Beyond the Screen: A Comparative Deep-Dive into Netflix and iQIYI’s FY2025 Profit Quality and Strategic Moats

Date : 2026-03-18

Reading : 168

The global streaming industry has decisively entered a mature phase of inventory-driven competition in FY2025, shifting its strategic imperative from user acquisition to Average Revenue Per User (ARPU) expansion and operational efficiency. Based on an exhaustive comparative audit by HDIN Research, the financial realities of industry leaders Netflix (NFLX) and iQIYI (IQ) reveal a stark dichotomy. While Netflix has cemented its status as a self-sustaining cash compounder driven by global scale, iQIYI is navigating severe liquidity headwinds, forcing a radical strategic pivot toward offline IP monetization to survive cyclical headwinds.

Figure Operational DNA: Netflix vs iQlYl (2025 Performance Analysis)

Financial Health and Capital Allocation Efficiency

Financial Health and Capital Allocation Efficiency

In institutional financial analysis, the alignment between Operating Cash Flow (OCF) and Net Income is the ultimate litmus test for earnings quality. Our analysis uncovers a fundamental divergence in capital allocation efficiency between the two giants.

Netflix has achieved a highly robust profitability loop. In FY2025, the company reported a net income of $10.98 billion alongside an operating cash flow of $10.15 billion. This exceptional 0.92 OCF-to-Net Income ratio indicates that Netflix has entirely transcended the industry's traditional "cash-burn" phase. Furthermore, its debt structure is heavily insulated, driven by long-term notes with maturities extending to 2054, yielding a highly secure interest coverage ratio of over 17x.

Conversely, iQIYI’s balance sheet reflects fragile accounting equilibrium masking profound liquidity constraints. Reverting to a net loss in 2025, iQIYI’s operational cash flow is a mere fraction (0.14%) of Netflix’s. More alarmingly, iQIYI faces an imminent working capital deficit of approximately $1.64 billion (RMB 11.8 billion). With an interest coverage ratio plummeting to 0.25x, the company's operating profits are insufficient to service its debt obligations, leaving it heavily reliant on continuous refinancing and related-party life rafts to sustain operations.

The "Red Flags" of Content Amortization

Content amortization policies serve as the primary lever for streaming platforms to massage bottom-line optics. When amortization outpaces the actual depreciation of content value, it risks artificially inflating asset values and obscuring underlying losses.

Netflix employs a highly prudent, accelerated amortization model, expensing over 90% of its content assets within four years of premiere. This aligns perfectly with the rapid decay curve characteristic of internet media consumption.

iQIYI, however, exposes investors to significant accounting estimation risks. While claiming an accelerated approach, iQIYI caps its amortization horizon at the shorter of the contract term, estimated useful life, or *10 years*. In the hyper-fast Chinese content market, a 10-year horizon creates immense discretionary leeway for management. Should iQIYI artificially lower amortization rates to pad its struggling 2025 income statement, it would result in deeply overstated content assets—a critical vulnerability for investors to monitor.

Organizational Efficiency and Sector Positioning

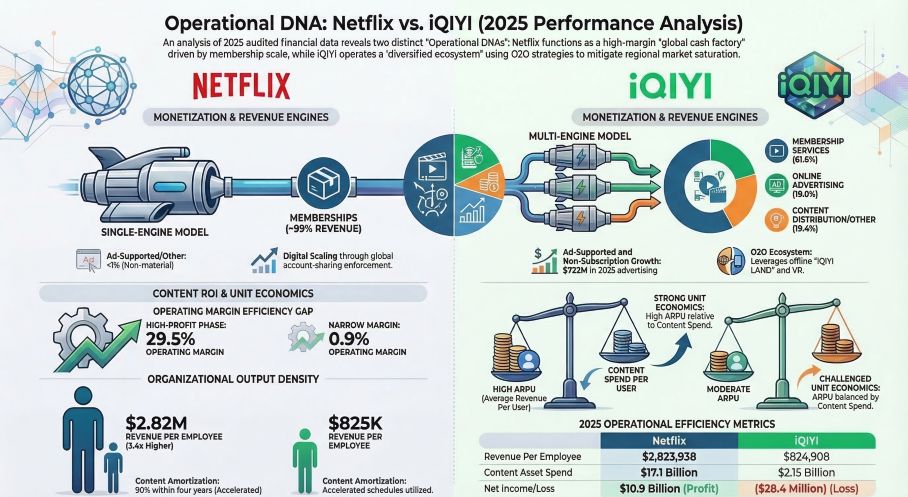

The underlying architecture of these two companies dictates their stark contrast in marginal cost control. Netflix operates a "Single Operating Segment," allowing it to amortize fixed content costs across a massive, borderless 190-country subscriber base. This single-point global penetration yields an extraordinary revenue per employee of approximately $2.82 million.

In contrast, iQIYI generates roughly $825,000 per employee (nearly 3.4x lower than Netflix). This disparity stems from iQIYI’s complex, multi-layered business matrix. To combat slowing online subscriptions, iQIYI has transformed into an O2O (Online-to-Offline) ecosystem. By deploying capital into VR immersive theaters and the newly launched "iQIYI LAND," the company is utilizing offline touchpoints as a defensive moat to expand the Lifetime Value (LTV) of its IP, mitigating the volatility of the digital advertising market.

Strategic Pivots: AI Integration and the Ad-Tier Imperative

To break through revenue ceilings, both platforms are aggressively standardizing Artificial Intelligence (AI) and Performance Advertising into their core infrastructures.

AI expenditure has transitioned from experimental R&D to foundational infrastructure. Netflix utilizes Generative AI to optimize content discovery and user retention algorithms, a non-negotiable asset for maintaining its pricing power. iQIYI has deeply integrated AI across its production lifecycle, deploying "Screenplay Studio" to predict breakout hits and introducing "Taodou," an AI-driven conversational assistant designed to deepen user immersion.

Simultaneously, the Ad-supported tier has become the universal mechanism for ARPU growth. Netflix utilizes ad-tiers to capture price-sensitive demographics in saturated markets, while iQIYI leverages algorithm-optimized performance advertising to extract value from its existing user base.

Cyclical Headwinds and Global Expansion

Macro-economic pressures and regulatory tightening remain the primary structural ceilings for the sector. Netflix's growth engine is currently fueled by its Asia-Pacific (APAC) segment, which surged 21% in 2025, largely driven by the aggressive enforcement of its household password-sharing crackdown in low-penetration markets. However, its global expansion is not without friction; unexpected non-income tax audits, such as a massive $619 million hit in Brazil, highlight the unpredictable fiscal traps of international operations.

iQIYI faces strict domestic regulatory environments regarding content and format formats (like micro-dramas). While expanding its Global App to export C-pop content, its overseas monetization remains shallow, lacking the deep advertising and offline integrations that sustain its domestic operations.

HDIN Viewpoint

The streaming wars have morphed from a battle for eyeballs into a war of balance sheets and capital efficiency. HDIN Research views Netflix as a highly mature, utility-like asset with an unparalleled global moat. However, investors must remain vigilant regarding the extreme leverage risks associated with its aggressive M&A pipeline, specifically its staggering $42.2 billion bridge facility for the WBD acquisition.

iQIYI, conversely, is executing a high-stakes ecosystem pivot. Its survival is strictly tethered to navigating its immediate liquidity gap. If management can successfully utilize offline assets like iQIYI LAND to translate digital traffic into tangible consumer spending, it could forge a unique, highly defensible business model distinct from Western counterparts. However, until the debt structure is stabilized, investors must heavily discount surface-level profitability and scrutinize its prolonged content amortization schedules.

Presentation Download & Media Access

To dive deeper into the financial models, risk assessments, and raw data behind this analysis:

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video. *(Link placeholder)*

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. Our rigorous methodologies ensure actionable intelligence for institutional investors and corporate strategists navigating complex global markets.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Operational DNA: Netflix vs iQlYl (2025 Performance Analysis)

Financial Health and Capital Allocation EfficiencyIn institutional financial analysis, the alignment between Operating Cash Flow (OCF) and Net Income is the ultimate litmus test for earnings quality. Our analysis uncovers a fundamental divergence in capital allocation efficiency between the two giants.

Netflix has achieved a highly robust profitability loop. In FY2025, the company reported a net income of $10.98 billion alongside an operating cash flow of $10.15 billion. This exceptional 0.92 OCF-to-Net Income ratio indicates that Netflix has entirely transcended the industry's traditional "cash-burn" phase. Furthermore, its debt structure is heavily insulated, driven by long-term notes with maturities extending to 2054, yielding a highly secure interest coverage ratio of over 17x.

Conversely, iQIYI’s balance sheet reflects fragile accounting equilibrium masking profound liquidity constraints. Reverting to a net loss in 2025, iQIYI’s operational cash flow is a mere fraction (0.14%) of Netflix’s. More alarmingly, iQIYI faces an imminent working capital deficit of approximately $1.64 billion (RMB 11.8 billion). With an interest coverage ratio plummeting to 0.25x, the company's operating profits are insufficient to service its debt obligations, leaving it heavily reliant on continuous refinancing and related-party life rafts to sustain operations.

The "Red Flags" of Content Amortization

Content amortization policies serve as the primary lever for streaming platforms to massage bottom-line optics. When amortization outpaces the actual depreciation of content value, it risks artificially inflating asset values and obscuring underlying losses.

Netflix employs a highly prudent, accelerated amortization model, expensing over 90% of its content assets within four years of premiere. This aligns perfectly with the rapid decay curve characteristic of internet media consumption.

iQIYI, however, exposes investors to significant accounting estimation risks. While claiming an accelerated approach, iQIYI caps its amortization horizon at the shorter of the contract term, estimated useful life, or *10 years*. In the hyper-fast Chinese content market, a 10-year horizon creates immense discretionary leeway for management. Should iQIYI artificially lower amortization rates to pad its struggling 2025 income statement, it would result in deeply overstated content assets—a critical vulnerability for investors to monitor.

Organizational Efficiency and Sector Positioning

The underlying architecture of these two companies dictates their stark contrast in marginal cost control. Netflix operates a "Single Operating Segment," allowing it to amortize fixed content costs across a massive, borderless 190-country subscriber base. This single-point global penetration yields an extraordinary revenue per employee of approximately $2.82 million.

In contrast, iQIYI generates roughly $825,000 per employee (nearly 3.4x lower than Netflix). This disparity stems from iQIYI’s complex, multi-layered business matrix. To combat slowing online subscriptions, iQIYI has transformed into an O2O (Online-to-Offline) ecosystem. By deploying capital into VR immersive theaters and the newly launched "iQIYI LAND," the company is utilizing offline touchpoints as a defensive moat to expand the Lifetime Value (LTV) of its IP, mitigating the volatility of the digital advertising market.

Strategic Pivots: AI Integration and the Ad-Tier Imperative

To break through revenue ceilings, both platforms are aggressively standardizing Artificial Intelligence (AI) and Performance Advertising into their core infrastructures.

AI expenditure has transitioned from experimental R&D to foundational infrastructure. Netflix utilizes Generative AI to optimize content discovery and user retention algorithms, a non-negotiable asset for maintaining its pricing power. iQIYI has deeply integrated AI across its production lifecycle, deploying "Screenplay Studio" to predict breakout hits and introducing "Taodou," an AI-driven conversational assistant designed to deepen user immersion.

Simultaneously, the Ad-supported tier has become the universal mechanism for ARPU growth. Netflix utilizes ad-tiers to capture price-sensitive demographics in saturated markets, while iQIYI leverages algorithm-optimized performance advertising to extract value from its existing user base.

Cyclical Headwinds and Global Expansion

Macro-economic pressures and regulatory tightening remain the primary structural ceilings for the sector. Netflix's growth engine is currently fueled by its Asia-Pacific (APAC) segment, which surged 21% in 2025, largely driven by the aggressive enforcement of its household password-sharing crackdown in low-penetration markets. However, its global expansion is not without friction; unexpected non-income tax audits, such as a massive $619 million hit in Brazil, highlight the unpredictable fiscal traps of international operations.

iQIYI faces strict domestic regulatory environments regarding content and format formats (like micro-dramas). While expanding its Global App to export C-pop content, its overseas monetization remains shallow, lacking the deep advertising and offline integrations that sustain its domestic operations.

HDIN Viewpoint

The streaming wars have morphed from a battle for eyeballs into a war of balance sheets and capital efficiency. HDIN Research views Netflix as a highly mature, utility-like asset with an unparalleled global moat. However, investors must remain vigilant regarding the extreme leverage risks associated with its aggressive M&A pipeline, specifically its staggering $42.2 billion bridge facility for the WBD acquisition.

iQIYI, conversely, is executing a high-stakes ecosystem pivot. Its survival is strictly tethered to navigating its immediate liquidity gap. If management can successfully utilize offline assets like iQIYI LAND to translate digital traffic into tangible consumer spending, it could forge a unique, highly defensible business model distinct from Western counterparts. However, until the debt structure is stabilized, investors must heavily discount surface-level profitability and scrutinize its prolonged content amortization schedules.

Presentation Download & Media Access

To dive deeper into the financial models, risk assessments, and raw data behind this analysis:

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video. *(Link placeholder)*

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. Our rigorous methodologies ensure actionable intelligence for institutional investors and corporate strategists navigating complex global markets.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com