly from mere scale expansion to a fierce competition over technological barriers and ESG premiums. According to HDIN Research’s in-depth analysis of the latest annual reports from industry giants—Givaudan, International Flavors & Fragrances (IFF), Sensient, and Treatt—the market is exhibiting extreme financial polarization. While top-tier players are leveraging entrenched strategic moats to dictate pricing, niche participants are navigating severe cyclical headwinds tied to commodity volatility.

For institutional investors and industry stakeholders, understanding the underlying capital allocation efficiency and shifting sector positioning is no longer optional—it is critical for predicting the next cycle of value creation.

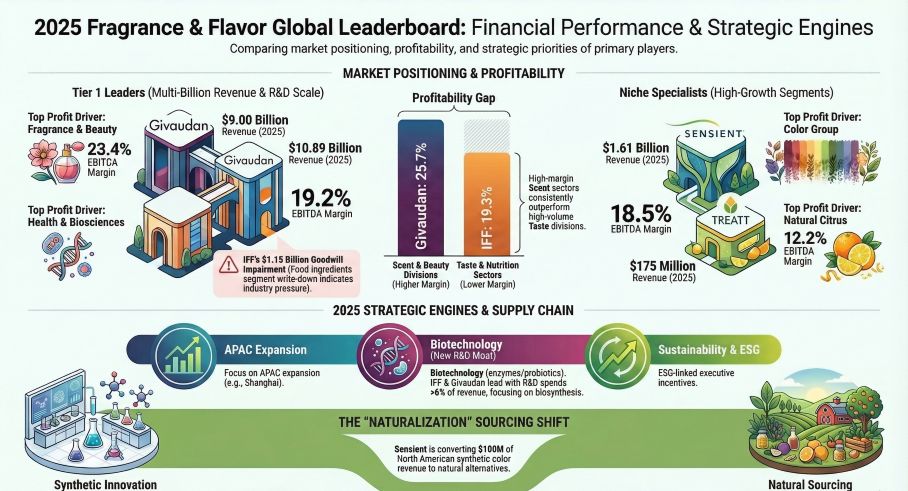

Figure 2025 Fragrance & Flavor Global Leaderboard: Financial Performance & Strategic Engines

Sector Positioning and Financial Health: The Profitability Divide

Sector Positioning and Financial Health: The Profitability Divide

In 2025, the F&F sector demonstrated a definitive "winner-takes-all" dynamic in terms of profitability and operational resilience.

Givaudan has unequivocally cemented its status as the industry’s profit benchmark. By maintaining exceptional pricing power in premium fine fragrances and high-tech taste solutions, Givaudan achieved a robust 23.4% EBITDA margin and an 18.5% operating margin. Furthermore, its superior capital allocation efficiency is evident in its highly synchronized cash flow generation, completely insulating it from the margin compression impacting smaller peers.

Conversely, IFF leads in absolute scale with nearly $10.89 billion in revenue but is currently navigating significant restructuring pains. The company recognized a massive $1.15 billion non-cash goodwill impairment in its Food Ingredients division. This accounting adjustment highlights the severe integration friction and unrealized synergies from past premium acquisitions. However, IFF's operational efficiency remains a formidable moat, evidenced by its industry-leading 58-day Days Sales Outstanding (DSO), reflecting dominant downstream bargaining power.

Meanwhile, Treatt, a mid-cap player heavily reliant on natural extracts, faced severe cyclical headwinds. A prolonged spike in citrus raw material prices and softening premium demand in the US triggered an 11.8% revenue contraction. This underscores the structural vulnerabilities of niche market participants when lacking the diversified portfolios required to absorb macroeconomic shocks.

Strategic Moats: High Switching Costs and Bio-Tech Innovation

The high barriers to entry in the F&F market are maintained through deeply entrenched "core supplier lists" and formula stickiness. Because flavor and fragrance profiles are critical to brand loyalty yet constitute a fraction of total Cost of Goods Sold (COGS), consumer packaged goods (CPG) companies face immense switching costs and sensory risks if they change suppliers.

To future-proof these moats, industry leaders are pivoting heavily toward biotechnology and health-oriented solutions:

* Biosciences as a Cash Cow: IFF’s Health & Biosciences (H&B) division has emerged as its true profit engine, delivering a 26.0% adjusted EBITDA margin. By leveraging proprietary enzyme and microbial technologies, IFF provides advanced sugar-reduction and high-fiber solutions. This enables lucrative cross-selling synergies with its Taste division, effectively elevating ingredients from commodities to high-margin technical solutions.

* Regulatory Arbitrage in Natural Colors: Sensient is strategically utilizing changing regulations as a growth catalyst. With impending US FDA bans on specific synthetic dyes (such as Red 3) and expanding state-level restrictions, Sensient is capturing a $100 million revenue opportunity in North America through natural color conversion. By vertically integrating its supply chain from farm to extraction, Sensient's Color Group generated a highly resilient 20.2% operating margin, proving that regulatory compliance can be weaponized for market share.

ESG Premiums and the New Cost of Compliance

Sustainability is no longer merely a corporate social responsibility initiative; it has materialized into a rigid financial cost and a competitive filter. HDIN Research notes that the tightening web of European regulations—including REACH requirements, CLP reclassifications, and microplastic bans in cosmetics—is forcing comprehensive portfolio reformulations across the board.

Leaders like Givaudan are absorbing these costs through scale and tying executive compensation directly to greenhouse gas emission targets. Treatt has transitioned 85% of its portfolio to natural ingredients, supported by a rigorous 29-country traceability network. However, the capital expenditure required to meet these stringent ESG mandates and secure supply chains against climate-induced agricultural stress will inevitably squeeze out undercapitalized market players.

Additionally, the sector faces heightened legal scrutiny, with both Givaudan and IFF navigating ongoing global antitrust investigations concerning coordinated pricing—a geopolitical and legal headwind that warrants close observation.

HDIN Viewpoint

HDIN Research views the 2025 F&F landscape as a market of diverging destinies. Givaudan remains the safest harbor for capital, displaying unparalleled cash flow quality and organic growth stability. IFF is currently in a defensive capital allocation phase—aggressively divesting non-core assets to deleverage its balance sheet—though its underlying bioscience intellectual property remains highly valuable.

For specialized players, the strategy is clear: survive cyclical commodity headwinds through aggressive differentiation. Sensient’s pivot toward regulatory-driven natural colors is a textbook example of finding growth in a stagnant macro environment. Moving forward, the true winners in the F&F space will be those who can seamlessly translate compliance and biotechnology into unassailable pricing power.

Presentation Download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

For institutional investors and industry stakeholders, understanding the underlying capital allocation efficiency and shifting sector positioning is no longer optional—it is critical for predicting the next cycle of value creation.

Figure 2025 Fragrance & Flavor Global Leaderboard: Financial Performance & Strategic Engines

Sector Positioning and Financial Health: The Profitability DivideIn 2025, the F&F sector demonstrated a definitive "winner-takes-all" dynamic in terms of profitability and operational resilience.

Givaudan has unequivocally cemented its status as the industry’s profit benchmark. By maintaining exceptional pricing power in premium fine fragrances and high-tech taste solutions, Givaudan achieved a robust 23.4% EBITDA margin and an 18.5% operating margin. Furthermore, its superior capital allocation efficiency is evident in its highly synchronized cash flow generation, completely insulating it from the margin compression impacting smaller peers.

Conversely, IFF leads in absolute scale with nearly $10.89 billion in revenue but is currently navigating significant restructuring pains. The company recognized a massive $1.15 billion non-cash goodwill impairment in its Food Ingredients division. This accounting adjustment highlights the severe integration friction and unrealized synergies from past premium acquisitions. However, IFF's operational efficiency remains a formidable moat, evidenced by its industry-leading 58-day Days Sales Outstanding (DSO), reflecting dominant downstream bargaining power.

Meanwhile, Treatt, a mid-cap player heavily reliant on natural extracts, faced severe cyclical headwinds. A prolonged spike in citrus raw material prices and softening premium demand in the US triggered an 11.8% revenue contraction. This underscores the structural vulnerabilities of niche market participants when lacking the diversified portfolios required to absorb macroeconomic shocks.

Strategic Moats: High Switching Costs and Bio-Tech Innovation

The high barriers to entry in the F&F market are maintained through deeply entrenched "core supplier lists" and formula stickiness. Because flavor and fragrance profiles are critical to brand loyalty yet constitute a fraction of total Cost of Goods Sold (COGS), consumer packaged goods (CPG) companies face immense switching costs and sensory risks if they change suppliers.

To future-proof these moats, industry leaders are pivoting heavily toward biotechnology and health-oriented solutions:

* Biosciences as a Cash Cow: IFF’s Health & Biosciences (H&B) division has emerged as its true profit engine, delivering a 26.0% adjusted EBITDA margin. By leveraging proprietary enzyme and microbial technologies, IFF provides advanced sugar-reduction and high-fiber solutions. This enables lucrative cross-selling synergies with its Taste division, effectively elevating ingredients from commodities to high-margin technical solutions.

* Regulatory Arbitrage in Natural Colors: Sensient is strategically utilizing changing regulations as a growth catalyst. With impending US FDA bans on specific synthetic dyes (such as Red 3) and expanding state-level restrictions, Sensient is capturing a $100 million revenue opportunity in North America through natural color conversion. By vertically integrating its supply chain from farm to extraction, Sensient's Color Group generated a highly resilient 20.2% operating margin, proving that regulatory compliance can be weaponized for market share.

ESG Premiums and the New Cost of Compliance

Sustainability is no longer merely a corporate social responsibility initiative; it has materialized into a rigid financial cost and a competitive filter. HDIN Research notes that the tightening web of European regulations—including REACH requirements, CLP reclassifications, and microplastic bans in cosmetics—is forcing comprehensive portfolio reformulations across the board.

Leaders like Givaudan are absorbing these costs through scale and tying executive compensation directly to greenhouse gas emission targets. Treatt has transitioned 85% of its portfolio to natural ingredients, supported by a rigorous 29-country traceability network. However, the capital expenditure required to meet these stringent ESG mandates and secure supply chains against climate-induced agricultural stress will inevitably squeeze out undercapitalized market players.

Additionally, the sector faces heightened legal scrutiny, with both Givaudan and IFF navigating ongoing global antitrust investigations concerning coordinated pricing—a geopolitical and legal headwind that warrants close observation.

HDIN Viewpoint

HDIN Research views the 2025 F&F landscape as a market of diverging destinies. Givaudan remains the safest harbor for capital, displaying unparalleled cash flow quality and organic growth stability. IFF is currently in a defensive capital allocation phase—aggressively divesting non-core assets to deleverage its balance sheet—though its underlying bioscience intellectual property remains highly valuable.

For specialized players, the strategy is clear: survive cyclical commodity headwinds through aggressive differentiation. Sensient’s pivot toward regulatory-driven natural colors is a textbook example of finding growth in a stagnant macro environment. Moving forward, the true winners in the F&F space will be those who can seamlessly translate compliance and biotechnology into unassailable pricing power.

Presentation Download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com