Otis vs KONE 2025: Navigating the Elevator Sector's Paradigm Shift

Date : 2026-03-18

Reading : 1077

The global elevator industry is undergoing a structural paradigm shift, transitioning from a volume-driven new equipment market to a highly lucrative, installed-base governance model. According to the latest 2025 financial analysis by HDIN Research, industry titans Otis and KONE are deploying divergent strategies to navigate cyclical headwinds. While Otis leverages aggressive operational efficiency and capital allocation to drive profitability, KONE exhibits unparalleled earnings quality and asset-light resilience, positioning modernization as its ultimate counter-cyclical growth engine.

Figure Clash of the Titans: Otis vs KONE 2025 Performance Review

Sector Positioning: The Shift from Hardware to Lifecycle Services

Sector Positioning: The Shift from Hardware to Lifecycle Services

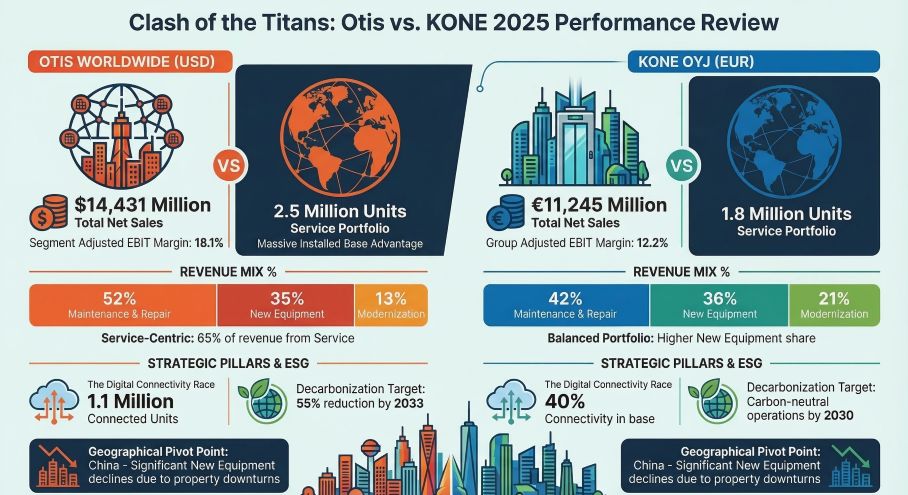

Both Otis and KONE are facing severe cyclical headwinds in the new equipment sector, primarily driven by the deep contraction in the Chinese real estate market, where Otis and KONE saw organic new equipment sales decline by over 20% and 11.1%, respectively.

So, what is the strategic implication? The core profit engine of the elevator sector is no longer manufacturing; it is the "lock-in effect" of the equipment's lifecycle. Both companies have successfully pivoted their sector positioning to rely on their massive installed bases—approximately 2.5 million units for Otis and 1.8 million for KONE. For Otis, high-margin service and modernization revenues now contribute a staggering 91% of its operating profit, effectively transforming the industrial giant into a recurring-revenue service ecosystem. Simultaneously, KONE has utilized its aging global footprint to drive a 17.4% surge in its modernization business, utilizing sustainability upgrades to offset new construction slumps.

Capital Allocation Efficiency: Aggressive Returns vs. Cash Cow Stability

A deep dive into the 2025 financials reveals stark contrasts in capital allocation efficiency and balance sheet philosophy.

* KONE’s Asset-Light "Cash Machine": KONE operates on a negative working capital model driven by highly efficient prepayments. This structural advantage translates to an exceptional Operating Cash Flow to Net Income (OCF/NI) conversion rate of 1.77x. Operating with a net cash position of roughly $791 million, KONE is shielded from high-interest-rate environments, allowing for a robust 95.1% dividend payout ratio while maintaining the agility for strategic M&A in Europe.

* Otis’s Leveraged Efficiency: In contrast, Otis exhibits classic aggressive capital distribution. Despite carrying substantial debt, Otis consistently utilizes stock buybacks and dividends to drive EPS growth. Furthermore, Otis's "UpLift" restructuring program has successfully optimized its SG&A expenses, resulting in an industry-leading operating margin (EBIT) of 14.8% (compared to KONE’s 11.9%).

Strategic Moats: Digital Connectivity vs. R&D Intensity

To defend their high-margin service portfolios from independent service providers (ISPs) engaging in price arbitrage, both giants are rapidly digitizing their strategic moats.

KONE heavily outpaces Otis in R&D intensity (2.1% of revenue vs. 1.1%), focusing on "People Flow" intelligence and carbon-neutral hardware. By achieving a 40% digital connection rate across its service base, KONE is building a technological fortress around its premium modernization contracts.

Conversely, Otis focuses its innovation on service-margin expansion. Through the "Otis ONE" IoT platform, the company has connected 1.1 million units globally. This predictive maintenance infrastructure drastically reduces unexpected downtimes and optimizes labor allocation, directly funneling efficiency gains into shareholder value.

HDIN Viewpoint

From an institutional perspective, HDIN Research views the Otis and KONE 2025 financial results as a masterclass in strategic divergence under macroeconomic stress. Otis offers superior nominal profitability and aggressive value extraction for shareholders, making it an attractive play for those prioritizing service-margin expansion and capital leverage. However, from an earnings quality and risk-mitigation standpoint, KONE emerges as the more resilient "cash cow." Its debt-free balance sheet, superior cash conversion cycle, and European market depth offer substantial downside protection against prolonged cyclical headwinds in Asia.

Looking ahead to 2026, the critical metric for investors will not be new elevator shipments, but rather the retention rate of service contracts and the ability of digital predictive maintenance to offset wage inflation and local ISP pricing pressures.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Clash of the Titans: Otis vs KONE 2025 Performance Review

Sector Positioning: The Shift from Hardware to Lifecycle ServicesBoth Otis and KONE are facing severe cyclical headwinds in the new equipment sector, primarily driven by the deep contraction in the Chinese real estate market, where Otis and KONE saw organic new equipment sales decline by over 20% and 11.1%, respectively.

So, what is the strategic implication? The core profit engine of the elevator sector is no longer manufacturing; it is the "lock-in effect" of the equipment's lifecycle. Both companies have successfully pivoted their sector positioning to rely on their massive installed bases—approximately 2.5 million units for Otis and 1.8 million for KONE. For Otis, high-margin service and modernization revenues now contribute a staggering 91% of its operating profit, effectively transforming the industrial giant into a recurring-revenue service ecosystem. Simultaneously, KONE has utilized its aging global footprint to drive a 17.4% surge in its modernization business, utilizing sustainability upgrades to offset new construction slumps.

Capital Allocation Efficiency: Aggressive Returns vs. Cash Cow Stability

A deep dive into the 2025 financials reveals stark contrasts in capital allocation efficiency and balance sheet philosophy.

* KONE’s Asset-Light "Cash Machine": KONE operates on a negative working capital model driven by highly efficient prepayments. This structural advantage translates to an exceptional Operating Cash Flow to Net Income (OCF/NI) conversion rate of 1.77x. Operating with a net cash position of roughly $791 million, KONE is shielded from high-interest-rate environments, allowing for a robust 95.1% dividend payout ratio while maintaining the agility for strategic M&A in Europe.

* Otis’s Leveraged Efficiency: In contrast, Otis exhibits classic aggressive capital distribution. Despite carrying substantial debt, Otis consistently utilizes stock buybacks and dividends to drive EPS growth. Furthermore, Otis's "UpLift" restructuring program has successfully optimized its SG&A expenses, resulting in an industry-leading operating margin (EBIT) of 14.8% (compared to KONE’s 11.9%).

Strategic Moats: Digital Connectivity vs. R&D Intensity

To defend their high-margin service portfolios from independent service providers (ISPs) engaging in price arbitrage, both giants are rapidly digitizing their strategic moats.

KONE heavily outpaces Otis in R&D intensity (2.1% of revenue vs. 1.1%), focusing on "People Flow" intelligence and carbon-neutral hardware. By achieving a 40% digital connection rate across its service base, KONE is building a technological fortress around its premium modernization contracts.

Conversely, Otis focuses its innovation on service-margin expansion. Through the "Otis ONE" IoT platform, the company has connected 1.1 million units globally. This predictive maintenance infrastructure drastically reduces unexpected downtimes and optimizes labor allocation, directly funneling efficiency gains into shareholder value.

HDIN Viewpoint

From an institutional perspective, HDIN Research views the Otis and KONE 2025 financial results as a masterclass in strategic divergence under macroeconomic stress. Otis offers superior nominal profitability and aggressive value extraction for shareholders, making it an attractive play for those prioritizing service-margin expansion and capital leverage. However, from an earnings quality and risk-mitigation standpoint, KONE emerges as the more resilient "cash cow." Its debt-free balance sheet, superior cash conversion cycle, and European market depth offer substantial downside protection against prolonged cyclical headwinds in Asia.

Looking ahead to 2026, the critical metric for investors will not be new elevator shipments, but rather the retention rate of service contracts and the ability of digital predictive maintenance to offset wage inflation and local ISP pricing pressures.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com