2025 Global EMS/ODM Industry Outlook: AI Compute Infrastructure and the Bifurcation of Strategic Moats

Date : 2026-03-21

Reading : 137

The 2025 Electronic Manufacturing Services (EMS) and Original Design Manufacturing (ODM) landscape is experiencing a profound structural bifurcation. Driven by the explosive demand for AI compute infrastructure and the urgent need for supply chain regionalization, top-tier global manufacturers are no longer competing solely on cost. According to the latest analysis by HDIN Research, the industry has fundamentally split into two strategic tracks: hyperscaler-bound AI infrastructure leaders and highly regulated, High-Mix, Low-Volume (HMLV) niche specialists.

The strategic implication is clear: operational efficiency and embedded design capabilities are replacing pure manufacturing scale as the primary drivers of gross margin expansion and market valuation.

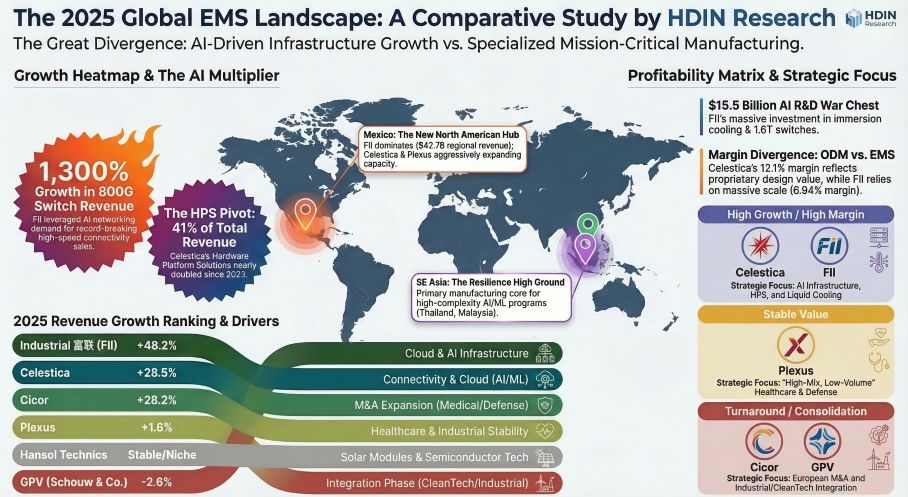

Figure The 2025 Global EMS Landscape

Strategic Pivots: The Value Chain Leap from EMS to ODM

Strategic Pivots: The Value Chain Leap from EMS to ODM

The traditional EMS model is giving way to Original Design Manufacturing (ODM) and Hardware Platform Solutions (HPS). Leading firms are successfully executing value chain leaps by integrating embedded design and vertical consolidation to lock in higher-margin revenues.

Celestica exemplifies this transition. By expanding its Hardware Platform Solutions (HPS) segment to 41% of its total revenue, Celestica has effectively transformed from a traditional contract manufacturer to a quasi-ODM, driving its gross margin to a robust 12.1%. By offering proprietary IP in rack-scale design and AI-load power management, Celestica commands a significant design premium. Similarly, Foxconn Industrial Internet (FII) is demonstrating immense technical sovereignty. Backed by $1.55 billion in R&D expenditure, FII is aggressively moving beyond server rack assembly into the foundational hardware layer, pioneering immersion liquid cooling systems and 1.6T high-speed switches with Co-Packaged Optics (CPO).

Sector Positioning: AI Hyperscaling vs. Task-Critical Niches

Sector positioning in 2025 is defined by a company’s ability to anchor itself to either secular hyper-growth or defensive, inelastic demand.

FII and Celestica have firmly positioned themselves at the core of the global AI server supply chain, deeply binding themselves to North American hyperscalers. FII’s cloud computing revenue surged exponentially, underpinned by unprecedented demand for AI servers and 800G network switches.

Conversely, European and North American peers like Plexus, Cicor, and GPV are deploying a defensive sector positioning strategy to weather cyclical headwinds. By focusing on HMLV markets—specifically healthcare, aerospace, defense, and CleanTech—these firms insulate themselves from the volatility of consumer electronics. Plexus derives over 80% of its revenue from mission-critical industrial and healthcare applications, creating high customer stickiness and a formidable regulatory barrier to entry.

Capital Allocation Efficiency & Supply Chain Regionalization

Capital allocation in 2025 is dominated by the global transition from a localized cost-arbitrage model to a "China + 1" and nearshoring strategy. Geopolitical risks, trade protectionism, and advanced chip export controls have made supply chain regionalization an absolute necessity.

FII and GPV are directing massive capital expenditures toward Mexico to capture North American nearshoring demand, with FII reporting over $42.7 billion in localized revenue from its Mexican operations. Meanwhile, Celestica and Plexus are aggressively expanding their manufacturing footprints in Southeast Asia, particularly in Malaysia and Thailand. This geographic diversification is not merely about sourcing cheap labor; it is a sophisticated exercise in complexity management, designed to ensure delivery resilience amid macroeconomic instability and power/water infrastructure constraints.

Financial Health: Navigating Inventory Risks and Liquidity

Beneath the surface of AI-driven revenue growth lies significant working capital volatility. HDIN Research's stress tests reveal diverging financial health profiles across the industry.

FII faces an aggressive operational strategy, with its inventory surging 77% year-over-year to $21.0 billion as it stockpiles AI components. While this secures supply for hyperscalers, it exposes the firm to substantial inventory impairment risks if AI chip architectures rapidly iterate.

In stark contrast, HMLV leaders demonstrate exceptional capital allocation efficiency. Plexus has mastered working capital management, utilizing structural offsets like customer advanced payments and material liability agreements to compress its cash conversion cycle (C2C) to just 63 days, shifting inventory risk back to the client. Meanwhile, Cicor has utilized highly efficient capital structuring to execute five major European acquisitions in 2025, maintaining a highly secure Net Debt/EBITDA leverage ratio of just 1.10x, proving that aggressive market consolidation can be achieved without compromising financial stability.

HDIN Viewpoint

From an institutional perspective, the 2025 EMS/ODM narrative is defined by the transition from scale-driven commoditization to technology-driven sovereignty. HDIN Research observes that while AI infrastructure provides an unprecedented growth ceiling, the true long-term winners will be those who master working capital efficiency and geographical risk hedging. Investors and industry stakeholders should look beyond top-line revenue inflation and critically evaluate a firm's pricing power, ODM IP accumulation, and its ability to seamlessly execute localized delivery across a fractured global supply chain.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

The strategic implication is clear: operational efficiency and embedded design capabilities are replacing pure manufacturing scale as the primary drivers of gross margin expansion and market valuation.

Figure The 2025 Global EMS Landscape

Strategic Pivots: The Value Chain Leap from EMS to ODMThe traditional EMS model is giving way to Original Design Manufacturing (ODM) and Hardware Platform Solutions (HPS). Leading firms are successfully executing value chain leaps by integrating embedded design and vertical consolidation to lock in higher-margin revenues.

Celestica exemplifies this transition. By expanding its Hardware Platform Solutions (HPS) segment to 41% of its total revenue, Celestica has effectively transformed from a traditional contract manufacturer to a quasi-ODM, driving its gross margin to a robust 12.1%. By offering proprietary IP in rack-scale design and AI-load power management, Celestica commands a significant design premium. Similarly, Foxconn Industrial Internet (FII) is demonstrating immense technical sovereignty. Backed by $1.55 billion in R&D expenditure, FII is aggressively moving beyond server rack assembly into the foundational hardware layer, pioneering immersion liquid cooling systems and 1.6T high-speed switches with Co-Packaged Optics (CPO).

Sector Positioning: AI Hyperscaling vs. Task-Critical Niches

Sector positioning in 2025 is defined by a company’s ability to anchor itself to either secular hyper-growth or defensive, inelastic demand.

FII and Celestica have firmly positioned themselves at the core of the global AI server supply chain, deeply binding themselves to North American hyperscalers. FII’s cloud computing revenue surged exponentially, underpinned by unprecedented demand for AI servers and 800G network switches.

Conversely, European and North American peers like Plexus, Cicor, and GPV are deploying a defensive sector positioning strategy to weather cyclical headwinds. By focusing on HMLV markets—specifically healthcare, aerospace, defense, and CleanTech—these firms insulate themselves from the volatility of consumer electronics. Plexus derives over 80% of its revenue from mission-critical industrial and healthcare applications, creating high customer stickiness and a formidable regulatory barrier to entry.

Capital Allocation Efficiency & Supply Chain Regionalization

Capital allocation in 2025 is dominated by the global transition from a localized cost-arbitrage model to a "China + 1" and nearshoring strategy. Geopolitical risks, trade protectionism, and advanced chip export controls have made supply chain regionalization an absolute necessity.

FII and GPV are directing massive capital expenditures toward Mexico to capture North American nearshoring demand, with FII reporting over $42.7 billion in localized revenue from its Mexican operations. Meanwhile, Celestica and Plexus are aggressively expanding their manufacturing footprints in Southeast Asia, particularly in Malaysia and Thailand. This geographic diversification is not merely about sourcing cheap labor; it is a sophisticated exercise in complexity management, designed to ensure delivery resilience amid macroeconomic instability and power/water infrastructure constraints.

Financial Health: Navigating Inventory Risks and Liquidity

Beneath the surface of AI-driven revenue growth lies significant working capital volatility. HDIN Research's stress tests reveal diverging financial health profiles across the industry.

FII faces an aggressive operational strategy, with its inventory surging 77% year-over-year to $21.0 billion as it stockpiles AI components. While this secures supply for hyperscalers, it exposes the firm to substantial inventory impairment risks if AI chip architectures rapidly iterate.

In stark contrast, HMLV leaders demonstrate exceptional capital allocation efficiency. Plexus has mastered working capital management, utilizing structural offsets like customer advanced payments and material liability agreements to compress its cash conversion cycle (C2C) to just 63 days, shifting inventory risk back to the client. Meanwhile, Cicor has utilized highly efficient capital structuring to execute five major European acquisitions in 2025, maintaining a highly secure Net Debt/EBITDA leverage ratio of just 1.10x, proving that aggressive market consolidation can be achieved without compromising financial stability.

HDIN Viewpoint

From an institutional perspective, the 2025 EMS/ODM narrative is defined by the transition from scale-driven commoditization to technology-driven sovereignty. HDIN Research observes that while AI infrastructure provides an unprecedented growth ceiling, the true long-term winners will be those who master working capital efficiency and geographical risk hedging. Investors and industry stakeholders should look beyond top-line revenue inflation and critically evaluate a firm's pricing power, ODM IP accumulation, and its ability to seamlessly execute localized delivery across a fractured global supply chain.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com