Porsche vs Ferrari 2025: Scarcity Premium or Valuation Trap

Date : 2026-03-17

Reading : 1874

The 2025 fiscal year marks a definitive bifurcation in the ultra-luxury automotive sector. While Porsche AG and Ferrari N.V. share overlapping high-net-worth consumer demographics, their latest financial disclosures reveal fundamentally diverging strategic trajectories. HDIN Research’s latest comparative analysis indicates that while Ferrari has successfully solidified its "hard luxury" valuation through extreme scarcity management, Porsche has stumbled into an industrial valuation trap, battered by cyclical headwinds, aggressive R&D impairments, and stalled Software-Defined Vehicle (SDV) architectures.

Figure Luxury Performance Benchmarking 2025: Industrial Scale vs Exclusive Scarcity

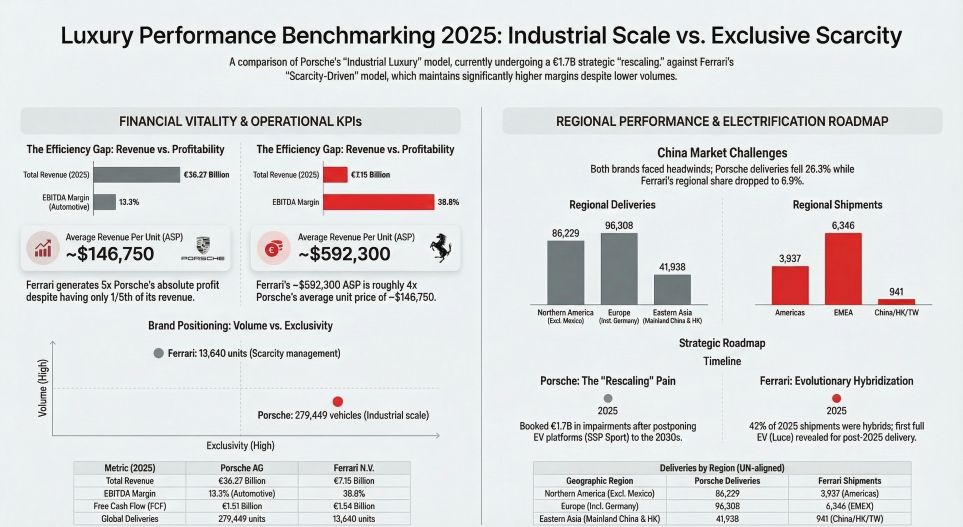

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

A granular review of 2025 earnings exposes a stark contrast in capital allocation efficiency and earnings quality between the two automakers.

Ferrari’s financial architecture remains exceptionally resilient. Despite delivering only 13,640 units (a slight 0.8% volume dip), the brand achieved a 7.0% net revenue growth to approximately $8.08 billion. By leveraging its highly lucrative customization programs (Personalization) and an agile, "technology-neutral" R&D approach, Ferrari maintained a formidable 29.5% EBIT margin. Its absolute operating profit ($2.38 billion) equated to roughly five times that of Porsche, despite operating on one-fifth of the revenue scale.

Conversely, Porsche is enduring severe transitional pain. The company’s Return on Sales (RoS) plummeted to a perilous 1.1%, generating a mere $467 million in operating profit on $41.01 billion in revenue. The catalyst for this margin collapse was a massive $1.92 billion (€1.7 billion) asset impairment and provision. HDIN Research identifies this as a classic "kitchen-sinking" accounting maneuver: Porsche was forced to drastically slash its R&D capitalization rate from 62.6% in 2024 to 42.0% in 2025 following profound delays and strategic pivots regarding its premium electric platform (SSP Sport). This indicates that previous earnings may have been inflated by aggressive capitalization strategies, leaving the current balance sheet highly vulnerable.

Strategic Pivots & Sector Positioning

The underlying operational models of both companies dictate their market defenses.

Porsche’s "Nokia Moment" and Channel Risks:

Porsche is grappling with significant technological and channel-stuffing risks. In 2025, its deliveries in the critical Chinese market plunged by 26.3%. However, global inventory levels remained stubbornly high at approximately $6.79 billion. This alarming divergence between shrinking retail deliveries and stagnant wholesale inventory suggests heavy channel stuffing, which will inevitably lead to margin-crushing discounts or dealer buybacks. Furthermore, the company is facing an impending "Nokia Moment" in its sector positioning. Falling behind local Chinese EV manufacturers in high-level autonomous driving and digital cockpit innovations, Porsche has been forced to delay key pure-electric (BEV) launches and retreat to a transitional hybrid/ICE strategy.

Ferrari’s Impenetrable Scarcity Moat:

Ferrari operates on a completely different paradigm: order-driven production. With 100% of its new vehicles featuring bespoke personalization and a waiting list that vastly outstrips supply, Ferrari enjoys near-absolute pricing power. Its strategic moats are fortified not just by its motorsport DNA, but by strict quota controls that artificially suppress volume to maximize unit profitability.

Cyclical Headwinds & Regulatory Moats

Both automakers operate under the shadow of intensifying global regulatory frameworks and supply chain geopolitics, yet their exposure varies significantly.

The transition to Euro 7 emissions standards and unpredictable US tariff structures presents an asymmetric threat. Porsche has already earmarked hundreds of millions of euros in provisions for potential carbon compliance fines, as its scale makes rapid fleet-wide decarbonization exceptionally costly. Furthermore, shifts in US import tariffs eroded Porsche’s operating profit by an estimated $791 million in 2025.

While Ferrari is not immune to ESG pressures—recently tying 20% of its executive long-term incentives to ESG targets—its low-volume output and strategic investments in e-Fuels buffer the immediate impact of global ICE bans. Both companies share a structural vulnerability: deep reliance on the Greater China supply chain for critical battery raw materials and semiconductor components, making geopolitical stability a baseline requirement for future capital expenditure (CapEx) execution.

HDIN Viewpoint: The Alpha and Beta of Luxury Auto

From an institutional valuation perspective, the capital markets have definitively split the narratives of these two brands. HDIN Research concludes that Ferrari has successfully untethered itself from the traditional automotive sector, earning an *Alpha* asset profile. Its valuation is benchmarked against elite luxury conglomerates like Hermes and LVMH, justified by its extreme capital efficiency, asset-light agility, and brand-driven pricing power.

Porsche, conversely, is being re-rated as a *Beta* industrial stock. Trapped by the immense capital burdens of its EV transition, tied heavily to the Volkswagen Group's software struggles (CARIAD), and highly sensitive to macroeconomic consumption cycles, Porsche’s 1.1% RoS leaves no margin for error. Until Porsche can successfully execute its SDV pipeline without massive consecutive write-downs and clear its congested dealer networks in China, its valuation will remain constrained by traditional automotive industry ceilings.

---

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Luxury Performance Benchmarking 2025: Industrial Scale vs Exclusive Scarcity

Financial Health & Capital Allocation EfficiencyA granular review of 2025 earnings exposes a stark contrast in capital allocation efficiency and earnings quality between the two automakers.

Ferrari’s financial architecture remains exceptionally resilient. Despite delivering only 13,640 units (a slight 0.8% volume dip), the brand achieved a 7.0% net revenue growth to approximately $8.08 billion. By leveraging its highly lucrative customization programs (Personalization) and an agile, "technology-neutral" R&D approach, Ferrari maintained a formidable 29.5% EBIT margin. Its absolute operating profit ($2.38 billion) equated to roughly five times that of Porsche, despite operating on one-fifth of the revenue scale.

Conversely, Porsche is enduring severe transitional pain. The company’s Return on Sales (RoS) plummeted to a perilous 1.1%, generating a mere $467 million in operating profit on $41.01 billion in revenue. The catalyst for this margin collapse was a massive $1.92 billion (€1.7 billion) asset impairment and provision. HDIN Research identifies this as a classic "kitchen-sinking" accounting maneuver: Porsche was forced to drastically slash its R&D capitalization rate from 62.6% in 2024 to 42.0% in 2025 following profound delays and strategic pivots regarding its premium electric platform (SSP Sport). This indicates that previous earnings may have been inflated by aggressive capitalization strategies, leaving the current balance sheet highly vulnerable.

Strategic Pivots & Sector Positioning

The underlying operational models of both companies dictate their market defenses.

Porsche’s "Nokia Moment" and Channel Risks:

Porsche is grappling with significant technological and channel-stuffing risks. In 2025, its deliveries in the critical Chinese market plunged by 26.3%. However, global inventory levels remained stubbornly high at approximately $6.79 billion. This alarming divergence between shrinking retail deliveries and stagnant wholesale inventory suggests heavy channel stuffing, which will inevitably lead to margin-crushing discounts or dealer buybacks. Furthermore, the company is facing an impending "Nokia Moment" in its sector positioning. Falling behind local Chinese EV manufacturers in high-level autonomous driving and digital cockpit innovations, Porsche has been forced to delay key pure-electric (BEV) launches and retreat to a transitional hybrid/ICE strategy.

Ferrari’s Impenetrable Scarcity Moat:

Ferrari operates on a completely different paradigm: order-driven production. With 100% of its new vehicles featuring bespoke personalization and a waiting list that vastly outstrips supply, Ferrari enjoys near-absolute pricing power. Its strategic moats are fortified not just by its motorsport DNA, but by strict quota controls that artificially suppress volume to maximize unit profitability.

Cyclical Headwinds & Regulatory Moats

Both automakers operate under the shadow of intensifying global regulatory frameworks and supply chain geopolitics, yet their exposure varies significantly.

The transition to Euro 7 emissions standards and unpredictable US tariff structures presents an asymmetric threat. Porsche has already earmarked hundreds of millions of euros in provisions for potential carbon compliance fines, as its scale makes rapid fleet-wide decarbonization exceptionally costly. Furthermore, shifts in US import tariffs eroded Porsche’s operating profit by an estimated $791 million in 2025.

While Ferrari is not immune to ESG pressures—recently tying 20% of its executive long-term incentives to ESG targets—its low-volume output and strategic investments in e-Fuels buffer the immediate impact of global ICE bans. Both companies share a structural vulnerability: deep reliance on the Greater China supply chain for critical battery raw materials and semiconductor components, making geopolitical stability a baseline requirement for future capital expenditure (CapEx) execution.

HDIN Viewpoint: The Alpha and Beta of Luxury Auto

From an institutional valuation perspective, the capital markets have definitively split the narratives of these two brands. HDIN Research concludes that Ferrari has successfully untethered itself from the traditional automotive sector, earning an *Alpha* asset profile. Its valuation is benchmarked against elite luxury conglomerates like Hermes and LVMH, justified by its extreme capital efficiency, asset-light agility, and brand-driven pricing power.

Porsche, conversely, is being re-rated as a *Beta* industrial stock. Trapped by the immense capital burdens of its EV transition, tied heavily to the Volkswagen Group's software struggles (CARIAD), and highly sensitive to macroeconomic consumption cycles, Porsche’s 1.1% RoS leaves no margin for error. Until Porsche can successfully execute its SDV pipeline without massive consecutive write-downs and clear its congested dealer networks in China, its valuation will remain constrained by traditional automotive industry ceilings.

---

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com