Owlet 2025 Annual Report Analysis: Navigating the Digital Healthcare Pivot and Securing FDA Moats

Date : 2026-03-21

Reading : 82

In 2025, Owlet, Inc. (NYSE: OWLT) executed a definitive structural shift, transitioning from a traditional consumer electronics manufacturer into a globally recognized, FDA-cleared digital pediatric healthcare platform. Rather than merely shipping standalone hardware, Owlet has successfully operationalized a closed-loop ecosystem. Driven by aggressive product mix optimization and the rapid scaling of its high-margin subscription services, the company not only achieved a 35.4% revenue surge but also recorded its first-ever full-year positive Adjusted EBITDA.

Figure Owlet 2025: The Year of Strategic Inflection

Strategic Pivots: Transitioning to a High-Margin SaaS Healthcare Platform

Strategic Pivots: Transitioning to a High-Margin SaaS Healthcare Platform

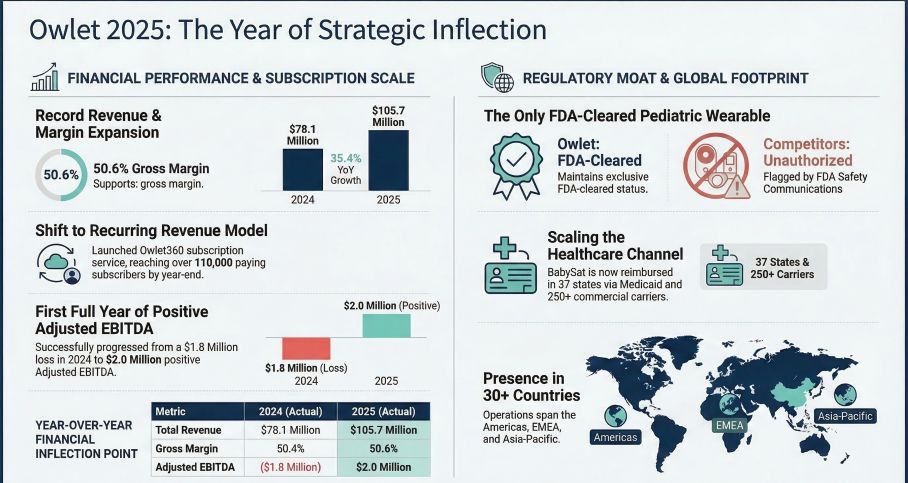

The most critical catalyst in Owlet’s 2025 performance was its strategic pivot from a one-off hardware sales model to a high-retention Software-as-a-Service (SaaS) framework. The launch of the Owlet360 subscription service ($9.99/month) fundamentally rearchitected the company’s unit economics.

Closing the year with over 110,000 paid subscribers, this SaaS overlay provides highly predictable recurring revenue that effectively cushions the cyclical volatility inherent in hardware manufacturing. More importantly, it exponentially expands Customer Lifetime Value (LTV). While traditional infant monitors capture value only at the point of sale, Owlet’s AI-driven health insights extend the monetization window across the infant's 27-month developmental cycle, systematically lowering Customer Acquisition Cost (CAC) through enhanced ecosystem stickiness.

Sector Positioning: FDA Clearance as a Strategic Moat

Owlet’s sector positioning is anchored by an unparalleled regulatory moat. The company remains the sole player in the over-the-counter (OTC) infant monitoring market to secure FDA *De Novo* marketing authorization for its Dream Sock. This unique classification creates formidable barriers to entry for competitors like Nanit or Cubo AI, forcing them to navigate stringent and costly compliance pathways.

Furthermore, the introduction of the prescription-grade BabySat monitor has unlocked deep institutional channels. By penetrating the reimbursement infrastructure—securing Medicaid coverage across 37 states and partnerships with over 250 commercial insurance providers—Owlet is successfully transforming consumer discretionary spending into non-cyclical healthcare expenditure.

Financial Health & Capital Allocation Efficiency

Operational efficiency and market expansion drove a 35.4% revenue surge to $105.7 million in FY2025. Capital allocation efficiency is clearly reflected in the gross margin expansion to an all-time high of 50.6%. This margin premium was largely generated by the low marginal costs of the Owlet360 software revenue and the enhanced fixed-cost absorption of scaled manufacturing.

Consequently, operating losses narrowed by an impressive 58.9% to $8.3 million. While the GAAP net loss stood at $39.7 million, this figure was heavily skewed by a $26.6 million non-cash warrant liability adjustment. Stripping away these non-operational derivatives, the company achieved a milestone positive Adjusted EBITDA of $2.0 million, signaling that its core commercial engine is now financially self-sustaining.

Cyclical Headwinds & Supply Chain Reallocation

Despite robust top-line growth, Owlet faces severe cyclical headwinds stemming from geopolitical trade fragmentation. Throughout late 2025, the company’s asset-light manufacturing partners in Thailand and Vietnam were hit with reciprocal tariffs ranging from 19% to 20%, later stabilizing as a 10% ad valorem surcharge.

To defend operating margins, management is executing a strategic supply chain reallocation. By establishing a new manufacturing footprint in Mexico slated for 2026, Owlet aims to leverage medical device tariff exemptions. If executed seamlessly, this nearshoring strategy will engineer a structural cost advantage, though the short-term transition will require rigorous oversight of capital expenditures and operational friction.

HDIN Viewpoint: The Balancing Act of Digital Health Transformation

From an institutional perspective, HDIN Research views Owlet at a critical inflection point where its massive proprietary pediatric dataset is finally yielding tangible financial leverage. The transition toward AI-driven predictive health analytics cements a durable competitive advantage that is difficult for pure-play hardware competitors to replicate.

However, a prudent valuation must account for structural vulnerabilities. The company candidly reported material weaknesses in its internal controls regarding financial reporting, which introduces a layer of governance risk until fully remediated. Additionally, with 66.5% of revenue concentrated among top retail partners, downstream inventory corrections remain a persistent threat. Ultimately, 2026 will be the definitive test of management’s execution capabilities as they attempt to scale their high-margin SaaS model globally while successfully navigating the complex relocation of their manufacturing base.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Owlet 2025: The Year of Strategic Inflection

Strategic Pivots: Transitioning to a High-Margin SaaS Healthcare PlatformThe most critical catalyst in Owlet’s 2025 performance was its strategic pivot from a one-off hardware sales model to a high-retention Software-as-a-Service (SaaS) framework. The launch of the Owlet360 subscription service ($9.99/month) fundamentally rearchitected the company’s unit economics.

Closing the year with over 110,000 paid subscribers, this SaaS overlay provides highly predictable recurring revenue that effectively cushions the cyclical volatility inherent in hardware manufacturing. More importantly, it exponentially expands Customer Lifetime Value (LTV). While traditional infant monitors capture value only at the point of sale, Owlet’s AI-driven health insights extend the monetization window across the infant's 27-month developmental cycle, systematically lowering Customer Acquisition Cost (CAC) through enhanced ecosystem stickiness.

Sector Positioning: FDA Clearance as a Strategic Moat

Owlet’s sector positioning is anchored by an unparalleled regulatory moat. The company remains the sole player in the over-the-counter (OTC) infant monitoring market to secure FDA *De Novo* marketing authorization for its Dream Sock. This unique classification creates formidable barriers to entry for competitors like Nanit or Cubo AI, forcing them to navigate stringent and costly compliance pathways.

Furthermore, the introduction of the prescription-grade BabySat monitor has unlocked deep institutional channels. By penetrating the reimbursement infrastructure—securing Medicaid coverage across 37 states and partnerships with over 250 commercial insurance providers—Owlet is successfully transforming consumer discretionary spending into non-cyclical healthcare expenditure.

Financial Health & Capital Allocation Efficiency

Operational efficiency and market expansion drove a 35.4% revenue surge to $105.7 million in FY2025. Capital allocation efficiency is clearly reflected in the gross margin expansion to an all-time high of 50.6%. This margin premium was largely generated by the low marginal costs of the Owlet360 software revenue and the enhanced fixed-cost absorption of scaled manufacturing.

Consequently, operating losses narrowed by an impressive 58.9% to $8.3 million. While the GAAP net loss stood at $39.7 million, this figure was heavily skewed by a $26.6 million non-cash warrant liability adjustment. Stripping away these non-operational derivatives, the company achieved a milestone positive Adjusted EBITDA of $2.0 million, signaling that its core commercial engine is now financially self-sustaining.

Cyclical Headwinds & Supply Chain Reallocation

Despite robust top-line growth, Owlet faces severe cyclical headwinds stemming from geopolitical trade fragmentation. Throughout late 2025, the company’s asset-light manufacturing partners in Thailand and Vietnam were hit with reciprocal tariffs ranging from 19% to 20%, later stabilizing as a 10% ad valorem surcharge.

To defend operating margins, management is executing a strategic supply chain reallocation. By establishing a new manufacturing footprint in Mexico slated for 2026, Owlet aims to leverage medical device tariff exemptions. If executed seamlessly, this nearshoring strategy will engineer a structural cost advantage, though the short-term transition will require rigorous oversight of capital expenditures and operational friction.

HDIN Viewpoint: The Balancing Act of Digital Health Transformation

From an institutional perspective, HDIN Research views Owlet at a critical inflection point where its massive proprietary pediatric dataset is finally yielding tangible financial leverage. The transition toward AI-driven predictive health analytics cements a durable competitive advantage that is difficult for pure-play hardware competitors to replicate.

However, a prudent valuation must account for structural vulnerabilities. The company candidly reported material weaknesses in its internal controls regarding financial reporting, which introduces a layer of governance risk until fully remediated. Additionally, with 66.5% of revenue concentrated among top retail partners, downstream inventory corrections remain a persistent threat. Ultimately, 2026 will be the definitive test of management’s execution capabilities as they attempt to scale their high-margin SaaS model globally while successfully navigating the complex relocation of their manufacturing base.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com