The 2026 Memory Semiconductor Landscape: AI Structural Moats, Capital Allocation, and Geopolitical Headwinds

Date : 2026-03-19

Reading : 1177

The global memory semiconductor industry is undergoing a profound paradigm shift, transitioning from a cyclical commodity market to an architecture-defined ecosystem driven by artificial intelligence. Based on a comprehensive audit of 2025 financial disclosures from industry heavyweights—Samsung, SK hynix, Micron, and niche innovator Everspin—HDIN Research reveals that 2026 will be defined by a high-stakes arms race in advanced node capacity, HBM4 commercialization, and the rising costs of localized supply chains.

Figure Global Memory Semiconductor Landscape 2025: The Shift to Al-Architecture

Rather than merely chasing volume, the sector's ultimate victors will be determined by capital allocation efficiency and the ability to navigate complex geopolitical frictions.

Rather than merely chasing volume, the sector's ultimate victors will be determined by capital allocation efficiency and the ability to navigate complex geopolitical frictions.

Structural Tailwinds: The AI Server and Edge Computing Paradigm

The integration of generative AI is fundamentally altering pricing power and sector positioning. Market demand is no longer broad-based; it is a "single-engine" hyper-growth model centered on AI servers, flanked by rising requirements in edge computing and automotive reliability.

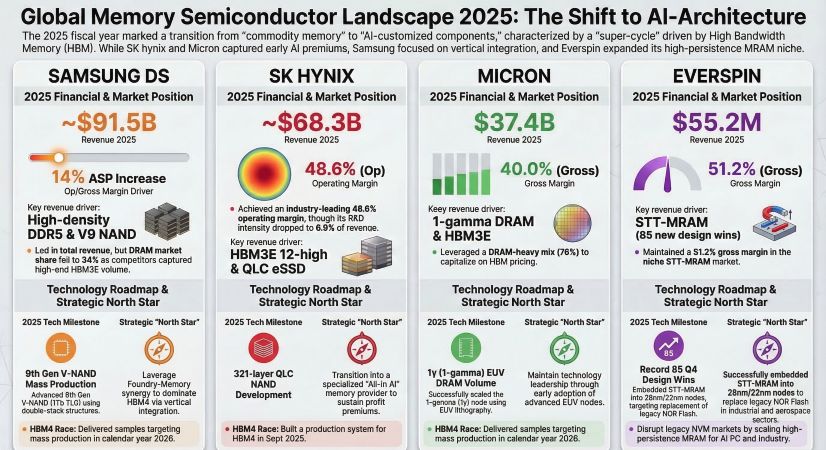

* The HBM Profitability Premium: High Bandwidth Memory (HBM) has become the undisputed profit engine. SK hynix has leveraged its first-mover advantage in HBM3E and proprietary Advanced MR-MUF packaging to capture massive AI premiums, achieving an astonishing 48.6% operating margin in 2025. By 2026, the transition to HBM4 will catalyze the next server upgrade cycle, cementing memory as a core computational bottleneck rather than mere data storage.

* Edge AI and Niche Strategic Moats: Beyond the data center, Edge AI and AI PCs (which now demand a 16GB memory baseline) are poised for a 2026 breakout. In this arena, Everspin has carved out a deep, highly defensible strategic moat. By utilizing magnetic tunnel junctions (MTJ) rather than traditional electrical charge to store data, Everspin’s EAR99 MRAM technology is immune to alpha particle radiation. This physical IP monopoly allows them to dominate mission-critical aerospace and industrial IoT sectors, boasting gross margins above 51% despite their smaller operational scale.

Capital Allocation Efficiency: The Advanced Node Arms Race

Capital expenditures (Capex) across the "Big Three" are moving in aggressive synchronization, specifically targeting 1-gamma DRAM, 300+ layer NAND, and HBM4. However, the *efficiency* of this capital allocation reveals divergent strategic postures:

* SK hynix (The Aggressive Expander): Deploying over $21.2 billion in Capex, SK hynix is utilizing its massive internal cash flow to aggressively build out its M15X fab. Their strategy is pure market-share dominance in the AI premium tier.

* Micron (The Prudent Innovator): Micron is balancing technological leaps with extreme balance-sheet resilience. With a highly defensive net debt ratio of just 9.1% and a $15.8 billion Capex budget, Micron is pioneering EUV integration for its 1-gamma nodes while keeping its financial powder dry against macroeconomic shocks.

* Samsung (The Vertical Ecosystem): With a staggering $37 billion Capex, Samsung is playing the long game. By engineering a vertical "Foundry + Memory" ecosystem, Samsung aims to utilize its 2nm GAA process for HBM4 base-die production, offering unmatched throughput elasticity should AI demand exceed current forecasts.

Cyclical Headwinds: Geopolitical Frictions and Localized Costs

Despite record-breaking AI profits, the sector faces formidable cyclical headwinds driven by geopolitical fragmentation. The push for localized manufacturing is establishing a new, higher ceiling for operational costs.

While the U.S. CHIPS Act provides vital "painkillers"—such as Micron’s $6.4 billion direct grant and substantial investment tax credits—these subsidies come with stringent guardrails. Building cutting-edge fabs in the U.S. incurs significantly higher construction and labor costs, exacerbated by a severe shortage of specialized engineering talent. Furthermore, regulatory market-access restrictions in China act as a persistent frictional drag, limiting the strategic flexibility and geographic revenue potential for U.S. and allied manufacturers.

HDIN Viewpoint: Navigating the 2026 Paradigm Shift

From our institutional perspective at HDIN Research, the 2026 memory market will not be won purely on scale, but on the ability to balance architectural innovation with disciplined capital deployment. SK hynix currently holds the strategic high ground with unmatched HBM profitability, while Micron exhibits the strongest financial resilience, and Samsung possesses the ultimate scale-out elasticity.

However, we advise institutional investors to exercise caution regarding the synchronized Capex boom. The industry is highly reliant on Long-Term Agreements (LTAs) with hyperscalers to justify these massive investments. If AI inference demand normalizes, or if the "double-booking" illusion in the supply chain unwinds, suppliers may be forced to pivot advanced node capacity back to conventional DRAM. This could trigger a severe oversupply cycle, rapidly collapsing the current ASP (Average Selling Price) premiums. Navigating 2026 will require vigilance against this impending cyclical trap and a strict focus on companies with authentic, radiation-proof, or AI-integrated technological moats.

Get presentation:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Global Memory Semiconductor Landscape 2025: The Shift to Al-Architecture

Rather than merely chasing volume, the sector's ultimate victors will be determined by capital allocation efficiency and the ability to navigate complex geopolitical frictions. Structural Tailwinds: The AI Server and Edge Computing Paradigm

The integration of generative AI is fundamentally altering pricing power and sector positioning. Market demand is no longer broad-based; it is a "single-engine" hyper-growth model centered on AI servers, flanked by rising requirements in edge computing and automotive reliability.

* The HBM Profitability Premium: High Bandwidth Memory (HBM) has become the undisputed profit engine. SK hynix has leveraged its first-mover advantage in HBM3E and proprietary Advanced MR-MUF packaging to capture massive AI premiums, achieving an astonishing 48.6% operating margin in 2025. By 2026, the transition to HBM4 will catalyze the next server upgrade cycle, cementing memory as a core computational bottleneck rather than mere data storage.

* Edge AI and Niche Strategic Moats: Beyond the data center, Edge AI and AI PCs (which now demand a 16GB memory baseline) are poised for a 2026 breakout. In this arena, Everspin has carved out a deep, highly defensible strategic moat. By utilizing magnetic tunnel junctions (MTJ) rather than traditional electrical charge to store data, Everspin’s EAR99 MRAM technology is immune to alpha particle radiation. This physical IP monopoly allows them to dominate mission-critical aerospace and industrial IoT sectors, boasting gross margins above 51% despite their smaller operational scale.

Capital Allocation Efficiency: The Advanced Node Arms Race

Capital expenditures (Capex) across the "Big Three" are moving in aggressive synchronization, specifically targeting 1-gamma DRAM, 300+ layer NAND, and HBM4. However, the *efficiency* of this capital allocation reveals divergent strategic postures:

* SK hynix (The Aggressive Expander): Deploying over $21.2 billion in Capex, SK hynix is utilizing its massive internal cash flow to aggressively build out its M15X fab. Their strategy is pure market-share dominance in the AI premium tier.

* Micron (The Prudent Innovator): Micron is balancing technological leaps with extreme balance-sheet resilience. With a highly defensive net debt ratio of just 9.1% and a $15.8 billion Capex budget, Micron is pioneering EUV integration for its 1-gamma nodes while keeping its financial powder dry against macroeconomic shocks.

* Samsung (The Vertical Ecosystem): With a staggering $37 billion Capex, Samsung is playing the long game. By engineering a vertical "Foundry + Memory" ecosystem, Samsung aims to utilize its 2nm GAA process for HBM4 base-die production, offering unmatched throughput elasticity should AI demand exceed current forecasts.

Cyclical Headwinds: Geopolitical Frictions and Localized Costs

Despite record-breaking AI profits, the sector faces formidable cyclical headwinds driven by geopolitical fragmentation. The push for localized manufacturing is establishing a new, higher ceiling for operational costs.

While the U.S. CHIPS Act provides vital "painkillers"—such as Micron’s $6.4 billion direct grant and substantial investment tax credits—these subsidies come with stringent guardrails. Building cutting-edge fabs in the U.S. incurs significantly higher construction and labor costs, exacerbated by a severe shortage of specialized engineering talent. Furthermore, regulatory market-access restrictions in China act as a persistent frictional drag, limiting the strategic flexibility and geographic revenue potential for U.S. and allied manufacturers.

HDIN Viewpoint: Navigating the 2026 Paradigm Shift

From our institutional perspective at HDIN Research, the 2026 memory market will not be won purely on scale, but on the ability to balance architectural innovation with disciplined capital deployment. SK hynix currently holds the strategic high ground with unmatched HBM profitability, while Micron exhibits the strongest financial resilience, and Samsung possesses the ultimate scale-out elasticity.

However, we advise institutional investors to exercise caution regarding the synchronized Capex boom. The industry is highly reliant on Long-Term Agreements (LTAs) with hyperscalers to justify these massive investments. If AI inference demand normalizes, or if the "double-booking" illusion in the supply chain unwinds, suppliers may be forced to pivot advanced node capacity back to conventional DRAM. This could trigger a severe oversupply cycle, rapidly collapsing the current ASP (Average Selling Price) premiums. Navigating 2026 will require vigilance against this impending cyclical trap and a strict focus on companies with authentic, radiation-proof, or AI-integrated technological moats.

Get presentation:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com