Serve Robotics 2025: Navigating L4 Scaling, Strategic Moats, and Unit Economic Realities

Date : 2026-03-18

Reading : 108

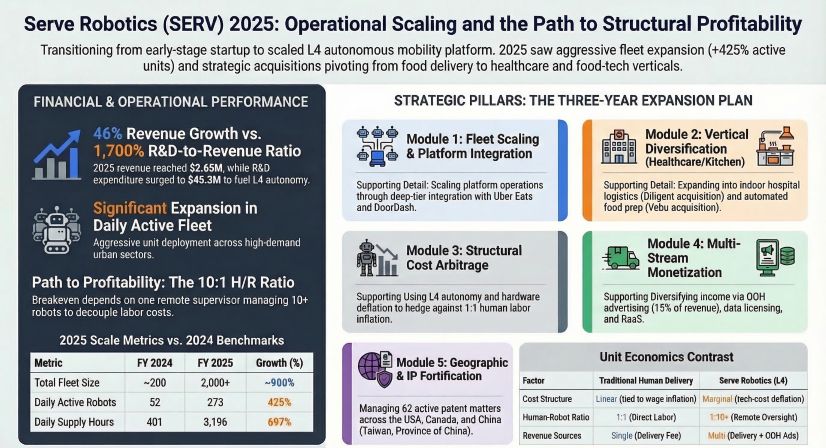

Serve Robotics Inc. has reached a critical inflection point in its commercialization journey. While top-line revenue expanded by 46% to $2.65 million in 2025, it was heavily eclipsed by a $15.38 million gross loss, underscoring the severe unit economic penalties of early-stage fleet deployment. HDIN Research’s deep-dive analysis of the 2025 10-K filings reveals a company caught between aggressive capital expenditure-driven expansion and extreme supply chain and regulatory vulnerabilities. Serve’s ultimate survival relies on seamlessly transitioning its 2,000-unit fleet from a state of "deployment" to "high-frequency monetization."

Figure Serve Robotics (SERV) 2025: Operational Scaling and the Path to Structural Profitability

Financial Health and Capital Allocation Efficiency

Financial Health and Capital Allocation Efficiency

Serve Robotics exhibits the classic financial architecture of an early-stage, deep-tech enterprise: structural cash burn prioritizing market capture over immediate margin realization. The company reported a net loss of $101.36 million in 2025, burdened by a staggering negative gross margin of 580%. This indicates that every dollar of revenue currently requires nearly six dollars in direct costs, primarily driven by early network infrastructure, heavy depreciation, and high localized labor costs.

However, capital allocation efficiency is showing signs of a strategic pivot. Management plans to reduce Capital Expenditure (CapEx) from $37.33 million in 2025 to approximately $25 million in 2026. This contraction signals a necessary shift from a "hardware build-out phase" to an "operational optimization phase." Bolstered by recent equity financing, the company currently maintains $233 million in total liquidity. At a historical operating cash outflow of ~$80 million annually, Serve commands a theoretical cash runway of nearly 24 months—provided that share-based compensation (which accounted for nearly 47% of 2025 R&D spend) continues to substitute for immediate cash expenditures without triggering terminal talent attrition.

Sector Positioning and Strategic Pivots

Serve is aggressively moving beyond the low-margin constraints of pure food delivery, attempting to establish a robust Autonomous Mobility Platform. The company’s sector positioning is being redefined through a sophisticated Robot-as-a-Service (RaaS) transition, driven by targeted M&A activity:

* Healthcare Automation Logistics: The $29.0 million acquisition of Diligent Robotics (and its Moxi robot) transitions Serve from outdoor sidewalks to high-margin, B2B indoor clinical environments, effectively unlocking recurring software licensing revenue.

* Vertical Integration in Food Tech: Acquiring Vebu Inc. enables Serve to capture upstream value in food preparation automation.

* Algorithmic and Operational Synergies: The integrations of Vayu Robotics (LLM-based urban navigation) and Voysys (ultra-low latency teleoperations) directly fortify Serve’s Level 4 (L4) autonomy stack.

Furthermore, out-of-home (OOH) advertising generated 15% of Serve's 2025 revenues. This secondary monetization of physical assets is a vital strategic moat that must be aggressively scaled to subsidize core delivery costs.

Cyclical Headwinds and Operational Bottlenecks

Despite structural labor cost advantages—where robotics theoretically counteracts gig-worker wage inflation via tech cost deflation—Serve faces intense cyclical headwinds and operational friction:

* Regulatory Fragmentation (Existential Risk): Market access is highly siloed. While over 25 states permit Personal Delivery Devices (PDDs), major hubs like New York City and Santa Monica have banned sidewalk robots. ADA compliance incidents could trigger rapid, localized shutdowns.

* Supply Chain Concentration (Structural Risk): The firm’s L4 autonomy relies on single-source suppliers for critical components, namely NVIDIA (processors) and Ouster (LiDAR). In an era of geopolitical volatility, this concentration leaves 2026 hardware iteration plans highly exposed to bottleneck pricing and delays.

* Asset Utilization Deficit: In 2025, daily active robots averaged only 273 units—less than 15% of the total deployed fleet of 2,000+. This massive drag on asset turnover means depreciation costs are vastly outpacing revenue generation.

HDIN Viewpoint: The Path to Breakeven

As an independent market consulting firm, HDIN Research views Serve Robotics’ theoretical cost advantage over human labor as fundamentally sound but empirically unproven. To cross the chasm from cash-burning pioneer to a profitable enterprise, Serve must conquer three "death variables" by 2026:

1. The Human-to-Robot (H/R) Ratio: The entire unit economic thesis rests on L4 autonomy effectively allowing one remote supervisor to manage 10+ robots simultaneously. If "humans-in-the-loop" intervention remains high due to edge cases, the labor arbitrage model collapses.

2. Asset Utilization: Fleet utilization must scale from the current 15% to above 60% to absorb the $8.2 million in annual depreciation.

3. Alternative Revenue Scaling: Delivery fees alone cannot bridge a 580% gross loss. OOH advertising and data monetization must become primary, rather than tertiary, revenue streams.

Failure to optimize these specific operational levers will inevitably force Serve back into the capital markets, risking severe equity dilution for current shareholders before profitability is ever realized.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Serve Robotics (SERV) 2025: Operational Scaling and the Path to Structural Profitability

Financial Health and Capital Allocation EfficiencyServe Robotics exhibits the classic financial architecture of an early-stage, deep-tech enterprise: structural cash burn prioritizing market capture over immediate margin realization. The company reported a net loss of $101.36 million in 2025, burdened by a staggering negative gross margin of 580%. This indicates that every dollar of revenue currently requires nearly six dollars in direct costs, primarily driven by early network infrastructure, heavy depreciation, and high localized labor costs.

However, capital allocation efficiency is showing signs of a strategic pivot. Management plans to reduce Capital Expenditure (CapEx) from $37.33 million in 2025 to approximately $25 million in 2026. This contraction signals a necessary shift from a "hardware build-out phase" to an "operational optimization phase." Bolstered by recent equity financing, the company currently maintains $233 million in total liquidity. At a historical operating cash outflow of ~$80 million annually, Serve commands a theoretical cash runway of nearly 24 months—provided that share-based compensation (which accounted for nearly 47% of 2025 R&D spend) continues to substitute for immediate cash expenditures without triggering terminal talent attrition.

Sector Positioning and Strategic Pivots

Serve is aggressively moving beyond the low-margin constraints of pure food delivery, attempting to establish a robust Autonomous Mobility Platform. The company’s sector positioning is being redefined through a sophisticated Robot-as-a-Service (RaaS) transition, driven by targeted M&A activity:

* Healthcare Automation Logistics: The $29.0 million acquisition of Diligent Robotics (and its Moxi robot) transitions Serve from outdoor sidewalks to high-margin, B2B indoor clinical environments, effectively unlocking recurring software licensing revenue.

* Vertical Integration in Food Tech: Acquiring Vebu Inc. enables Serve to capture upstream value in food preparation automation.

* Algorithmic and Operational Synergies: The integrations of Vayu Robotics (LLM-based urban navigation) and Voysys (ultra-low latency teleoperations) directly fortify Serve’s Level 4 (L4) autonomy stack.

Furthermore, out-of-home (OOH) advertising generated 15% of Serve's 2025 revenues. This secondary monetization of physical assets is a vital strategic moat that must be aggressively scaled to subsidize core delivery costs.

Cyclical Headwinds and Operational Bottlenecks

Despite structural labor cost advantages—where robotics theoretically counteracts gig-worker wage inflation via tech cost deflation—Serve faces intense cyclical headwinds and operational friction:

* Regulatory Fragmentation (Existential Risk): Market access is highly siloed. While over 25 states permit Personal Delivery Devices (PDDs), major hubs like New York City and Santa Monica have banned sidewalk robots. ADA compliance incidents could trigger rapid, localized shutdowns.

* Supply Chain Concentration (Structural Risk): The firm’s L4 autonomy relies on single-source suppliers for critical components, namely NVIDIA (processors) and Ouster (LiDAR). In an era of geopolitical volatility, this concentration leaves 2026 hardware iteration plans highly exposed to bottleneck pricing and delays.

* Asset Utilization Deficit: In 2025, daily active robots averaged only 273 units—less than 15% of the total deployed fleet of 2,000+. This massive drag on asset turnover means depreciation costs are vastly outpacing revenue generation.

HDIN Viewpoint: The Path to Breakeven

As an independent market consulting firm, HDIN Research views Serve Robotics’ theoretical cost advantage over human labor as fundamentally sound but empirically unproven. To cross the chasm from cash-burning pioneer to a profitable enterprise, Serve must conquer three "death variables" by 2026:

1. The Human-to-Robot (H/R) Ratio: The entire unit economic thesis rests on L4 autonomy effectively allowing one remote supervisor to manage 10+ robots simultaneously. If "humans-in-the-loop" intervention remains high due to edge cases, the labor arbitrage model collapses.

2. Asset Utilization: Fleet utilization must scale from the current 15% to above 60% to absorb the $8.2 million in annual depreciation.

3. Alternative Revenue Scaling: Delivery fees alone cannot bridge a 580% gross loss. OOH advertising and data monetization must become primary, rather than tertiary, revenue streams.

Failure to optimize these specific operational levers will inevitably force Serve back into the capital markets, risking severe equity dilution for current shareholders before profitability is ever realized.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com