Zomedica FY2025: Navigating Cyclical Headwinds Through Strategic Moats and Platform Ecosystems

Date : 2026-03-24

Reading : 91

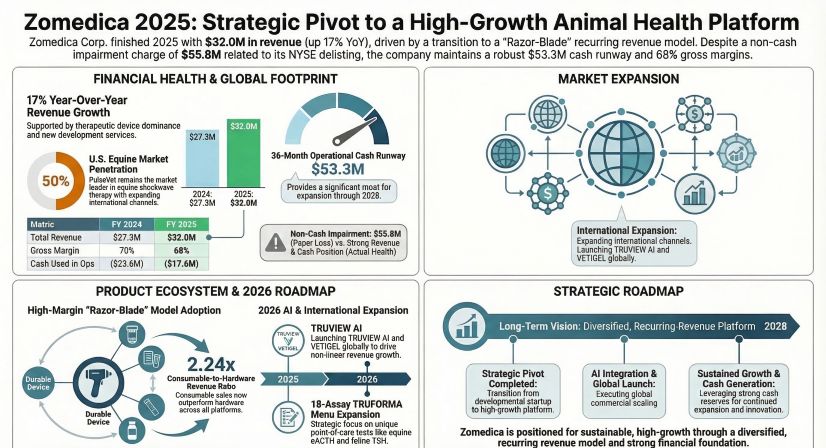

According to the latest deep-dive analysis by HDIN Research, Zomedica Corp.’s FY2025 financial performance highlights a critical inflection point: the complex transition from a product-oriented R&D firm to a multi-dimensional animal health platform. While the company achieved robust top-line expansion, its core profitability remains under pressure from severe cyclical headwinds and capital market restructuring. Zomedica’s FY2025 narrative is defined by a dichotomy—steadily expanding operational scale offset by a massive non-cash asset impairment following its delisting from the NYSE American.

Figure Zomedica 2025: Strategic Pivot to a High-Growth Animal Health Platform

Here is HDIN Research’s institutional perspective on Zomedica’s capital allocation efficiency, sector positioning, and future growth engines.

Here is HDIN Research’s institutional perspective on Zomedica’s capital allocation efficiency, sector positioning, and future growth engines.

Financial Health: Revenue Surges Amidst "Big Bath" Asset Impairments

Operational efficiency and market expansion drove a 17.4% revenue surge, bringing Zomedica’s FY2025 total revenue to $32.03 million. This top-line growth was primarily catalyzed by sustained demand for PulseVet® consumables, the rollout of new TRUFORMA® diagnostic assays, and the strategic launch of VETIGEL®. However, gross margins experienced a slight compression to 68% (down from 70% in FY2024), largely due to increased depreciation expenses from newly completed capital projects that partially offset the scale economies of fixed-cost absorption.

The most critical anomaly in the FY2025 balance sheet is the $55.83 million non-cash asset impairment triggered in Q1. Driven by a depressed market capitalization that forced an OTCQB market transition, Zomedica executed a strategic write-down—zeroing out $45.56 million in goodwill associated with legacy acquisitions, alongside reductions in intangible assets and PPE. While this pushed net losses to $81.86 million, this aggressive clearing of the balance sheet mitigates future depreciation overhangs.

Despite the net loss, Zomedica maintains robust capital allocation efficiency. The company holds $53.26 million in total liquidity. More importantly, management successfully reduced the operational cash burn rate by 25% year-over-year to $1.47 million per month, securing an estimated 36-month operational runway to fund ongoing clinical research and commercialization efforts.

Sector Positioning: The Power of the "Razor-Blade" Moat

Zomedica’s strategic moat is heavily anchored in its Therapeutic Devices segment, which generated $26.2 million (81.8% of total revenue) in FY2025. The company has successfully institutionalized a high-margin "razor-blade" business model.

* Therapeutic Dominance: The PulseVet® electrohydraulic shockwave platform commands a formidable 50% penetration rate within U.S. equine clinics. The consumable-to-capital revenue ratio in this segment stands at a highly efficient 2.17x. The introduction of the X-Trode® handpiece—which allows for companion animal treatment without sedation—is rapidly accelerating Zomedica's footprint in the vastly larger small-animal clinic market.

* Diagnostic Penetration: Although a smaller revenue contributor ($2.8 million), the TRUFORMA® point-of-care (POC) diagnostic platform boasts an impressive 3.08x consumable-to-instrument ratio. This is driven by the Customer Appreciation Program (CAP), which trades free instrument placements for long-term, high-margin reagent purchasing commitments.

Strategic Pivots & Industry Outlook

To hedge against the inherent volatility of the veterinary market, Zomedica is actively diversifying its revenue streams. In Q3 2025, the company launched a "Development Services" division, monetizing excess engineering and manufacturing capacity to generate $3.03 million in new, non-cyclical revenue.

Looking toward 2026, HDIN Research identifies three primary growth engines that will dictate Zomedica’s path to profitability:

1. AI-Driven Subscription Models: The TRUVIEW® digital cytology platform will integrate automated Artificial Intelligence (AI) hematology interpretations in 2026. This upgrades the platform’s subscription model, reducing clinic reliance on costly third-party pathologists.

2. High-Margin Consumables: The global commercialization of VETIGEL®—a pure-consumable hemostatic gel requiring zero equipment installation—promises to optimize the company's gross margin structure rapidly.

3. Targeted International Expansion: Rather than building from scratch, Zomedica is utilizing "Product Stacking." The company plans to leverage its mature PulseVet and Assisi international distribution networks in Europe, Asia, and South America to distribute new diagnostic and surgical products, minimizing marginal customer acquisition costs.

HDIN Viewpoint

Zomedica is executing a high-risk, high-reward pivot toward a "Diagnostic + Therapeutic" closed-loop ecosystem. While the firm possesses a deep competitive moat in therapeutic devices, it remains a high-growth challenger against entrenched industry giants like IDEXX and Zoetis in the diagnostic space. Investors and market stakeholders must look beyond the noise of the FY2025 impairment. The true litmus test for Zomedica will be its ability to translate its 36-month liquidity runway into sustainable free cash flow, closely monitoring potential supply chain vulnerabilities (such as the reliance on Eastern Europe for Palladium) and the P&L volatility introduced by its Stock Appreciation Rights (SARs) liabilities.

Get presentation:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Zomedica 2025: Strategic Pivot to a High-Growth Animal Health Platform

Here is HDIN Research’s institutional perspective on Zomedica’s capital allocation efficiency, sector positioning, and future growth engines.Financial Health: Revenue Surges Amidst "Big Bath" Asset Impairments

Operational efficiency and market expansion drove a 17.4% revenue surge, bringing Zomedica’s FY2025 total revenue to $32.03 million. This top-line growth was primarily catalyzed by sustained demand for PulseVet® consumables, the rollout of new TRUFORMA® diagnostic assays, and the strategic launch of VETIGEL®. However, gross margins experienced a slight compression to 68% (down from 70% in FY2024), largely due to increased depreciation expenses from newly completed capital projects that partially offset the scale economies of fixed-cost absorption.

The most critical anomaly in the FY2025 balance sheet is the $55.83 million non-cash asset impairment triggered in Q1. Driven by a depressed market capitalization that forced an OTCQB market transition, Zomedica executed a strategic write-down—zeroing out $45.56 million in goodwill associated with legacy acquisitions, alongside reductions in intangible assets and PPE. While this pushed net losses to $81.86 million, this aggressive clearing of the balance sheet mitigates future depreciation overhangs.

Despite the net loss, Zomedica maintains robust capital allocation efficiency. The company holds $53.26 million in total liquidity. More importantly, management successfully reduced the operational cash burn rate by 25% year-over-year to $1.47 million per month, securing an estimated 36-month operational runway to fund ongoing clinical research and commercialization efforts.

Sector Positioning: The Power of the "Razor-Blade" Moat

Zomedica’s strategic moat is heavily anchored in its Therapeutic Devices segment, which generated $26.2 million (81.8% of total revenue) in FY2025. The company has successfully institutionalized a high-margin "razor-blade" business model.

* Therapeutic Dominance: The PulseVet® electrohydraulic shockwave platform commands a formidable 50% penetration rate within U.S. equine clinics. The consumable-to-capital revenue ratio in this segment stands at a highly efficient 2.17x. The introduction of the X-Trode® handpiece—which allows for companion animal treatment without sedation—is rapidly accelerating Zomedica's footprint in the vastly larger small-animal clinic market.

* Diagnostic Penetration: Although a smaller revenue contributor ($2.8 million), the TRUFORMA® point-of-care (POC) diagnostic platform boasts an impressive 3.08x consumable-to-instrument ratio. This is driven by the Customer Appreciation Program (CAP), which trades free instrument placements for long-term, high-margin reagent purchasing commitments.

Strategic Pivots & Industry Outlook

To hedge against the inherent volatility of the veterinary market, Zomedica is actively diversifying its revenue streams. In Q3 2025, the company launched a "Development Services" division, monetizing excess engineering and manufacturing capacity to generate $3.03 million in new, non-cyclical revenue.

Looking toward 2026, HDIN Research identifies three primary growth engines that will dictate Zomedica’s path to profitability:

1. AI-Driven Subscription Models: The TRUVIEW® digital cytology platform will integrate automated Artificial Intelligence (AI) hematology interpretations in 2026. This upgrades the platform’s subscription model, reducing clinic reliance on costly third-party pathologists.

2. High-Margin Consumables: The global commercialization of VETIGEL®—a pure-consumable hemostatic gel requiring zero equipment installation—promises to optimize the company's gross margin structure rapidly.

3. Targeted International Expansion: Rather than building from scratch, Zomedica is utilizing "Product Stacking." The company plans to leverage its mature PulseVet and Assisi international distribution networks in Europe, Asia, and South America to distribute new diagnostic and surgical products, minimizing marginal customer acquisition costs.

HDIN Viewpoint

Zomedica is executing a high-risk, high-reward pivot toward a "Diagnostic + Therapeutic" closed-loop ecosystem. While the firm possesses a deep competitive moat in therapeutic devices, it remains a high-growth challenger against entrenched industry giants like IDEXX and Zoetis in the diagnostic space. Investors and market stakeholders must look beyond the noise of the FY2025 impairment. The true litmus test for Zomedica will be its ability to translate its 36-month liquidity runway into sustainable free cash flow, closely monitoring potential supply chain vulnerabilities (such as the reliance on Eastern Europe for Palladium) and the P&L volatility introduced by its Stock Appreciation Rights (SARs) liabilities.

Get presentation:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com