2025 Global Titanium Dioxide Giants: Strategic Moats and Survival Tactics in a Cyclical Trough

Date : 2026-03-17

Reading : 134

The global Titanium Dioxide ($TiO_2$) industry is navigating a severe cyclical trough in 2025, battered by macroeconomic uncertainties, high interest rates, and stagnant real estate demand. However, a deeper analysis of the top three global giants—Chemours, Tronox, and KRONOS—reveals a profound strategic divergence. Rather than simply waiting for a macroeconomic rebound, these market leaders are actively restructuring their operational DNA.

Based on HDIN Research’s proprietary analysis of 2025 financial disclosures, the industry paradigm has fundamentally shifted from "scale expansion" to "cost resilience" and "structural hedging."

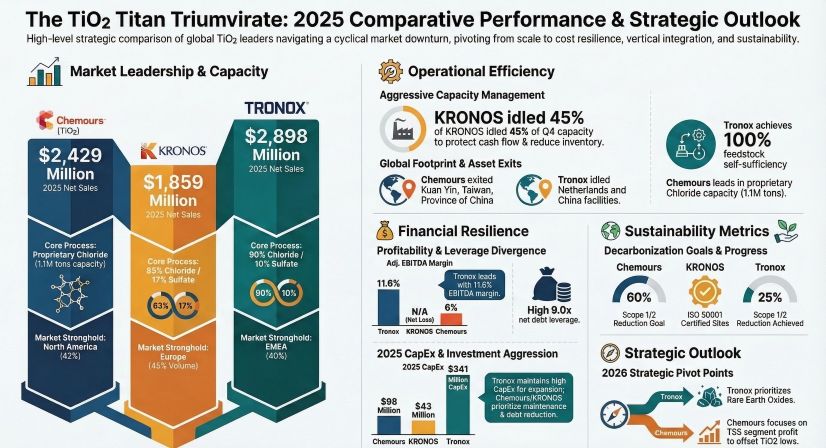

Figure The TiO2 Titan Triumvirate: 2025 Comparative Performance & Strategic Qutlook

Cyclical Headwinds and Aggressive Capacity Rationalization

Cyclical Headwinds and Aggressive Capacity Rationalization

In 2025, sustained high interest rates have frozen housing mobility, directly compressing downstream demand in architectural coatings and plastics. The strategic implication is clear: maintaining high utilization rates in a depressed market is financial suicide. Consequently, the industry is undergoing aggressive capacity out-clearing.

Instead of absorbing inventory holding costs, producers are prioritizing liquidity. KRONOS executed a drastic operational pivot, slashing its Q4 capacity utilization rate to a mere 55%. This deliberate sacrifice of fixed-cost absorption was necessary to aggressively drive down its Days Sales of Inventory (DSI) to 57 days.

Furthermore, the sector is witnessing the permanent elimination of high-cost assets. Chemours completed the decommissioning of its Kuan Yin facility (Taiwan, China), liquidating the land for approximately $360 million to pare down debt. Similarly, Tronox permanently shuttered its 46,000-ton Fuzhou plant and indefinitely idled its Botlek facility in the Netherlands, taking a $232 million restructuring charge. This is not a temporary pause, but a structural optimization of the industry's breakeven point.

The "Low-Cost" Moat: Vertical Integration vs. Technological Yield

In a commodity downcycle, raw material price volatility acts as the ultimate margin killer. The 2025 data explicitly identifies the true "low-cost leader" through the lens of supply chain architecture.

Tronox has successfully leveraged its vertical integration strategy, supplying its own titanium ore from captive mines in South Africa and Australia. This insulates the company from third-party mineral inflation, allowing Tronox to post an industry-leading Adjusted EBITDA margin of 11.6%.

Conversely, Chemours, which relies heavily on the technological yield of its proprietary chloride process, saw its $TiO_2$ segment margins compress to 6%, highly exposed to external ore costs. KRONOS, heavily dependent on the sluggish European market (46% of revenue) and lacking upstream immunity, saw margins collapse to approximately 2.1%. The data confirms that in a high-inflation environment, resource self-sufficiency eclipses pure technological efficiency.

Capital Allocation Efficiency and Portfolio Hedging

The cyclical severity of 2025 has forced companies to re-evaluate their capital allocation, utilizing non-correlated businesses as financial firewalls.

* Chemours’ Regulatory Cash Cow: Chemours’ financial resilience is heavily anchored by its Thermal & Specialized Solutions (TSS) segment. Driven by strict environmental regulations (such as the US AIM Act and EU F-Gas directives), its next-generation refrigerants business generated an exceptional 32% Adjusted EBITDA margin. This structural hedge effectively subsidized the underperforming $TiO_2$ division.

* Tronox’s High-Growth Pivot: Tronox is utilizing its robust capital expenditures ($341 million) to pioneer a second growth curve. By extracting Monazite from its titanium mining by-products, Tronox is strategically entering the Rare Earth Oxides (REO) supply chain. This strategic pivot targets the high-margin EV and wind power sectors, setting the stage for a potential valuation multiple reset.

* KRONOS’ Structural Vulnerability: Generating roughly 90% of its revenue purely from $TiO_2$, KRONOS completely lacks a counter-cyclical safety net. This extreme concentration resulted in a glaring $110.9 million net loss in 2025, demonstrating the lethal risk of an unhedged portfolio during an industry bottom.

Financial Health: Leverage, Liquidity, and Latent Liabilities

Beneath the operational metrics lie significant balance sheet risks. According to HDIN Research’s risk assessment, cash flow authenticity must be prioritized over paper profits.

Despite its operational moat, Tronox is navigating perilous financial leverage, with a Net Debt to Adjusted EBITDA ratio ballooning to 9.0x. Its recent $50 million "Inventory Financing Arrangement"—essentially utilizing inventory as collateral for short-term cash—signals acute liquidity friction. Meanwhile, Chemours faces profound ESG and governance headwinds. Beyond the shadow of past executive accounting manipulation regarding working capital, the company is battling mounting PFAS (per- and polyfluoroalkyl substances) environmental liabilities, which currently exceed $484 million and act as a continuous drain on free cash flow.

HDIN Viewpoint

At HDIN Research, we view 2025 as the ultimate stress test for the global Titanium Dioxide sector. The industry is currently trading short-term utilization for long-term survival. Tronox presents the most formidable operational moat but requires strict monitoring of its debt covenants. Chemours offers superior portfolio resilience, yet investors must discount its valuation due to latent environmental litigation. KRONOS, currently fighting a defensive war of attrition, remains the most vulnerable pure-play entity. Moving forward, competitive advantage will be dictated not by market share, but by capital allocation efficiency and resource independence.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Based on HDIN Research’s proprietary analysis of 2025 financial disclosures, the industry paradigm has fundamentally shifted from "scale expansion" to "cost resilience" and "structural hedging."

Figure The TiO2 Titan Triumvirate: 2025 Comparative Performance & Strategic Qutlook

Cyclical Headwinds and Aggressive Capacity RationalizationIn 2025, sustained high interest rates have frozen housing mobility, directly compressing downstream demand in architectural coatings and plastics. The strategic implication is clear: maintaining high utilization rates in a depressed market is financial suicide. Consequently, the industry is undergoing aggressive capacity out-clearing.

Instead of absorbing inventory holding costs, producers are prioritizing liquidity. KRONOS executed a drastic operational pivot, slashing its Q4 capacity utilization rate to a mere 55%. This deliberate sacrifice of fixed-cost absorption was necessary to aggressively drive down its Days Sales of Inventory (DSI) to 57 days.

Furthermore, the sector is witnessing the permanent elimination of high-cost assets. Chemours completed the decommissioning of its Kuan Yin facility (Taiwan, China), liquidating the land for approximately $360 million to pare down debt. Similarly, Tronox permanently shuttered its 46,000-ton Fuzhou plant and indefinitely idled its Botlek facility in the Netherlands, taking a $232 million restructuring charge. This is not a temporary pause, but a structural optimization of the industry's breakeven point.

The "Low-Cost" Moat: Vertical Integration vs. Technological Yield

In a commodity downcycle, raw material price volatility acts as the ultimate margin killer. The 2025 data explicitly identifies the true "low-cost leader" through the lens of supply chain architecture.

Tronox has successfully leveraged its vertical integration strategy, supplying its own titanium ore from captive mines in South Africa and Australia. This insulates the company from third-party mineral inflation, allowing Tronox to post an industry-leading Adjusted EBITDA margin of 11.6%.

Conversely, Chemours, which relies heavily on the technological yield of its proprietary chloride process, saw its $TiO_2$ segment margins compress to 6%, highly exposed to external ore costs. KRONOS, heavily dependent on the sluggish European market (46% of revenue) and lacking upstream immunity, saw margins collapse to approximately 2.1%. The data confirms that in a high-inflation environment, resource self-sufficiency eclipses pure technological efficiency.

Capital Allocation Efficiency and Portfolio Hedging

The cyclical severity of 2025 has forced companies to re-evaluate their capital allocation, utilizing non-correlated businesses as financial firewalls.

* Chemours’ Regulatory Cash Cow: Chemours’ financial resilience is heavily anchored by its Thermal & Specialized Solutions (TSS) segment. Driven by strict environmental regulations (such as the US AIM Act and EU F-Gas directives), its next-generation refrigerants business generated an exceptional 32% Adjusted EBITDA margin. This structural hedge effectively subsidized the underperforming $TiO_2$ division.

* Tronox’s High-Growth Pivot: Tronox is utilizing its robust capital expenditures ($341 million) to pioneer a second growth curve. By extracting Monazite from its titanium mining by-products, Tronox is strategically entering the Rare Earth Oxides (REO) supply chain. This strategic pivot targets the high-margin EV and wind power sectors, setting the stage for a potential valuation multiple reset.

* KRONOS’ Structural Vulnerability: Generating roughly 90% of its revenue purely from $TiO_2$, KRONOS completely lacks a counter-cyclical safety net. This extreme concentration resulted in a glaring $110.9 million net loss in 2025, demonstrating the lethal risk of an unhedged portfolio during an industry bottom.

Financial Health: Leverage, Liquidity, and Latent Liabilities

Beneath the operational metrics lie significant balance sheet risks. According to HDIN Research’s risk assessment, cash flow authenticity must be prioritized over paper profits.

Despite its operational moat, Tronox is navigating perilous financial leverage, with a Net Debt to Adjusted EBITDA ratio ballooning to 9.0x. Its recent $50 million "Inventory Financing Arrangement"—essentially utilizing inventory as collateral for short-term cash—signals acute liquidity friction. Meanwhile, Chemours faces profound ESG and governance headwinds. Beyond the shadow of past executive accounting manipulation regarding working capital, the company is battling mounting PFAS (per- and polyfluoroalkyl substances) environmental liabilities, which currently exceed $484 million and act as a continuous drain on free cash flow.

HDIN Viewpoint

At HDIN Research, we view 2025 as the ultimate stress test for the global Titanium Dioxide sector. The industry is currently trading short-term utilization for long-term survival. Tronox presents the most formidable operational moat but requires strict monitoring of its debt covenants. Chemours offers superior portfolio resilience, yet investors must discount its valuation due to latent environmental litigation. KRONOS, currently fighting a defensive war of attrition, remains the most vulnerable pure-play entity. Moving forward, competitive advantage will be dictated not by market share, but by capital allocation efficiency and resource independence.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com