Agent AI 2025: A Narrative-Driven AI Pivot Masking Deep Financial Distress

Date : 2026-03-21

Reading : 115

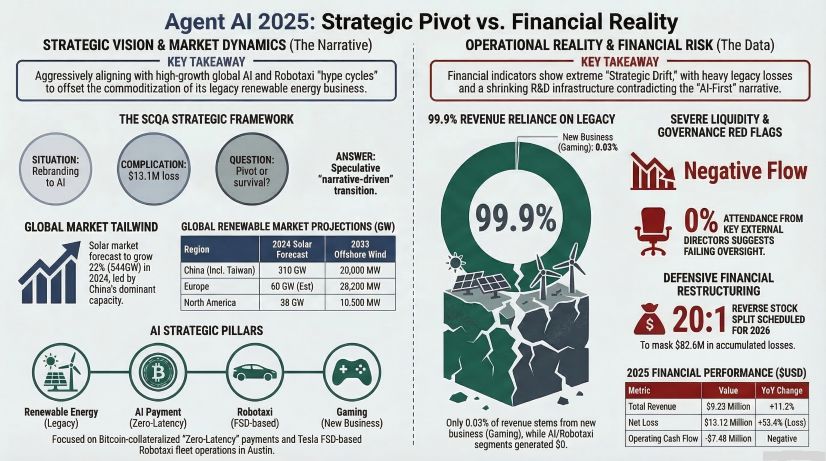

Agent AI Co., Ltd. (formerly DGP) is currently executing one of the most radical strategic transitions in the market, attempting to pivot from a traditional renewable energy Engineering, Procurement, and Construction (EPC) contractor into an "AI-first" conglomerate. However, beneath the aggressive rebranding and high-profile acquisitions lies a fragile financial foundation. While management projects a futuristic vision of AI payment systems, Robotaxi fleet operations, and global gaming, structural mismatches in revenue generation and severe liquidity constraints paint a highly cautionary tale for 2025.

Figure Agent Al 2025: Strategic Pivot vs. Financial Reality

Strategic Pivots and Sector Positioning

Strategic Pivots and Sector Positioning

Agent AI’s recent operational overhaul under its new largest shareholder, Satoshi Holdings, represents a profound strategic pivot aimed at capturing high-margin tech valuations. The company's new sector positioning is spread across three ambitious verticals: an AI Agent stablecoin payment system via Agent AI Labs, a Tesla FSD-reliant Robotaxi fleet operator in Austin, Texas, and a global gaming push through the acquisition of Needs Games.

Yet, operational efficiency and market expansion in these new sectors remain unproven. A closer look at the data reveals that these initiatives are largely theoretical or in early beta phases. In the Robotaxi space, Agent AI acts merely as a secondary fleet operator within the Tesla ecosystem, heavily reliant on third-party algorithms. This lack of proprietary underlying technology severely limits the company's ability to build genuine strategic moats, positioning them as an entrant rather than a leader in an increasingly saturated AI landscape.

Capital Allocation Efficiency and Financial Health

The core disconnect within Agent AI lies in its capital allocation efficiency versus actual revenue generation. In 2025, the company posted consolidated revenues of approximately $9.23 million (a 11.2% year-over-year increase). However, an overwhelming 99.9% of this revenue remains tethered to legacy, low-margin renewable energy and O&M operations in South Korea.

Cyclical headwinds, geopolitical instability, and rising raw material costs caused gross margins to collapse from 16.96% in 2024 to a mere 8.96% in 2025. This structural deterioration of the core business drove an operating loss of $6.56 million and a net loss of $13.13 million. Furthermore, a 91% precipitous drop in contract liabilities—a leading indicator for future EPC revenue—suggests that the company's existing backlog is rapidly depleting. To mask these capital vulnerabilities and wipe out $82.62 million in accumulated deficits, the board recently resorted to a desperate 20:1 reverse stock split, highlighting a balance sheet under extreme duress.

Governance Red Flags and the Erosion of Strategic Moats

To sustain its "AI-first" narrative, Agent AI has engaged in highly questionable M&A practices. The late-2025 acquisition of Needs Games generated approximately $4.6 million in goodwill, despite the gaming studio carrying deeply negative net assets and ongoing operational losses. This aggressive accounting introduces massive goodwill impairment risks for the upcoming fiscal year.

Furthermore, HDIN Research notes a severe contradiction in the company's R&D narrative. Achieving zero-latency AI payment systems requires intense technological investment; however, Agent AI recently dissolved its independent R&D department, folding it into general operations. Compounded by a board of directors lacking fundamental tech DNA and exhibiting highly irregular attendance records (0% for select external directors), the company’s governance framework raises critical red flags regarding oversight and strategic execution.

The HDIN Viewpoint: Hype-Cycle Alignment vs. Fundamental Value

Based on our independent analysis, Agent AI is executing a "narrative-driven" transition rather than a "capability-driven" one. The company has changed its name four times in five years (from KR P&E to Daehan Green Power, to DGP, and now Agent AI). In the view of HDIN Research, this pattern is a defensive rebranding strategy designed to align with market hype cycles, distracting from a history of operational failures in the energy sector.

Agent AI currently functions as a distressed energy company cloaked in an AI narrative. Until the company can demonstrate organic cash flow generation from its tech verticals and prove the LTV (Life-Time Value) of its new user base, its strategic moats remain highly vulnerable. Institutional investors should approach this valuation with extreme caution, as the current capital structure and lack of proprietary tech assets present substantial downside risks.

Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Agent Al 2025: Strategic Pivot vs. Financial Reality

Strategic Pivots and Sector PositioningAgent AI’s recent operational overhaul under its new largest shareholder, Satoshi Holdings, represents a profound strategic pivot aimed at capturing high-margin tech valuations. The company's new sector positioning is spread across three ambitious verticals: an AI Agent stablecoin payment system via Agent AI Labs, a Tesla FSD-reliant Robotaxi fleet operator in Austin, Texas, and a global gaming push through the acquisition of Needs Games.

Yet, operational efficiency and market expansion in these new sectors remain unproven. A closer look at the data reveals that these initiatives are largely theoretical or in early beta phases. In the Robotaxi space, Agent AI acts merely as a secondary fleet operator within the Tesla ecosystem, heavily reliant on third-party algorithms. This lack of proprietary underlying technology severely limits the company's ability to build genuine strategic moats, positioning them as an entrant rather than a leader in an increasingly saturated AI landscape.

Capital Allocation Efficiency and Financial Health

The core disconnect within Agent AI lies in its capital allocation efficiency versus actual revenue generation. In 2025, the company posted consolidated revenues of approximately $9.23 million (a 11.2% year-over-year increase). However, an overwhelming 99.9% of this revenue remains tethered to legacy, low-margin renewable energy and O&M operations in South Korea.

Cyclical headwinds, geopolitical instability, and rising raw material costs caused gross margins to collapse from 16.96% in 2024 to a mere 8.96% in 2025. This structural deterioration of the core business drove an operating loss of $6.56 million and a net loss of $13.13 million. Furthermore, a 91% precipitous drop in contract liabilities—a leading indicator for future EPC revenue—suggests that the company's existing backlog is rapidly depleting. To mask these capital vulnerabilities and wipe out $82.62 million in accumulated deficits, the board recently resorted to a desperate 20:1 reverse stock split, highlighting a balance sheet under extreme duress.

Governance Red Flags and the Erosion of Strategic Moats

To sustain its "AI-first" narrative, Agent AI has engaged in highly questionable M&A practices. The late-2025 acquisition of Needs Games generated approximately $4.6 million in goodwill, despite the gaming studio carrying deeply negative net assets and ongoing operational losses. This aggressive accounting introduces massive goodwill impairment risks for the upcoming fiscal year.

Furthermore, HDIN Research notes a severe contradiction in the company's R&D narrative. Achieving zero-latency AI payment systems requires intense technological investment; however, Agent AI recently dissolved its independent R&D department, folding it into general operations. Compounded by a board of directors lacking fundamental tech DNA and exhibiting highly irregular attendance records (0% for select external directors), the company’s governance framework raises critical red flags regarding oversight and strategic execution.

The HDIN Viewpoint: Hype-Cycle Alignment vs. Fundamental Value

Based on our independent analysis, Agent AI is executing a "narrative-driven" transition rather than a "capability-driven" one. The company has changed its name four times in five years (from KR P&E to Daehan Green Power, to DGP, and now Agent AI). In the view of HDIN Research, this pattern is a defensive rebranding strategy designed to align with market hype cycles, distracting from a history of operational failures in the energy sector.

Agent AI currently functions as a distressed energy company cloaked in an AI narrative. Until the company can demonstrate organic cash flow generation from its tech verticals and prove the LTV (Life-Time Value) of its new user base, its strategic moats remain highly vulnerable. Institutional investors should approach this valuation with extreme caution, as the current capital structure and lack of proprietary tech assets present substantial downside risks.

Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com