2025 Rehabilitation Robotics Market: Strategic Moats, Policy Tailwinds, and Financial Bifurcation

Date : 2026-03-17

Reading : 108

The 2025 fiscal year marks a watershed moment for the global wearable exoskeleton and rehabilitation robotics market. An in-depth financial penetration analysis conducted by HDIN Research reveals a sector experiencing aggressive bifurcation. While regulatory shifts have unlocked unprecedented commercialization pathways, capital allocation efficiency and fundamental financial health remain starkly polarized among the industry's "Big Three": Ekso Bionics (EKSO), Myomo (MYO), and P&S Robotics.

Rather than a uniform rising tide, the current market landscape is defined by non-overlapping operational strategies and vastly different risk-reward profiles.

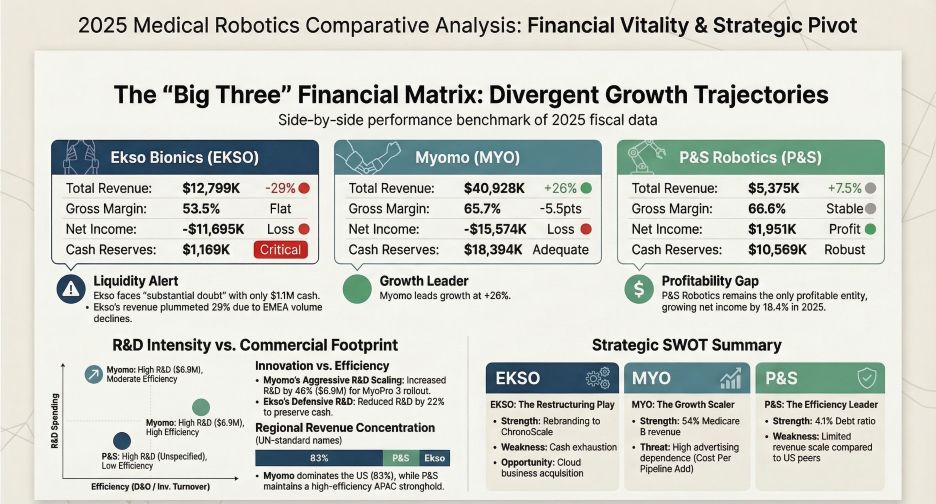

Figure 2025 Medical Robotics Comparative Analysis: Financial Vitality & Strategic Pivot

Industry Outlook: Policy Tailwinds vs. Cyclical Headwinds

Industry Outlook: Policy Tailwinds vs. Cyclical Headwinds

The most significant macroeconomic catalyst driving the sector is the paradigm shift in the United States CMS (Centers for Medicare & Medicaid Services) reimbursement structure. The transition from a leasing model to a "Lump Sum" purchase categorization (yielding $35,000 to $91,000 per unit) has fundamentally altered the B2C trajectory. This policy dividend has effectively transformed personal rehabilitation devices from niche, out-of-pocket luxuries into accessible, evidence-based medical necessities.

Coupled with the structural labor shortages of physical therapists and a rapidly aging global population facing stroke and spinal cord injuries (SCI), the baseline demand for automated rehabilitation is increasingly rigid.

However, cyclical headwinds threaten to compress margins for unprepared players. The painful transition to CE MDR certification in Europe has caused delivery disruptions, while geopolitical supply chain friction—particularly concerning semiconductors and battery components—continues to challenge cross-border operational stability.

Financial Health & Capital Allocation Efficiency

Beneath the topline revenue figures, the capital allocation efficiency of these three entities reveals three entirely different business lifecycles:

* Myomo (Aggressive Growth): Capitalizing heavily on the CMS policy dividend, Myomo’s direct billing model has proven highly efficient. Revenue surged 26% year-over-year to $40.92 million, driven by higher Average Selling Prices (ASP) and explosive growth in the U.S. Orthotics and Prosthetics (O&P) channel. Its Days Sales Outstanding (DSO) of merely 37 days highlights exceptional cash conversion in the personal health market. However, this growth is heavily subsidized by ballooning SG&A expenditures ($20.38 million), resulting in a strategic net loss of $15.57 million as the company aggressively burns cash to capture market share.

* P&S Robotics (Steady Value): As a clinical B2B pure-play, P&S Robotics stands out as the only consistently profitable entity among the trio. Generating roughly $5.37 million in revenue with a highly conservative debt-to-asset ratio of 4.3%, the company boasts a pristine balance sheet. Despite cyclical headwinds in its domestic South Korean market due to medical strikes, its self-sustaining cash flow and 80.5% export revenue ratio underscore a highly resilient business model.

* Ekso Bionics (Distressed Asset): Ekso is facing severe financial distress. Revenue plummeted 29% to $12.79 million, and core enterprise markets are shrinking. With cash reserves dwindling to a perilous $1.16 million by the end of 2025, the company has officially issued a "Going Concern" warning. Its survival now hinges on emergency Series B financing and a potential shell-company restructuring (ChronoScale) to merge with a cloud computing entity, signaling a desperate pivot to avoid insolvency.

Strategic Moats & Sector Positioning

From a technological and geographical perspective, the competitive landscape is driven by highly specialized strategic moats:

* R&D Intensity & Innovation: P&S Robotics leads in deep-tech innovation with an astonishing R&D intensity of approximately 46%. Its proprietary 3-joint (hip/knee/ankle) synchronous kinematics and advanced AI sensor fusion platforms (WalkAgent and WalkCAM) provide an unassailable moat in the premium B2B hospital segment. Conversely, Ekso has defensively slashed its R&D budget by 22% to preserve capital, essentially stalling its innovation pipeline.

* APAC Sector Positioning: The Asia-Pacific (APAC) market highlights a divergence in geopolitical risk management. P&S Robotics dominates the APAC hospital sector with a robust distribution network extending through mainland China and Taiwan, China. Meanwhile, Myomo suffered a total asset impairment following the bankruptcy and liquidation of its Chinese joint venture (JV Ryzur), underscoring severe cross-border compliance and execution risks. Ekso's APAC footprint also remains stagnant at just 11.8% of its global revenue due to certification delays.

* Accounting Red Flags: HDIN Research advises scrutiny regarding earnings quality. Myomo's capitalization of $1.59 million in software development costs slightly masks its true operational cash burn. Furthermore, Ekso's elevated DSO of 208 days—despite crashing revenues—raises critical audit red flags regarding potential channel stuffing, while its reliance on $523,000 in Employee Retention Credit (ERC) tax subsidies artificially softens its operating losses.

HDIN Viewpoint

HDIN Research views the 2025 rehabilitation robotics landscape not as a homogenous tech sector, but as a fragmented arena where policy maneuvering outweighs legacy brand equity.

Myomo has successfully crossed the commercialization threshold; if it can optimize its customer acquisition costs, its CMS-backed moat offers significant upside. P&S Robotics remains the ultimate safe harbor—a rare, profitable innovator whose clean capitalization table makes it a prime candidate for future M&A expansion. Ekso Bionics, however, is a cautionary tale of misaligned capital allocation, requiring investors to navigate extreme liquidity risks and look past accounting maneuvers. Ultimately, sustainable leadership in this space will belong to entities that can bridge clinical AI validation with frictionless reimbursement ecosystems.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Rather than a uniform rising tide, the current market landscape is defined by non-overlapping operational strategies and vastly different risk-reward profiles.

Figure 2025 Medical Robotics Comparative Analysis: Financial Vitality & Strategic Pivot

Industry Outlook: Policy Tailwinds vs. Cyclical HeadwindsThe most significant macroeconomic catalyst driving the sector is the paradigm shift in the United States CMS (Centers for Medicare & Medicaid Services) reimbursement structure. The transition from a leasing model to a "Lump Sum" purchase categorization (yielding $35,000 to $91,000 per unit) has fundamentally altered the B2C trajectory. This policy dividend has effectively transformed personal rehabilitation devices from niche, out-of-pocket luxuries into accessible, evidence-based medical necessities.

Coupled with the structural labor shortages of physical therapists and a rapidly aging global population facing stroke and spinal cord injuries (SCI), the baseline demand for automated rehabilitation is increasingly rigid.

However, cyclical headwinds threaten to compress margins for unprepared players. The painful transition to CE MDR certification in Europe has caused delivery disruptions, while geopolitical supply chain friction—particularly concerning semiconductors and battery components—continues to challenge cross-border operational stability.

Financial Health & Capital Allocation Efficiency

Beneath the topline revenue figures, the capital allocation efficiency of these three entities reveals three entirely different business lifecycles:

* Myomo (Aggressive Growth): Capitalizing heavily on the CMS policy dividend, Myomo’s direct billing model has proven highly efficient. Revenue surged 26% year-over-year to $40.92 million, driven by higher Average Selling Prices (ASP) and explosive growth in the U.S. Orthotics and Prosthetics (O&P) channel. Its Days Sales Outstanding (DSO) of merely 37 days highlights exceptional cash conversion in the personal health market. However, this growth is heavily subsidized by ballooning SG&A expenditures ($20.38 million), resulting in a strategic net loss of $15.57 million as the company aggressively burns cash to capture market share.

* P&S Robotics (Steady Value): As a clinical B2B pure-play, P&S Robotics stands out as the only consistently profitable entity among the trio. Generating roughly $5.37 million in revenue with a highly conservative debt-to-asset ratio of 4.3%, the company boasts a pristine balance sheet. Despite cyclical headwinds in its domestic South Korean market due to medical strikes, its self-sustaining cash flow and 80.5% export revenue ratio underscore a highly resilient business model.

* Ekso Bionics (Distressed Asset): Ekso is facing severe financial distress. Revenue plummeted 29% to $12.79 million, and core enterprise markets are shrinking. With cash reserves dwindling to a perilous $1.16 million by the end of 2025, the company has officially issued a "Going Concern" warning. Its survival now hinges on emergency Series B financing and a potential shell-company restructuring (ChronoScale) to merge with a cloud computing entity, signaling a desperate pivot to avoid insolvency.

Strategic Moats & Sector Positioning

From a technological and geographical perspective, the competitive landscape is driven by highly specialized strategic moats:

* R&D Intensity & Innovation: P&S Robotics leads in deep-tech innovation with an astonishing R&D intensity of approximately 46%. Its proprietary 3-joint (hip/knee/ankle) synchronous kinematics and advanced AI sensor fusion platforms (WalkAgent and WalkCAM) provide an unassailable moat in the premium B2B hospital segment. Conversely, Ekso has defensively slashed its R&D budget by 22% to preserve capital, essentially stalling its innovation pipeline.

* APAC Sector Positioning: The Asia-Pacific (APAC) market highlights a divergence in geopolitical risk management. P&S Robotics dominates the APAC hospital sector with a robust distribution network extending through mainland China and Taiwan, China. Meanwhile, Myomo suffered a total asset impairment following the bankruptcy and liquidation of its Chinese joint venture (JV Ryzur), underscoring severe cross-border compliance and execution risks. Ekso's APAC footprint also remains stagnant at just 11.8% of its global revenue due to certification delays.

* Accounting Red Flags: HDIN Research advises scrutiny regarding earnings quality. Myomo's capitalization of $1.59 million in software development costs slightly masks its true operational cash burn. Furthermore, Ekso's elevated DSO of 208 days—despite crashing revenues—raises critical audit red flags regarding potential channel stuffing, while its reliance on $523,000 in Employee Retention Credit (ERC) tax subsidies artificially softens its operating losses.

HDIN Viewpoint

HDIN Research views the 2025 rehabilitation robotics landscape not as a homogenous tech sector, but as a fragmented arena where policy maneuvering outweighs legacy brand equity.

Myomo has successfully crossed the commercialization threshold; if it can optimize its customer acquisition costs, its CMS-backed moat offers significant upside. P&S Robotics remains the ultimate safe harbor—a rare, profitable innovator whose clean capitalization table makes it a prime candidate for future M&A expansion. Ekso Bionics, however, is a cautionary tale of misaligned capital allocation, requiring investors to navigate extreme liquidity risks and look past accounting maneuvers. Ultimately, sustainable leadership in this space will belong to entities that can bridge clinical AI validation with frictionless reimbursement ecosystems.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com