Samsung vs. LG Display 2025: Strategic Moats and Capital Allocation in the OLED Era

Date : 2026-03-17

Reading : 432

The global display panel industry in 2025 has decisively pivoted from capacity-driven scale competition to a battle for technological premium and strategic moats. According to HDIN Research’s latest benchmark analysis, the era of commoditized LCD dominance has officially ended for South Korean tech giants. Instead, LG Display (LGD) and Samsung Electronics (specifically Samsung Display, SDC) are executing starkly divergent playbooks to navigate cyclical headwinds and capture high-margin growth.

While LGD is undergoing a radical balance sheet restructuring to carve out a turnaround, Samsung is leveraging its formidable vertical integration to solidify its position as an insulated cash cow. Here is a deep dive into the strategic implications behind the 2025 data.

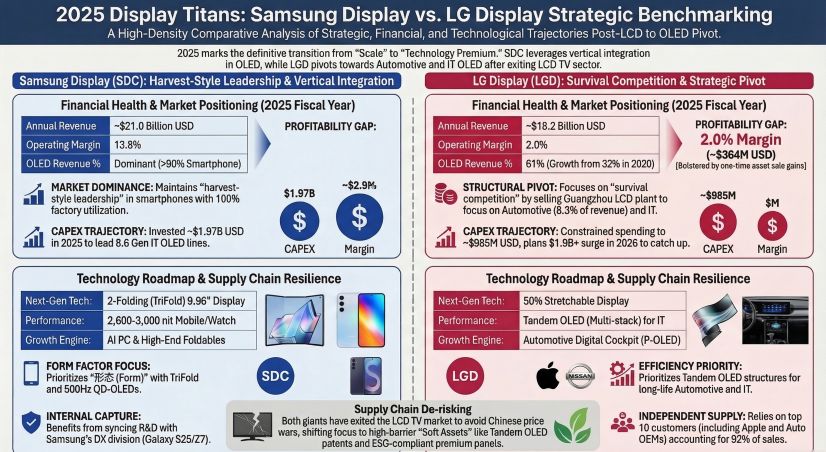

Figure 2025 Display Titans: Samsung Display vs LG Display Strategic Benchmarking

Capital Allocation Efficiency and Structural De-risking

Capital Allocation Efficiency and Structural De-risking

In 2025, both companies demonstrated a shared strategic consensus: the complete liquidation of legacy LCD assets. However, their capital allocation efficiency reveals contrasting financial realities.

LGD successfully executed a critical asset de-risking strategy by divesting its Guangzhou LCD plant to CSOT. This move generated approximately $534 million in disposal gains, serving a dual purpose: it significantly deleveraged LGD’s balance sheet (reducing financial liabilities by $1.32 billion) and structurally insulated the company from the severe price volatility of standard LCD TVs. Consequently, LGD has aggressively repositioned its revenue mix, elevating its OLED share to 61%.

Conversely, Samsung operates from a position of immense capital surplus. SDC generated an industry-leading 13.8% operating profit margin in 2025, contributing roughly $2.89 billion to its parent company. This robust cash generation fueled an aggressive $1.96 billion capital expenditure (CAPEX) heavily weighted toward Gen 8.6 IT OLED production lines. The strategic implication is clear: Samsung is leveraging its early-mover advantage and superior asset return (ROA of ~5.9% vs. LGD’s ~1.1%) to monopolize the next-generation AI PC and premium tablet market, while LGD is forced to delay its major Gen 8.6 CAPEX push until 2026 due to financing constraints.

Strategic Moats: Vertical Integration vs. Independent Supply

The most defining differentiator between the two giants lies in their ecosystem architecture.

Samsung’s greatest strategic moat is its "Internal Capture" capability. Operating a closed-loop "Panel-Device-Chip" ecosystem, SDC aligns its advanced R&D directly with the Samsung DX division's product roadmap. In 2025, this synergy was evident in the seamless rollout of the TriFold (9.96" 2-Folding) display and the Galaxy S25 series. This vertical integration provides a powerful profit buffer against cyclical headwinds; even as global smartphone OLED average selling prices (ASPs) dipped by 6%, SDC maintained a 100% factory utilization rate by digesting its own premium supply.

LGD, as an independent supplier, relies on a vastly different strategy. With its top 10 clients accounting for 92% of sales, LGD faces higher concentration risks but counters this by deeply embedding itself into the supply chains of global Tier-1 automotive and IT brands. By pioneering Tandem OLED technology for medium-sized IT devices and premium automotive digital cockpits, LGD is building an exclusive technological moat that caters to clients who directly compete with Samsung’s end-products.

Sector Positioning in the AI and Automotive Era

As consumer electronics face macroeconomic ceilings, both firms are aggressively repositioning into high-growth, high-margin sectors.

Samsung’s focus remains on "form-factor innovation" and peak performance. By commercializing ultra-high refresh rate QD-OLED monitors (500Hz) and achieving peak brightness levels of 3,000 nits in wearables, Samsung is dictating the pricing power in the ultra-premium segment.

Meanwhile, LGD is capitalizing on the electrification of vehicles. Its strategic pivot toward P-OLED and ATO (Advanced Thin OLED) combinations has secured a dominant foothold in the automotive sector. Furthermore, LGD’s breakthrough in 50% stretchable displays signals a long-term play in unlocking entirely new form factors for IoT and mobility integration. Both companies are also rapidly scaling their ESG compliance capabilities, recognizing that certified low-carbon manufacturing is now a mandatory barrier to entry for lucrative North American and European contracts.

HDIN Viewpoint: The Investor's Perspective

HDIN Research categorizes Samsung Electronics as a "robust value growth" play. Its diversified profit engines—where the semiconductor division's explosive AI-driven growth effectively hedges against display panel cyclicality—grant SDC an unmatched tolerance for risk and a massive runway for sustained Gen 8.6 investments.

In contrast, LG Display represents a "high-elasticity turnaround" case. The 2025 financials indicate that LGD has successfully stopped the bleeding by severing its ties with the commoditized LCD market. If LGD can maintain its lead in automotive Tandem OLEDs and successfully execute its 2026 infrastructure investments without over-leveraging, the company is well-positioned for structural profitability. However, its future valuation will heavily depend on navigating high external client concentration and managing depreciation costs over the next two years.

Presentation Download & Media Access

- Click the PDF download link under “Related Topics” to access the presentation of this report.

- Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

While LGD is undergoing a radical balance sheet restructuring to carve out a turnaround, Samsung is leveraging its formidable vertical integration to solidify its position as an insulated cash cow. Here is a deep dive into the strategic implications behind the 2025 data.

Figure 2025 Display Titans: Samsung Display vs LG Display Strategic Benchmarking

Capital Allocation Efficiency and Structural De-riskingIn 2025, both companies demonstrated a shared strategic consensus: the complete liquidation of legacy LCD assets. However, their capital allocation efficiency reveals contrasting financial realities.

LGD successfully executed a critical asset de-risking strategy by divesting its Guangzhou LCD plant to CSOT. This move generated approximately $534 million in disposal gains, serving a dual purpose: it significantly deleveraged LGD’s balance sheet (reducing financial liabilities by $1.32 billion) and structurally insulated the company from the severe price volatility of standard LCD TVs. Consequently, LGD has aggressively repositioned its revenue mix, elevating its OLED share to 61%.

Conversely, Samsung operates from a position of immense capital surplus. SDC generated an industry-leading 13.8% operating profit margin in 2025, contributing roughly $2.89 billion to its parent company. This robust cash generation fueled an aggressive $1.96 billion capital expenditure (CAPEX) heavily weighted toward Gen 8.6 IT OLED production lines. The strategic implication is clear: Samsung is leveraging its early-mover advantage and superior asset return (ROA of ~5.9% vs. LGD’s ~1.1%) to monopolize the next-generation AI PC and premium tablet market, while LGD is forced to delay its major Gen 8.6 CAPEX push until 2026 due to financing constraints.

Strategic Moats: Vertical Integration vs. Independent Supply

The most defining differentiator between the two giants lies in their ecosystem architecture.

Samsung’s greatest strategic moat is its "Internal Capture" capability. Operating a closed-loop "Panel-Device-Chip" ecosystem, SDC aligns its advanced R&D directly with the Samsung DX division's product roadmap. In 2025, this synergy was evident in the seamless rollout of the TriFold (9.96" 2-Folding) display and the Galaxy S25 series. This vertical integration provides a powerful profit buffer against cyclical headwinds; even as global smartphone OLED average selling prices (ASPs) dipped by 6%, SDC maintained a 100% factory utilization rate by digesting its own premium supply.

LGD, as an independent supplier, relies on a vastly different strategy. With its top 10 clients accounting for 92% of sales, LGD faces higher concentration risks but counters this by deeply embedding itself into the supply chains of global Tier-1 automotive and IT brands. By pioneering Tandem OLED technology for medium-sized IT devices and premium automotive digital cockpits, LGD is building an exclusive technological moat that caters to clients who directly compete with Samsung’s end-products.

Sector Positioning in the AI and Automotive Era

As consumer electronics face macroeconomic ceilings, both firms are aggressively repositioning into high-growth, high-margin sectors.

Samsung’s focus remains on "form-factor innovation" and peak performance. By commercializing ultra-high refresh rate QD-OLED monitors (500Hz) and achieving peak brightness levels of 3,000 nits in wearables, Samsung is dictating the pricing power in the ultra-premium segment.

Meanwhile, LGD is capitalizing on the electrification of vehicles. Its strategic pivot toward P-OLED and ATO (Advanced Thin OLED) combinations has secured a dominant foothold in the automotive sector. Furthermore, LGD’s breakthrough in 50% stretchable displays signals a long-term play in unlocking entirely new form factors for IoT and mobility integration. Both companies are also rapidly scaling their ESG compliance capabilities, recognizing that certified low-carbon manufacturing is now a mandatory barrier to entry for lucrative North American and European contracts.

HDIN Viewpoint: The Investor's Perspective

HDIN Research categorizes Samsung Electronics as a "robust value growth" play. Its diversified profit engines—where the semiconductor division's explosive AI-driven growth effectively hedges against display panel cyclicality—grant SDC an unmatched tolerance for risk and a massive runway for sustained Gen 8.6 investments.

In contrast, LG Display represents a "high-elasticity turnaround" case. The 2025 financials indicate that LGD has successfully stopped the bleeding by severing its ties with the commoditized LCD market. If LGD can maintain its lead in automotive Tandem OLEDs and successfully execute its 2026 infrastructure investments without over-leveraging, the company is well-positioned for structural profitability. However, its future valuation will heavily depend on navigating high external client concentration and managing depreciation costs over the next two years.

Presentation Download & Media Access

- Click the PDF download link under “Related Topics” to access the presentation of this report.

- Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com