Kodiak AI 2025 Annual Review: Strategic DaaS Pivot Amid Solvency Bottlenecks

Date : 2026-03-20

Reading : 106

Kodiak AI’s 2025 fiscal year represents a watershed moment defined by aggressive technological validation juxtaposed against severe liquidity pressures. While headline figures reveal a staggering $585.5 million net loss, HDIN Research's forensic analysis indicates that this deficit is primarily an accounting artifact driven by non-cash SPAC merger adjustments. The underlying strategic narrative is far more nuanced: Kodiak is executing a critical pivot from an asset-heavy autonomous fleet operator to an asset-light, high-margin Driver-as-a-Service (DaaS) provider. However, with a cash runway extending only through the fourth quarter of 2026, the company faces a race against time to bridge the gap between technical readiness and financial self-sustainability.

Figure Kodiak Al 2025: 0perational & Financial Performance At A Glance

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

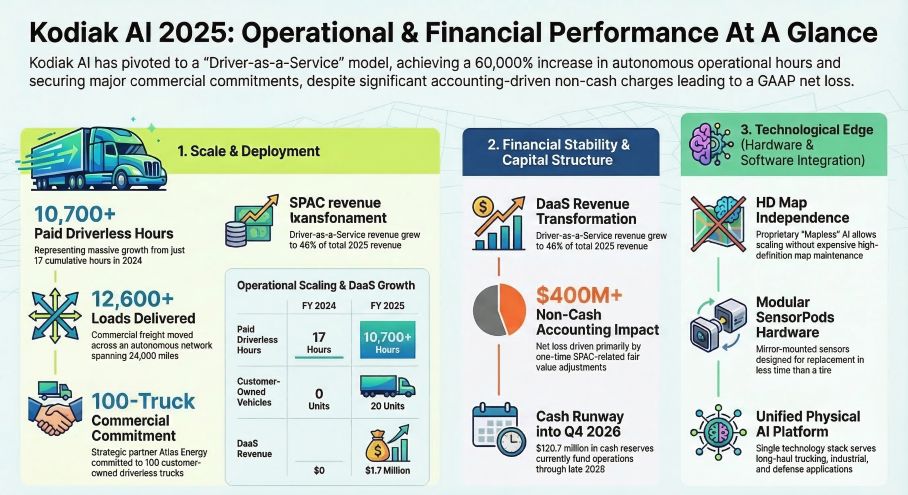

A surface-level reading of Kodiak’s financials shows a 75% year-over-year revenue contraction to $3.8 million, alongside a 7.4x expansion in net losses. The "so what" behind these numbers, however, reveals a planned transitional phase rather than operational decay.

The revenue drop was anticipated, stemming from the cyclical completion of U.S. Army developmental contracts. Meanwhile, over 81% of the $585.5 million net loss was driven by non-cash reverse recapitalization events, including SAFE and warrant fair-value adjustments tied to its public listing.

In terms of capital allocation efficiency, Kodiak’s actual operating cash outflow stood at $94.4 million. To mitigate near-term capital expenditure (CapEx) pressures, the company executed a $30 million debt restructuring in late 2025. While this extends the interest-only period to 30 months, it introduces stringent financial leverage: the effective interest rate exceeds 10%, and the loan is collateralized against Kodiak’s core intellectual property. Without subsequent equity or debt injections, Kodiak's $120.7 million cash reserve establishes a hard solvency deadline of Q4 2026, triggering an explicitly stated "going concern" risk.

Strategic Pivots: The Transition to Asset-Light DaaS

Kodiak recognized that scaling an autonomous trucking fleet organically is a capital-incinerating endeavor. Consequently, 2025 marked the operationalization of its Driver-as-a-Service (DaaS) model.

By licensing the Kodiak Driver system to client-owned fleets—such as its landmark partnership with Atlas Energy Solutions in the Permian Basin—Kodiak effectively externalizes truck procurement, depreciation, and routine maintenance costs to its customers. The operational data validates this strategic pivot: Kodiak logged over 10,700 paid driverless hours in 2025 (up exponentially from just 17 hours in 2024) and successfully deployed 20 client-owned Level 4 autonomous trucks. This shift lays the groundwork for recurring, high-margin software-like revenue, insulating the balance sheet from the heavy CapEx traditionally associated with the logistics sector.

Sector Positioning & Strategic Moats

In a highly fragmented autonomous vehicle market, Kodiak has carved out distinct strategic moats that differentiate it from competitors like Aurora Innovation and Gatik.

The cornerstone of Kodiak’s sector positioning is its HD Map Independence. While peers rely heavily on pre-mapped routes, Kodiak utilizes a mapless, Physical AI-driven architecture supported by Vision Language Models (VLMs). This enables the system to navigate highly unstructured, dynamic environments—from the unpaved roads of Texas oil fields to complex military theaters.

Furthermore, Kodiak’s modular "SensorPods" architecture allows for plug-and-play sensor replacement in under the time it takes to change a tire. This maximizes fleet uptime, a critical KPI for converting legacy logistics providers into DaaS subscribers. By adopting a "dual-use" market strategy that captures both defense contracts and commercial industrial logistics, Kodiak is generating early-stage cash flow while systematically preparing for its ultimate objective: fully driverless long-haul highway operations by late 2026.

Cyclical Headwinds & Regulatory Roadblocks

Despite robust technological milestones, Kodiak’s path to profitability by 2028 is threatened by macroeconomic and regulatory cyclical headwinds.

Currently, only 24 U.S. states have legislative frameworks permitting autonomous trucking. Key logistical arteries, such as California, remain mired in regulatory limbo. Concurrently, organized labor unions are aggressively lobbying across 20 states to mandate human safety operators, presenting a formidable political headwind to nationwide scale.

Additionally, Kodiak faces supply chain vulnerabilities. The company relies heavily on hardware components that are currently exposed to tariffs ranging from 10% to 125%. If geopolitical trade tensions escalate, the anticipated margin expansion of the DaaS model could be severely compressed by inflated hardware integration costs.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Kodiak AI as a "technology-rich, liquidity-fragile" pioneer. The company’s mapless cognitive architecture and its decisive pivot to the DaaS model represent best-in-class strategic foresight. The validation of its system in the harsh conditions of the Permian Basin proves that its physical AI works outside of sterile testing environments.

However, technology alone does not guarantee survival. The ultimate litmus test for Kodiak will not be its autonomous readiness, but its financial engineering over the next 12 months. Management must successfully close a major funding round before the Q4 2026 cash cliff. Investors and strategic partners should closely monitor the horizontal scalability of the Atlas Energy deployment; if Kodiak can replicate this DaaS blueprint with Tier-1 logistics carriers swiftly, it will cement its position as a dominant force in the autonomous freight revolution.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Kodiak Al 2025: 0perational & Financial Performance At A Glance

Financial Health & Capital Allocation EfficiencyA surface-level reading of Kodiak’s financials shows a 75% year-over-year revenue contraction to $3.8 million, alongside a 7.4x expansion in net losses. The "so what" behind these numbers, however, reveals a planned transitional phase rather than operational decay.

The revenue drop was anticipated, stemming from the cyclical completion of U.S. Army developmental contracts. Meanwhile, over 81% of the $585.5 million net loss was driven by non-cash reverse recapitalization events, including SAFE and warrant fair-value adjustments tied to its public listing.

In terms of capital allocation efficiency, Kodiak’s actual operating cash outflow stood at $94.4 million. To mitigate near-term capital expenditure (CapEx) pressures, the company executed a $30 million debt restructuring in late 2025. While this extends the interest-only period to 30 months, it introduces stringent financial leverage: the effective interest rate exceeds 10%, and the loan is collateralized against Kodiak’s core intellectual property. Without subsequent equity or debt injections, Kodiak's $120.7 million cash reserve establishes a hard solvency deadline of Q4 2026, triggering an explicitly stated "going concern" risk.

Strategic Pivots: The Transition to Asset-Light DaaS

Kodiak recognized that scaling an autonomous trucking fleet organically is a capital-incinerating endeavor. Consequently, 2025 marked the operationalization of its Driver-as-a-Service (DaaS) model.

By licensing the Kodiak Driver system to client-owned fleets—such as its landmark partnership with Atlas Energy Solutions in the Permian Basin—Kodiak effectively externalizes truck procurement, depreciation, and routine maintenance costs to its customers. The operational data validates this strategic pivot: Kodiak logged over 10,700 paid driverless hours in 2025 (up exponentially from just 17 hours in 2024) and successfully deployed 20 client-owned Level 4 autonomous trucks. This shift lays the groundwork for recurring, high-margin software-like revenue, insulating the balance sheet from the heavy CapEx traditionally associated with the logistics sector.

Sector Positioning & Strategic Moats

In a highly fragmented autonomous vehicle market, Kodiak has carved out distinct strategic moats that differentiate it from competitors like Aurora Innovation and Gatik.

The cornerstone of Kodiak’s sector positioning is its HD Map Independence. While peers rely heavily on pre-mapped routes, Kodiak utilizes a mapless, Physical AI-driven architecture supported by Vision Language Models (VLMs). This enables the system to navigate highly unstructured, dynamic environments—from the unpaved roads of Texas oil fields to complex military theaters.

Furthermore, Kodiak’s modular "SensorPods" architecture allows for plug-and-play sensor replacement in under the time it takes to change a tire. This maximizes fleet uptime, a critical KPI for converting legacy logistics providers into DaaS subscribers. By adopting a "dual-use" market strategy that captures both defense contracts and commercial industrial logistics, Kodiak is generating early-stage cash flow while systematically preparing for its ultimate objective: fully driverless long-haul highway operations by late 2026.

Cyclical Headwinds & Regulatory Roadblocks

Despite robust technological milestones, Kodiak’s path to profitability by 2028 is threatened by macroeconomic and regulatory cyclical headwinds.

Currently, only 24 U.S. states have legislative frameworks permitting autonomous trucking. Key logistical arteries, such as California, remain mired in regulatory limbo. Concurrently, organized labor unions are aggressively lobbying across 20 states to mandate human safety operators, presenting a formidable political headwind to nationwide scale.

Additionally, Kodiak faces supply chain vulnerabilities. The company relies heavily on hardware components that are currently exposed to tariffs ranging from 10% to 125%. If geopolitical trade tensions escalate, the anticipated margin expansion of the DaaS model could be severely compressed by inflated hardware integration costs.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Kodiak AI as a "technology-rich, liquidity-fragile" pioneer. The company’s mapless cognitive architecture and its decisive pivot to the DaaS model represent best-in-class strategic foresight. The validation of its system in the harsh conditions of the Permian Basin proves that its physical AI works outside of sterile testing environments.

However, technology alone does not guarantee survival. The ultimate litmus test for Kodiak will not be its autonomous readiness, but its financial engineering over the next 12 months. Management must successfully close a major funding round before the Q4 2026 cash cliff. Investors and strategic partners should closely monitor the horizontal scalability of the Atlas Energy deployment; if Kodiak can replicate this DaaS blueprint with Tier-1 logistics carriers swiftly, it will cement its position as a dominant force in the autonomous freight revolution.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com