Rheinmetall 2025: From European Supplier to Global

Date : 2026-03-19

Reading : 1264

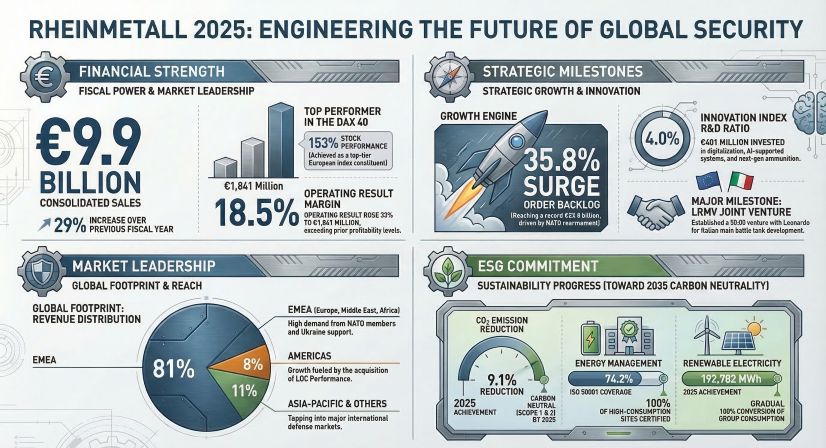

Rheinmetall’s 2025 fiscal year marks a definitive inflection point in the global defense landscape. Bolstered by a historic geopolitical premium, the company achieved a 28.8% revenue surge to $11.23 billion, underscored by an unprecedented 2.0 Book-to-Bill ratio. However, as management aggressively elevates its 2030 revenue target to $56.53 billion (approx. €500 billion), HDIN Research notes that the company's future hinges not merely on acquiring orders, but on mastering capital allocation efficiency and overcoming acute supply chain headwinds to execute a staggering 30% CAGR over the next five years.

Figure RHEINMETALL 2025: ENGINEERING THE FUTURE OF GLOBAL SECURITY

Strategic Pivots: The Dawn of "Software-Defined Defence"

Strategic Pivots: The Dawn of "Software-Defined Defence"

Rheinmetall has successfully completed a generational transition from an industrial automotive supplier to a pure-play defense technology hegemon. A critical component of this strategic pivot was the divestment of its civilian Power Systems division. By recording a $401 million impairment charge on these discontinued operations in late 2025, management executed a classic "big bath" accounting maneuver—clearing the balance sheet to pave the way for unencumbered, high-margin defense earnings in 2026.

More importantly, the company is aggressively expanding its strategic moats beyond traditional hardware. Through its 51% stake in blackned GmbH and the integration of the TACTICAL CORE middleware, Rheinmetall is spearheading the "Software-Defined Defence" revolution. Coupled with its space reconnaissance joint venture (ICEYE) and the market-leading Skyranger/Skynex anti-drone systems, the imminent organizational split of its Electronic Solutions division signals a deliberate move to detach high-growth digital assets from traditional hardware valuations, thereby commanding a structural premium in the market.

Sector Positioning and Capital Allocation Efficiency

Rheinmetall’s sector positioning is currently defined by a monopolistic pricing power, particularly within its Weapon and Ammunition division. This segment delivered an astonishing 29.3% operating margin in 2025. This profitability is not merely a byproduct of scale; it reflects robust inflation immunity achieved through Price Adjustment Clauses, allowing the firm to seamlessly pass raw material and energy costs onto sovereign clients.

From a capital allocation perspective, Rheinmetall’s financial health is operating at peak efficiency, driven by a highly lucrative "prepayment-driven" model. In 2025, a $2.01 billion surge in customer prepayments (contract liabilities) perfectly offset an $828 million working capital requirement for inventory build-ups. Consequently, the company transformed a $1.46 billion net debt position in 2024 into a $417 million net liquidity surplus by the end of 2025. This self-funding mechanism provided ample runway for a massive $990 million CapEx deployment—equating to 8.8% of sales—heavily targeted toward the new Unterlüß ammunition facility and US footprint expansions.

Cyclical Headwinds and Execution Risks

Despite a staggering $72.09 billion order backlog providing over six years of revenue visibility, translating this into the targeted $56.53 billion top-line by 2030 introduces profound operational risks.

The primary cyclical headwinds are rooted in supply chain bottlenecks and geopolitical volatility. The insatiable demand for 155mm artillery shells—which Rheinmetall is attempting to meet via a 350,000-round annual capacity expansion—is highly vulnerable to upstream shortages in nitrocellulose, explosives, and rare earth materials. Furthermore, while the company maintains strict compliance protocols globally, its sprawling supply chain—including operational hubs like Rheinmetall China Holding—requires continuous monitoring against shifting US tariff policies and global trade barriers. Any diplomatic de-escalation in Eastern Europe could also test the political durability of NATO’s 2%-5% GDP defense spending commitments, potentially softening long-term demand.

HDIN Viewpoint: "Capacity is Sovereignty"

In the assessment of HDIN Research, Rheinmetall is currently a "gold miner sitting on a volcano." The company has brilliantly capitalized on the European Defense Technological and Industrial Base (EDTIB) integration to transition from a regional vendor to the "Chief Architect" of NATO's land and digital warfare standards.

While the 2025 financial results showcase an impenetrable order book moat, institutional investors must scrutinize the transition from customized engineering to serial mass production. The true determinant of Rheinmetall’s valuation in 2026 and beyond will be its execution resilience: the ability to bring new global facilities online at unprecedented speeds while shielding its supply chain from macroeconomic fragmentation.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure RHEINMETALL 2025: ENGINEERING THE FUTURE OF GLOBAL SECURITY

Strategic Pivots: The Dawn of "Software-Defined Defence"Rheinmetall has successfully completed a generational transition from an industrial automotive supplier to a pure-play defense technology hegemon. A critical component of this strategic pivot was the divestment of its civilian Power Systems division. By recording a $401 million impairment charge on these discontinued operations in late 2025, management executed a classic "big bath" accounting maneuver—clearing the balance sheet to pave the way for unencumbered, high-margin defense earnings in 2026.

More importantly, the company is aggressively expanding its strategic moats beyond traditional hardware. Through its 51% stake in blackned GmbH and the integration of the TACTICAL CORE middleware, Rheinmetall is spearheading the "Software-Defined Defence" revolution. Coupled with its space reconnaissance joint venture (ICEYE) and the market-leading Skyranger/Skynex anti-drone systems, the imminent organizational split of its Electronic Solutions division signals a deliberate move to detach high-growth digital assets from traditional hardware valuations, thereby commanding a structural premium in the market.

Sector Positioning and Capital Allocation Efficiency

Rheinmetall’s sector positioning is currently defined by a monopolistic pricing power, particularly within its Weapon and Ammunition division. This segment delivered an astonishing 29.3% operating margin in 2025. This profitability is not merely a byproduct of scale; it reflects robust inflation immunity achieved through Price Adjustment Clauses, allowing the firm to seamlessly pass raw material and energy costs onto sovereign clients.

From a capital allocation perspective, Rheinmetall’s financial health is operating at peak efficiency, driven by a highly lucrative "prepayment-driven" model. In 2025, a $2.01 billion surge in customer prepayments (contract liabilities) perfectly offset an $828 million working capital requirement for inventory build-ups. Consequently, the company transformed a $1.46 billion net debt position in 2024 into a $417 million net liquidity surplus by the end of 2025. This self-funding mechanism provided ample runway for a massive $990 million CapEx deployment—equating to 8.8% of sales—heavily targeted toward the new Unterlüß ammunition facility and US footprint expansions.

Cyclical Headwinds and Execution Risks

Despite a staggering $72.09 billion order backlog providing over six years of revenue visibility, translating this into the targeted $56.53 billion top-line by 2030 introduces profound operational risks.

The primary cyclical headwinds are rooted in supply chain bottlenecks and geopolitical volatility. The insatiable demand for 155mm artillery shells—which Rheinmetall is attempting to meet via a 350,000-round annual capacity expansion—is highly vulnerable to upstream shortages in nitrocellulose, explosives, and rare earth materials. Furthermore, while the company maintains strict compliance protocols globally, its sprawling supply chain—including operational hubs like Rheinmetall China Holding—requires continuous monitoring against shifting US tariff policies and global trade barriers. Any diplomatic de-escalation in Eastern Europe could also test the political durability of NATO’s 2%-5% GDP defense spending commitments, potentially softening long-term demand.

HDIN Viewpoint: "Capacity is Sovereignty"

In the assessment of HDIN Research, Rheinmetall is currently a "gold miner sitting on a volcano." The company has brilliantly capitalized on the European Defense Technological and Industrial Base (EDTIB) integration to transition from a regional vendor to the "Chief Architect" of NATO's land and digital warfare standards.

While the 2025 financial results showcase an impenetrable order book moat, institutional investors must scrutinize the transition from customized engineering to serial mass production. The true determinant of Rheinmetall’s valuation in 2026 and beyond will be its execution resilience: the ability to bring new global facilities online at unprecedented speeds while shielding its supply chain from macroeconomic fragmentation.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com