Specialty Vehicles 2025: Navigating EDA Transitions, Strategic Moats, and Cyclical Headwinds

Date : 2026-03-19

Reading : 138

The global specialty vehicle sector has officially exited the era of indiscriminate scale expansion, entering a highly bifurcated phase defined by structural prosperity and cyclical pressure. Based on an exhaustive fundamental analysis of six industry titans—Bucher Industries, Douglas Dynamics, Hyundai Everdigm, Miller Industries, Oshkosh, and REV Group—HDIN Research concludes that sector growth is now overwhelmingly driven by a "Technology Premium" and "Non-discretionary Demand."

As macroeconomic headwinds such as elevated interest rates and supply chain frictions persist, industry leaders are aggressively pivoting their capital allocation toward the "EDA" framework (Electrification, Digitalization, and Autonomy) while leveraging aftermarket ecosystems to defend margins.

Figure 2025 Comparative Landscape: Utility & Specialty Vehicle Peers

Sector Positioning: Capitalizing on Non-Discretionary Demand

Sector Positioning: Capitalizing on Non-Discretionary Demand

In 2025, the underlying demand logic for specialty vehicles has decoupled from standard commercial automotive cycles. Market resilience is anchored by three structural drivers:

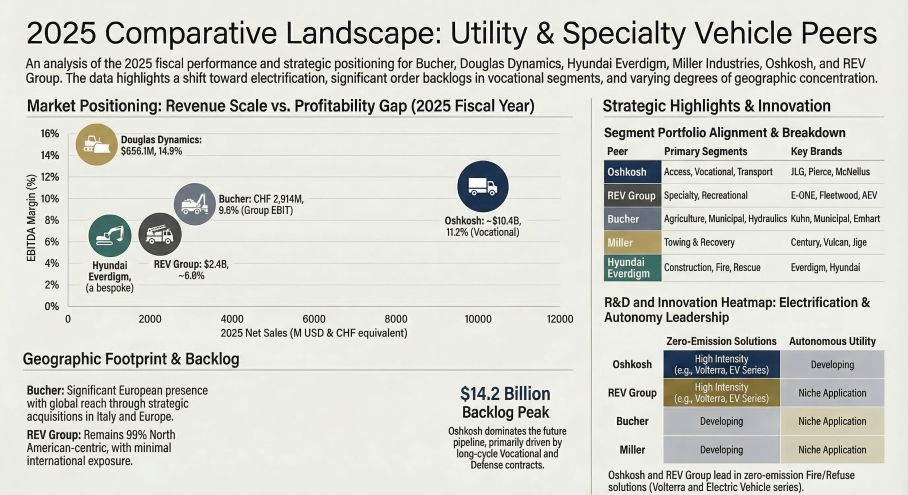

* The Rigid Nature of Municipal Spending: Fire apparatuses, ambulances, and snow-control equipment represent baseline societal continuity requirements. For instance, Douglas Dynamics and REV Group continue to benefit from municipal replacement cycles that cannot be indefinitely deferred, creating a highly visible revenue floor.

* Long-Cycle Infrastructure Updates: Rapid urbanization and megaprojects—such as Hyundai Everdigm’s $95 million deployment in the Middle East—provide long-term, counter-cyclical cash flows that offset localized construction slumps.

* Labor Shortage Catalysts: Chronic workforce deficits in agriculture, sanitation, and construction are forcing a shift from manual operation to vehicle automation, turning equipment upgrades from discretionary CapEx into operational necessities.

Strategic Moats: Vertical Integration vs. Authorized Conversion

The margin profiles across the sector reveal a stark divide based on supply chain mastery and vertical integration.

Companies that control the underlying chassis and proprietary components command superior pricing power. Oshkosh’s Vocational segment achieves an industry-leading 14.7% EBIT margin largely because its vertical integration (e.g., proprietary TAK-4 suspensions and custom fire truck chassis) captures value across the entire manufacturing chain, shielding it from third-party OEM delivery bottlenecks. Similarly, Miller Industries' strategic acquisition of hydraulic cylinder manufacturing insulates its heavy-duty rotator production from global component shortages.

Conversely, "Authorized Converters" relying heavily on third-party commercial chassis face distinct margin compression risks. Without proprietary chassis control, these players must execute rigorous, asset-light inventory management—such as REV Group’s "REV Drive" lean manufacturing system—to maintain operational efficiency and mitigate the lag in passing raw material costs to end-users.

Furthermore, aftermarket service density remains a virtually impenetrable moat. With REV Group’s massive 135,000-unit installed base (representing a $43 billion replacement value) and Douglas Dynamics’ expansive 3,000-location service network, these companies transform brand familiarity into recurring, high-margin parts revenue that stabilizes earnings during hardware sales dips.

Strategic Pivots: The "EDA" Capital Allocation Imperative

Capital expenditures across the top six manufacturers show a synchronized, aggressive pivot toward EDA technologies, transitioning companies from hardware assemblers to comprehensive fleet solution providers:

* Electrification: Commercial viability has arrived. Oshkosh is leading scale deployment with its Volterra™ platform and a massive multi-billion-dollar NGDV contract with the USPS. Concurrently, Bucher Municipal has captured the European zero-emission urban maintenance market with its fully electric CityCat sweepers.

* Digitalization: The monetization of fleet data is accelerating. Platforms like "Bucher Connect" provide predictive maintenance and data analytics, shifting the business model from transactional vehicle sales to recurring software-as-a-service (SaaS) revenue.

* Autonomy: To combat operator shortages, companies are embedding localized AI. From Douglas Dynamics’ precision AI-driven weed control to Oshkosh’s autonomous defense logistics platforms, automated assistance is driving significant technological price premiums.

Cyclical Headwinds: Tariffs, Rates, and Regulatory Friction

Despite robust strategic moats, the sector's expansion is capped by severe macro-environmental constraints.

* Tariff and Commodity Exposure: Geopolitical trade barriers are a dominant financial variable. Oshkosh has cautioned the market regarding a potential $200 million tariff-related cost burden by 2026. Forward-thinking procurement, such as Douglas Dynamics' aggressive steel hedging contracts, will be the primary differentiator in gross margin preservation.

* Cost of Capital Constraints: Prolonged high interest rates are severely straining distributor "floor plan" financing. This financial friction has temporarily dampened retail velocity for equipment like Miller Industries’ towing vehicles, forcing strategic production cuts to prevent channel channel inventory bloat.

* Regulatory Bottlenecks: Aggressive environmental mandates, particularly the California Air Resources Board (CARB) emission rules, are creating short-term hesitation. While these regulations ultimately favor EDA-compliant market leaders, they are currently causing order delays as fleet operators navigate compliance timelines.

HDIN Viewpoint: Navigating Capital Efficiency and Audit Risks

From an institutional advisory perspective, HDIN Research urges stakeholders to look beyond top-line backlog figures and rigorously audit the quality of operational cash flow.

We observe a clear divergence in capital allocation efficiency. Asset-light transitions, such as REV Group’s strategic divestitures and Douglas Dynamics’ sale-leaseback maneuvers, successfully convert fixed assets into variable costs, dramatically lowering breakeven points during demand lulls.

However, investors must exercise profound financial skepticism regarding short-term cash flow spikes. For instance, robust operating cash flow metrics may sometimes be the artifact of aggressive inventory liquidation rather than sustainable organic growth. Additionally, headline operating profits must be normalized to strip out non-recurring windfalls, such as real estate sales, to assess the true underlying margin health of the core manufacturing business. Moving forward into 2026, the true winners will be those who balance technology premiums with airtight, inflation-protected contract structures.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

As macroeconomic headwinds such as elevated interest rates and supply chain frictions persist, industry leaders are aggressively pivoting their capital allocation toward the "EDA" framework (Electrification, Digitalization, and Autonomy) while leveraging aftermarket ecosystems to defend margins.

Figure 2025 Comparative Landscape: Utility & Specialty Vehicle Peers

Sector Positioning: Capitalizing on Non-Discretionary DemandIn 2025, the underlying demand logic for specialty vehicles has decoupled from standard commercial automotive cycles. Market resilience is anchored by three structural drivers:

* The Rigid Nature of Municipal Spending: Fire apparatuses, ambulances, and snow-control equipment represent baseline societal continuity requirements. For instance, Douglas Dynamics and REV Group continue to benefit from municipal replacement cycles that cannot be indefinitely deferred, creating a highly visible revenue floor.

* Long-Cycle Infrastructure Updates: Rapid urbanization and megaprojects—such as Hyundai Everdigm’s $95 million deployment in the Middle East—provide long-term, counter-cyclical cash flows that offset localized construction slumps.

* Labor Shortage Catalysts: Chronic workforce deficits in agriculture, sanitation, and construction are forcing a shift from manual operation to vehicle automation, turning equipment upgrades from discretionary CapEx into operational necessities.

Strategic Moats: Vertical Integration vs. Authorized Conversion

The margin profiles across the sector reveal a stark divide based on supply chain mastery and vertical integration.

Companies that control the underlying chassis and proprietary components command superior pricing power. Oshkosh’s Vocational segment achieves an industry-leading 14.7% EBIT margin largely because its vertical integration (e.g., proprietary TAK-4 suspensions and custom fire truck chassis) captures value across the entire manufacturing chain, shielding it from third-party OEM delivery bottlenecks. Similarly, Miller Industries' strategic acquisition of hydraulic cylinder manufacturing insulates its heavy-duty rotator production from global component shortages.

Conversely, "Authorized Converters" relying heavily on third-party commercial chassis face distinct margin compression risks. Without proprietary chassis control, these players must execute rigorous, asset-light inventory management—such as REV Group’s "REV Drive" lean manufacturing system—to maintain operational efficiency and mitigate the lag in passing raw material costs to end-users.

Furthermore, aftermarket service density remains a virtually impenetrable moat. With REV Group’s massive 135,000-unit installed base (representing a $43 billion replacement value) and Douglas Dynamics’ expansive 3,000-location service network, these companies transform brand familiarity into recurring, high-margin parts revenue that stabilizes earnings during hardware sales dips.

Strategic Pivots: The "EDA" Capital Allocation Imperative

Capital expenditures across the top six manufacturers show a synchronized, aggressive pivot toward EDA technologies, transitioning companies from hardware assemblers to comprehensive fleet solution providers:

* Electrification: Commercial viability has arrived. Oshkosh is leading scale deployment with its Volterra™ platform and a massive multi-billion-dollar NGDV contract with the USPS. Concurrently, Bucher Municipal has captured the European zero-emission urban maintenance market with its fully electric CityCat sweepers.

* Digitalization: The monetization of fleet data is accelerating. Platforms like "Bucher Connect" provide predictive maintenance and data analytics, shifting the business model from transactional vehicle sales to recurring software-as-a-service (SaaS) revenue.

* Autonomy: To combat operator shortages, companies are embedding localized AI. From Douglas Dynamics’ precision AI-driven weed control to Oshkosh’s autonomous defense logistics platforms, automated assistance is driving significant technological price premiums.

Cyclical Headwinds: Tariffs, Rates, and Regulatory Friction

Despite robust strategic moats, the sector's expansion is capped by severe macro-environmental constraints.

* Tariff and Commodity Exposure: Geopolitical trade barriers are a dominant financial variable. Oshkosh has cautioned the market regarding a potential $200 million tariff-related cost burden by 2026. Forward-thinking procurement, such as Douglas Dynamics' aggressive steel hedging contracts, will be the primary differentiator in gross margin preservation.

* Cost of Capital Constraints: Prolonged high interest rates are severely straining distributor "floor plan" financing. This financial friction has temporarily dampened retail velocity for equipment like Miller Industries’ towing vehicles, forcing strategic production cuts to prevent channel channel inventory bloat.

* Regulatory Bottlenecks: Aggressive environmental mandates, particularly the California Air Resources Board (CARB) emission rules, are creating short-term hesitation. While these regulations ultimately favor EDA-compliant market leaders, they are currently causing order delays as fleet operators navigate compliance timelines.

HDIN Viewpoint: Navigating Capital Efficiency and Audit Risks

From an institutional advisory perspective, HDIN Research urges stakeholders to look beyond top-line backlog figures and rigorously audit the quality of operational cash flow.

We observe a clear divergence in capital allocation efficiency. Asset-light transitions, such as REV Group’s strategic divestitures and Douglas Dynamics’ sale-leaseback maneuvers, successfully convert fixed assets into variable costs, dramatically lowering breakeven points during demand lulls.

However, investors must exercise profound financial skepticism regarding short-term cash flow spikes. For instance, robust operating cash flow metrics may sometimes be the artifact of aggressive inventory liquidation rather than sustainable organic growth. Additionally, headline operating profits must be normalized to strip out non-recurring windfalls, such as real estate sales, to assess the true underlying margin health of the core manufacturing business. Moving forward into 2026, the true winners will be those who balance technology premiums with airtight, inflation-protected contract structures.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com