2025 Global Heavy Truck Market: Navigating Cyclical Headwinds and Structural Transformation

Date : 2026-03-18

Reading : 617

The global heavy truck sector has entered a critical inflection point in 2025, characterized by a complex collision of cyclical headwinds and structural transformation. As North American freight demand softens and global trade policy volatility escalates, an in-depth analysis by HDIN Research of industry titans—Daimler Truck, PACCAR, and TRATON—reveals a definitive shift in market dynamics.

Sector positioning is no longer dictated merely by manufacturing scale. Instead, the ultimate winners are leveraging capital allocation efficiency, software-defined ecosystems, and high-margin aftermarket services to insulate their balance sheets from cyclical downturns.

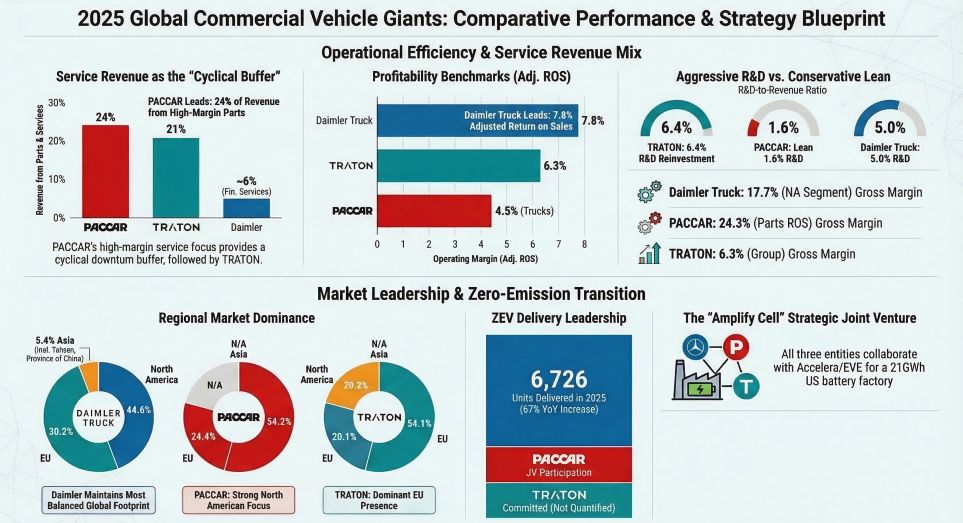

Figure 2025 Global Commercial Vehicle Giants: Comparative Performance & Strategy Blueprint

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

In 2025, macroeconomic pressures, notably the contraction in the North American Class 8 market and fluctuating tariff policies (such as the U.S. Section 232), universally suppressed new vehicle delivery volumes across the Big Three. However, their financial resilience varied significantly based on geographic exposure and revenue structures:

* Daimler Truck: Maintaining its position as the scale leader with $55.8 billion in group revenue, Daimler demonstrated the strongest geographic risk-hedging capabilities. While North American operations faced headwinds, an agile pivot to Asian market recoveries (+39% growth in China, +7% in India) and a robust 14% revenue surge in its global bus segment provided vital structural support.

* PACCAR: Despite heavy exposure to North America (54.2% of revenue) and a 27% drop in regional deliveries, PACCAR maintained unparalleled profitability through its PACCAR Parts division. Generating a staggering 24.3% Return on Sales (ROS), this aftermarket segment acted as the ultimate "cash cow," funding the company's dividend payouts and ongoing R&D without straining the core balance sheet.

* TRATON: Driven by its Scania premium brand and the aggressive rollout of the TRATON Modular System (TMS), the group achieved a resilient 6.3% adjusted ROS. TRATON is currently undergoing a massive internal integration phase, centralizing R&D to drive down common component costs across its Scania, MAN, and International brands.

Strategic Moats: The Shift to Full-Lifecycle Value

The historical business model of "selling hardware" has permanently shifted. To combat the margin-eroding effects of stringent emission regulations (e.g., Euro VII and EPA 2027), OEMs are aggressively building strategic moats around full-lifecycle value.

This transition is highly visible in their intelligent connectivity and autonomous driving investments. Daimler Truck is leading the charge in software standardization through "Coretura," its joint venture with Volvo Group, aiming to create an industry-wide software-defined vehicle platform. Meanwhile, TRATON has successfully initiated commercial Level 4 autonomous operations with safety drivers in the U.S., and PACCAR is utilizing its AI-driven PACCAR Connect system to deeply integrate with fleet operations, thereby locking customers into its highly profitable aftermarket parts network.

Furthermore, realizing the immense capital expenditure required for electrification, these fierce competitors are engaging in strategic "coopetition." The formation of Amplify Cell Technologies—a joint battery manufacturing venture among Daimler, PACCAR, and Accelera—highlights a mutual acknowledgment that sharing the financial burden of the supply chain transition is an operational necessity.

Decarbonization: A Divergence in Sector Positioning

While there is a consensus on the need for zero-emission vehicles (ZEVs), HDIN Research notes a sharp divergence in decarbonization technology roadmaps:

* TRATON operates on a strict "BEV-First" philosophy, focusing heavily on battery-electric efficiency and keeping hydrogen at a low priority.

* Daimler Truck remains steadfast in a "Dual-Track" approach, heavily investing in both BEV (e.g., eActros 600) and hydrogen fuel cell technology (FCEV) for long-haul applications.

* PACCAR adopts a pragmatic stance, focusing on squeezing maximum fuel efficiency out of its proprietary diesel engines while utilizing strategic joint ventures to manage its BEV transition risks.

HDIN Viewpoint: Hidden Financial Risks in the Transition Era

As an independent third-party consulting firm, HDIN Research urges investors and industry stakeholders to look beyond top-line revenue and scrutinize the forensic accounting metrics tied to this industry transition.

We highlight a significant divergence in R&D capitalization strategies. TRATON currently capitalizes an aggressive 44.5% of its R&D expenditures, significantly higher than Daimler Truck’s 12%. During a market downcycle, excessive capitalization can artificially smooth current earnings but creates a severe risk of future asset impairments if market adoption of new EV models underperforms.

Conversely, Daimler Truck exhibited prudent financial conservatism in 2025 by recognizing a $246 million non-cash write-down on capitalized EV development costs due to a slower-than-expected transition in the U.S. market. Furthermore, while PACCAR boasts a highly localized supply chain to dodge geopolitical tariffs, its public filings reveal a heavy, concentrated reliance on a few key suppliers (such as Cummins and ZF). Any disruption here presents a material risk that lacks the natural hedging found in Daimler's globally dispersed production network.

As we move deeper into the decade, the heavy truck sector will reward those who balance aggressive technological innovation with rigorous capital discipline and supply chain resilience.

Presentation download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports to help business leaders make informed, data-driven strategic decisions.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Sector positioning is no longer dictated merely by manufacturing scale. Instead, the ultimate winners are leveraging capital allocation efficiency, software-defined ecosystems, and high-margin aftermarket services to insulate their balance sheets from cyclical downturns.

Figure 2025 Global Commercial Vehicle Giants: Comparative Performance & Strategy Blueprint

Financial Health & Capital Allocation EfficiencyIn 2025, macroeconomic pressures, notably the contraction in the North American Class 8 market and fluctuating tariff policies (such as the U.S. Section 232), universally suppressed new vehicle delivery volumes across the Big Three. However, their financial resilience varied significantly based on geographic exposure and revenue structures:

* Daimler Truck: Maintaining its position as the scale leader with $55.8 billion in group revenue, Daimler demonstrated the strongest geographic risk-hedging capabilities. While North American operations faced headwinds, an agile pivot to Asian market recoveries (+39% growth in China, +7% in India) and a robust 14% revenue surge in its global bus segment provided vital structural support.

* PACCAR: Despite heavy exposure to North America (54.2% of revenue) and a 27% drop in regional deliveries, PACCAR maintained unparalleled profitability through its PACCAR Parts division. Generating a staggering 24.3% Return on Sales (ROS), this aftermarket segment acted as the ultimate "cash cow," funding the company's dividend payouts and ongoing R&D without straining the core balance sheet.

* TRATON: Driven by its Scania premium brand and the aggressive rollout of the TRATON Modular System (TMS), the group achieved a resilient 6.3% adjusted ROS. TRATON is currently undergoing a massive internal integration phase, centralizing R&D to drive down common component costs across its Scania, MAN, and International brands.

Strategic Moats: The Shift to Full-Lifecycle Value

The historical business model of "selling hardware" has permanently shifted. To combat the margin-eroding effects of stringent emission regulations (e.g., Euro VII and EPA 2027), OEMs are aggressively building strategic moats around full-lifecycle value.

This transition is highly visible in their intelligent connectivity and autonomous driving investments. Daimler Truck is leading the charge in software standardization through "Coretura," its joint venture with Volvo Group, aiming to create an industry-wide software-defined vehicle platform. Meanwhile, TRATON has successfully initiated commercial Level 4 autonomous operations with safety drivers in the U.S., and PACCAR is utilizing its AI-driven PACCAR Connect system to deeply integrate with fleet operations, thereby locking customers into its highly profitable aftermarket parts network.

Furthermore, realizing the immense capital expenditure required for electrification, these fierce competitors are engaging in strategic "coopetition." The formation of Amplify Cell Technologies—a joint battery manufacturing venture among Daimler, PACCAR, and Accelera—highlights a mutual acknowledgment that sharing the financial burden of the supply chain transition is an operational necessity.

Decarbonization: A Divergence in Sector Positioning

While there is a consensus on the need for zero-emission vehicles (ZEVs), HDIN Research notes a sharp divergence in decarbonization technology roadmaps:

* TRATON operates on a strict "BEV-First" philosophy, focusing heavily on battery-electric efficiency and keeping hydrogen at a low priority.

* Daimler Truck remains steadfast in a "Dual-Track" approach, heavily investing in both BEV (e.g., eActros 600) and hydrogen fuel cell technology (FCEV) for long-haul applications.

* PACCAR adopts a pragmatic stance, focusing on squeezing maximum fuel efficiency out of its proprietary diesel engines while utilizing strategic joint ventures to manage its BEV transition risks.

HDIN Viewpoint: Hidden Financial Risks in the Transition Era

As an independent third-party consulting firm, HDIN Research urges investors and industry stakeholders to look beyond top-line revenue and scrutinize the forensic accounting metrics tied to this industry transition.

We highlight a significant divergence in R&D capitalization strategies. TRATON currently capitalizes an aggressive 44.5% of its R&D expenditures, significantly higher than Daimler Truck’s 12%. During a market downcycle, excessive capitalization can artificially smooth current earnings but creates a severe risk of future asset impairments if market adoption of new EV models underperforms.

Conversely, Daimler Truck exhibited prudent financial conservatism in 2025 by recognizing a $246 million non-cash write-down on capitalized EV development costs due to a slower-than-expected transition in the U.S. market. Furthermore, while PACCAR boasts a highly localized supply chain to dodge geopolitical tariffs, its public filings reveal a heavy, concentrated reliance on a few key suppliers (such as Cummins and ZF). Any disruption here presents a material risk that lacks the natural hedging found in Daimler's globally dispersed production network.

As we move deeper into the decade, the heavy truck sector will reward those who balance aggressive technological innovation with rigorous capital discipline and supply chain resilience.

Presentation download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports to help business leaders make informed, data-driven strategic decisions.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com