Liquidmetal Technologies (LQMT) 2025 Annual Review: Navigating the Transition from Asset-Light IP to Heavy Manufacturing

Date : 2026-03-20

Reading : 101

Liquidmetal Technologies, Inc. (LQMT) is currently navigating a critical inflection point characterized by a stark contradiction: a robust liquidity buffer masking a severe deterioration in core operational cash generation. According to the latest proprietary analysis by HDIN Research, the company’s FY2025 results reveal a fundamental strategic pivot. Facing shrinking revenues and extreme customer concentration, LQMT is aggressively transitioning from an asset-light, technology-licensing model toward an asset-heavy, cross-border manufacturing joint venture in China. This move represents a make-or-break capitalization strategy to commercialize its amorphous alloy technology in non-consumer markets.

Figure Liquidmetal Technologies(LQMT) 2025 Strategic Pivot: From Patent Holder to Global Manufacturer

Capital Allocation Efficiency: High Liquidity Masks Operational Deficits

Capital Allocation Efficiency: High Liquidity Masks Operational Deficits

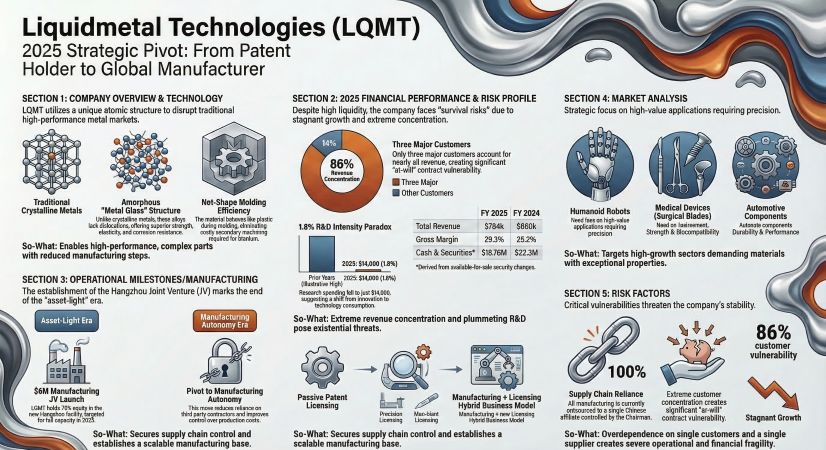

A deeper dive into LQMT’s financial health reveals structural profitability challenges. FY2025 total revenue contracted by 8.8% year-over-year to a mere $784,000, primarily driven by cyclical headwinds and reduced shipments in health-monitoring rings and medical device components.

While gross margins saw a marginal improvement to 29.3% (up from 25.2% in 2024), the absolute gross profit of $230,000 is vastly insufficient to sustain the company's corporate overhead. Consequently, the company posted a staggering operating loss of $3.74 million, translating to an operating margin of -477.3%. Essentially, for every dollar generated, LQMT spends nearly $4.77 in operational costs.

Despite this operational cash bleed, LQMT maintains a remarkably high financial safety margin. With a current ratio of 8.85 and holding approximately $19.76 million in cash and marketable securities, the company possesses an estimated 7.2 years of cash runway at its current burn rate. This liquidity "parachute" provides the necessary capital to fund its long-cycle commercialization efforts, even amidst an accumulated deficit of $280 million.

Sector Positioning & Strategic Moats: The Amorphous Alloy Advantage

From a material science perspective, Liquidmetal’s strategic moat lies in the unique atomic structure of its amorphous alloys. Unlike the crystalline grain structures of traditional stainless steel or titanium, Liquidmetal’s random atomic structure eliminates "dislocations," granting the material unparalleled yield strength, high elastic limits, and superior corrosion resistance.

More importantly, the commercial value proposition rests on its "net-shape casting" process. Operating similarly to thermoplastic injection molding, this process drastically reduces the need for expensive secondary machining, offering superior dimensional control for complex, high-precision components. Constrained by a historical licensing agreement that grants Apple Inc. exclusive rights in the consumer electronics space, LQMT is actively repositioning this technology to capture high-margin, long-tail opportunities in humanoid robotics, medical devices, and automotive components.

Strategic Pivots & Supply Chain Realignment: The China JV Gamble

The most defining strategic initiative of 2025 is LQMT's aggressive supply chain realignment. Historically, the company has operated with a critical vulnerability: a 100% reliance on a related-party Chinese manufacturer (Yihao/Eontec) for alloying and parts production.

To mitigate this bottleneck and capture higher value-chain margins, LQMT established Hangzhou Feifeng Liquidmetal Co. Ltd. in July 2025. By injecting $4.2 million in initial capital for a 70% controlling stake, management is making a concentrated bet on localized Chinese manufacturing. Expected to reach full production capacity in 2026, this facility is designed to transition LQMT from a passive licensor to a vertically integrated manufacturer, theoretically improving cost-plus pricing dynamics and accelerating time-to-market for international clients.

HDIN Viewpoint: Navigating Governance and Cyclical Headwinds

HDIN Research assigns a high-risk profile to LQMT’s current operational paradigm. While the shift to the Hangzhou joint venture demonstrates strong management execution (a high "Say/Do ratio" regarding infrastructure layout), the underlying business fundamentals raise several prudent red flags:

1. The R&D Paradox: For a company marketing itself as a disruptive deep-tech innovator, FY2025 R&D expenditure plummeted to an alarming $14,000 (just 1.8% of revenue). This near-total suspension of internal innovation risks eroding the company’s technological lead against emerging alternatives like Metal Injection Molding (MIM) and advanced 3D printing.

2. Customer Concentration Vulnerability: In 2025, just three clients accounted for 86% of total revenue, with a single client representing 60% of accounts receivable. In an environment where sales cycles exceed 12 months, this concentration poses a systemic risk to business continuity.

3. Governance and Alignment: Investors must carefully monitor related-party transactions and executive compensation structures. The 2025 issuance of 15 million stock options at a low strike price of $0.04 to management, coupled with heavy reliance on Chairman Lugee Li’s affiliated manufacturing entities, necessitates enhanced scrutiny regarding corporate governance and shareholder dilution.

Ultimately, LQMT's survival and path to profitability hinge entirely on the execution of the 2026 Hangzhou facility. If this asset-heavy pivot fails to generate substantial, routine commercial orders, the company's robust liquidity buffer will rapidly transform into a depreciating asset.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Liquidmetal Technologies(LQMT) 2025 Strategic Pivot: From Patent Holder to Global Manufacturer

Capital Allocation Efficiency: High Liquidity Masks Operational DeficitsA deeper dive into LQMT’s financial health reveals structural profitability challenges. FY2025 total revenue contracted by 8.8% year-over-year to a mere $784,000, primarily driven by cyclical headwinds and reduced shipments in health-monitoring rings and medical device components.

While gross margins saw a marginal improvement to 29.3% (up from 25.2% in 2024), the absolute gross profit of $230,000 is vastly insufficient to sustain the company's corporate overhead. Consequently, the company posted a staggering operating loss of $3.74 million, translating to an operating margin of -477.3%. Essentially, for every dollar generated, LQMT spends nearly $4.77 in operational costs.

Despite this operational cash bleed, LQMT maintains a remarkably high financial safety margin. With a current ratio of 8.85 and holding approximately $19.76 million in cash and marketable securities, the company possesses an estimated 7.2 years of cash runway at its current burn rate. This liquidity "parachute" provides the necessary capital to fund its long-cycle commercialization efforts, even amidst an accumulated deficit of $280 million.

Sector Positioning & Strategic Moats: The Amorphous Alloy Advantage

From a material science perspective, Liquidmetal’s strategic moat lies in the unique atomic structure of its amorphous alloys. Unlike the crystalline grain structures of traditional stainless steel or titanium, Liquidmetal’s random atomic structure eliminates "dislocations," granting the material unparalleled yield strength, high elastic limits, and superior corrosion resistance.

More importantly, the commercial value proposition rests on its "net-shape casting" process. Operating similarly to thermoplastic injection molding, this process drastically reduces the need for expensive secondary machining, offering superior dimensional control for complex, high-precision components. Constrained by a historical licensing agreement that grants Apple Inc. exclusive rights in the consumer electronics space, LQMT is actively repositioning this technology to capture high-margin, long-tail opportunities in humanoid robotics, medical devices, and automotive components.

Strategic Pivots & Supply Chain Realignment: The China JV Gamble

The most defining strategic initiative of 2025 is LQMT's aggressive supply chain realignment. Historically, the company has operated with a critical vulnerability: a 100% reliance on a related-party Chinese manufacturer (Yihao/Eontec) for alloying and parts production.

To mitigate this bottleneck and capture higher value-chain margins, LQMT established Hangzhou Feifeng Liquidmetal Co. Ltd. in July 2025. By injecting $4.2 million in initial capital for a 70% controlling stake, management is making a concentrated bet on localized Chinese manufacturing. Expected to reach full production capacity in 2026, this facility is designed to transition LQMT from a passive licensor to a vertically integrated manufacturer, theoretically improving cost-plus pricing dynamics and accelerating time-to-market for international clients.

HDIN Viewpoint: Navigating Governance and Cyclical Headwinds

HDIN Research assigns a high-risk profile to LQMT’s current operational paradigm. While the shift to the Hangzhou joint venture demonstrates strong management execution (a high "Say/Do ratio" regarding infrastructure layout), the underlying business fundamentals raise several prudent red flags:

1. The R&D Paradox: For a company marketing itself as a disruptive deep-tech innovator, FY2025 R&D expenditure plummeted to an alarming $14,000 (just 1.8% of revenue). This near-total suspension of internal innovation risks eroding the company’s technological lead against emerging alternatives like Metal Injection Molding (MIM) and advanced 3D printing.

2. Customer Concentration Vulnerability: In 2025, just three clients accounted for 86% of total revenue, with a single client representing 60% of accounts receivable. In an environment where sales cycles exceed 12 months, this concentration poses a systemic risk to business continuity.

3. Governance and Alignment: Investors must carefully monitor related-party transactions and executive compensation structures. The 2025 issuance of 15 million stock options at a low strike price of $0.04 to management, coupled with heavy reliance on Chairman Lugee Li’s affiliated manufacturing entities, necessitates enhanced scrutiny regarding corporate governance and shareholder dilution.

Ultimately, LQMT's survival and path to profitability hinge entirely on the execution of the 2026 Hangzhou facility. If this asset-heavy pivot fails to generate substantial, routine commercial orders, the company's robust liquidity buffer will rapidly transform into a depreciating asset.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com