Amazon vs. Walmart 2025: The Paradigm Clash of Capital Efficiency and Strategic Moats

Date : 2026-03-19

Reading : 94

The battle for global retail supremacy has fundamentally shifted from a pure race for top-line scale to a sophisticated contest of capital allocation efficiency and ecosystem monetization. Based on an exhaustive MECE-framework analysis of the 2025 fiscal data, HDIN Research reveals that while Walmart retains the crown for absolute revenue volume ($713.1 billion), Amazon’s retail division ($588.1 billion) has constructed an unassailable financial fortress. By weaponizing its supply chain and cross-subsidizing operations through high-margin tech engines, Amazon has engineered a 10.8% revenue surge, dramatically outpacing Walmart’s 4.7% growth.

The strategic implications are clear: the future of retail belongs not merely to those who sell the most, but to those who can master platform financialization to fund aggressive artificial intelligence (AI) and automation infrastructure.

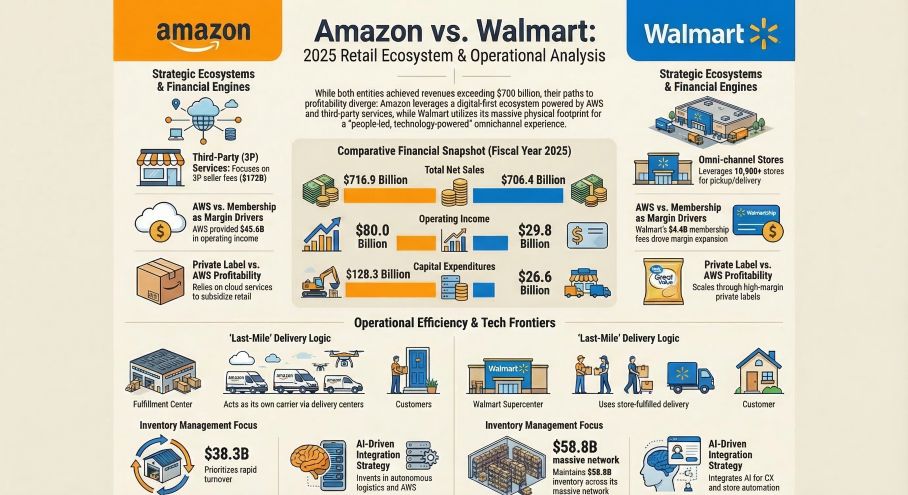

Figure Amazon vs. Walmart: 2025 Retail Ecosystem & Operational Analysis

Sector Positioning: Platform Financialization vs. Traditional Scale

Sector Positioning: Platform Financialization vs. Traditional Scale

The most striking divergence in our 2025 audit lies in supply chain bargaining power, quantified by the Days Payable Outstanding (DPO). Amazon operates with a staggering DPO of 110.8 days, creating a massive cash float. In contrast, Walmart’s DPO stands at 41.5 days.

The "So What" Factor: Amazon is not just delaying payments; it is executing a masterclass in capital allocation efficiency. By locking suppliers into its "1P + 3P + FBA" ecosystem, Amazon effectively utilizes over three months of zero-cost vendor financing to underwrite its colossal $128.3 billion capital expenditure (CapEx)—predominantly aimed at AI and AWS infrastructure—without triggering liquidity strain. Walmart’s supply chain, while highly optimized for Everyday Low Prices (EDLP), remains bound by traditional retail constraints and lacks this quasi-financial leverage.

Furthermore, Amazon’s pivot toward Third-Party (3P) seller services ($172.1 billion) fundamentally insulates its balance sheet. By shifting inventory depreciation risks to external sellers while extracting high-margin fulfillment fees and advertising revenue ($68.6 billion), Amazon’s retail operating margin has expanded to 5.84%, notably eclipsing Walmart’s 4.18%.

Strategic Pivots: Omnichannel Fulfillment and Capital Allocation

Both behemoths are deploying massive capital to combat cyclical headwinds, notably wage inflation and labor shortages, but their execution models represent a stark strategic dichotomy.

* Walmart’s "Store-as-a-Hub" Moat: Walmart is brilliantly leveraging its legacy physical assets. By utilizing over 8,400 global locations as distributed micro-fulfillment centers, Walmart secures the ultimate localized strategic moat. This proximity slashes last-mile delivery costs and accelerates grocery fulfillment. However, this transition is capital-intensive; Walmart’s $26.6 billion CapEx in FY2026 is heavily concentrated on supply chain automation, causing a temporary dip in its ROI to 15.1% as it navigates the friction of retrofitting legacy assets.

* Amazon’s Regionalized Network: Amazon has successfully decentralized its national fulfillment network into eight distinct regional nodes. This architectural overhaul directly reduces split-shipments and inter-regional transit costs. While its fulfillment costs reached $109 billion in 2025, the fulfillment-to-sales ratio actually contracted to 15.2%. This indicates that Amazon’s algorithmic inventory placement and robotic automation (e.g., Proteus) are generating genuine operational leverage, effectively neutralizing cyclical macroeconomic pressures.

Financial Health & Cyclical Headwinds

When stripping away surface-level earnings, a forensic look at profitability quality reveals hidden vulnerabilities and defensive accounting maneuvers.

For Walmart, its $21.89 billion net income was significantly padded by $2.07 billion in non-operating investment gains (primarily equity fair value fluctuations). Once adjusted for these non-recurring windfalls, Walmart’s core operating margins show slight compression due to rising self-insurance claims and labor costs. Its profitability remains deeply reliant on the highly predictable cash flow from its $4.4 billion membership fee revenue.

Conversely, Amazon exhibits extreme conservatism in its accounting estimates. In 2025, the company shortened the depreciation lifecycle of its servers from six years to five, absorbing a $1 billion hit to net income. HDIN Research views this not as a weakness, but as a strategic preemptive write-down. By recognizing the rapid obsolescence of AI hardware, Amazon is smoothing out future volatility and clearing the deck for next-generation technological dominance.

HDIN Viewpoint: The Ultimate Retail Trajectory

From an institutional perspective, HDIN Research concludes that Amazon has transcended traditional retail to become a high-margin infrastructure platform. Its ability to self-sustain retail operations through the dual engines of AWS and advertising cross-subsidization provides an unmatched threshold for absorbing strategic losses.

Walmart remains a formidable defensive play, anchored by its unparalleled grocery penetration and localized omnichannel integration. However, its exposure to traditional retail metrics—coupled with heavy reliance on non-operating gains and membership fees to shield its bottom line—leaves it more vulnerable to cyclical headwinds. Moving forward, the ultimate determinant of market valuation will be how effectively each firm navigates mounting antitrust scrutiny (such as Amazon’s recent $2.5 billion FTC settlement and Walmart's regulatory friction in Mexico and India) while translating AI CapEx into sustainable margin expansion.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

The strategic implications are clear: the future of retail belongs not merely to those who sell the most, but to those who can master platform financialization to fund aggressive artificial intelligence (AI) and automation infrastructure.

Figure Amazon vs. Walmart: 2025 Retail Ecosystem & Operational Analysis

Sector Positioning: Platform Financialization vs. Traditional ScaleThe most striking divergence in our 2025 audit lies in supply chain bargaining power, quantified by the Days Payable Outstanding (DPO). Amazon operates with a staggering DPO of 110.8 days, creating a massive cash float. In contrast, Walmart’s DPO stands at 41.5 days.

The "So What" Factor: Amazon is not just delaying payments; it is executing a masterclass in capital allocation efficiency. By locking suppliers into its "1P + 3P + FBA" ecosystem, Amazon effectively utilizes over three months of zero-cost vendor financing to underwrite its colossal $128.3 billion capital expenditure (CapEx)—predominantly aimed at AI and AWS infrastructure—without triggering liquidity strain. Walmart’s supply chain, while highly optimized for Everyday Low Prices (EDLP), remains bound by traditional retail constraints and lacks this quasi-financial leverage.

Furthermore, Amazon’s pivot toward Third-Party (3P) seller services ($172.1 billion) fundamentally insulates its balance sheet. By shifting inventory depreciation risks to external sellers while extracting high-margin fulfillment fees and advertising revenue ($68.6 billion), Amazon’s retail operating margin has expanded to 5.84%, notably eclipsing Walmart’s 4.18%.

Strategic Pivots: Omnichannel Fulfillment and Capital Allocation

Both behemoths are deploying massive capital to combat cyclical headwinds, notably wage inflation and labor shortages, but their execution models represent a stark strategic dichotomy.

* Walmart’s "Store-as-a-Hub" Moat: Walmart is brilliantly leveraging its legacy physical assets. By utilizing over 8,400 global locations as distributed micro-fulfillment centers, Walmart secures the ultimate localized strategic moat. This proximity slashes last-mile delivery costs and accelerates grocery fulfillment. However, this transition is capital-intensive; Walmart’s $26.6 billion CapEx in FY2026 is heavily concentrated on supply chain automation, causing a temporary dip in its ROI to 15.1% as it navigates the friction of retrofitting legacy assets.

* Amazon’s Regionalized Network: Amazon has successfully decentralized its national fulfillment network into eight distinct regional nodes. This architectural overhaul directly reduces split-shipments and inter-regional transit costs. While its fulfillment costs reached $109 billion in 2025, the fulfillment-to-sales ratio actually contracted to 15.2%. This indicates that Amazon’s algorithmic inventory placement and robotic automation (e.g., Proteus) are generating genuine operational leverage, effectively neutralizing cyclical macroeconomic pressures.

Financial Health & Cyclical Headwinds

When stripping away surface-level earnings, a forensic look at profitability quality reveals hidden vulnerabilities and defensive accounting maneuvers.

For Walmart, its $21.89 billion net income was significantly padded by $2.07 billion in non-operating investment gains (primarily equity fair value fluctuations). Once adjusted for these non-recurring windfalls, Walmart’s core operating margins show slight compression due to rising self-insurance claims and labor costs. Its profitability remains deeply reliant on the highly predictable cash flow from its $4.4 billion membership fee revenue.

Conversely, Amazon exhibits extreme conservatism in its accounting estimates. In 2025, the company shortened the depreciation lifecycle of its servers from six years to five, absorbing a $1 billion hit to net income. HDIN Research views this not as a weakness, but as a strategic preemptive write-down. By recognizing the rapid obsolescence of AI hardware, Amazon is smoothing out future volatility and clearing the deck for next-generation technological dominance.

HDIN Viewpoint: The Ultimate Retail Trajectory

From an institutional perspective, HDIN Research concludes that Amazon has transcended traditional retail to become a high-margin infrastructure platform. Its ability to self-sustain retail operations through the dual engines of AWS and advertising cross-subsidization provides an unmatched threshold for absorbing strategic losses.

Walmart remains a formidable defensive play, anchored by its unparalleled grocery penetration and localized omnichannel integration. However, its exposure to traditional retail metrics—coupled with heavy reliance on non-operating gains and membership fees to shield its bottom line—leaves it more vulnerable to cyclical headwinds. Moving forward, the ultimate determinant of market valuation will be how effectively each firm navigates mounting antitrust scrutiny (such as Amazon’s recent $2.5 billion FTC settlement and Walmart's regulatory friction in Mexico and India) while translating AI CapEx into sustainable margin expansion.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com