Playboy (PLBY Group) 2025 Financial Analysis: Navigating the Capital-Light Pivot Amid Structural Headwinds

Date : 2026-03-19

Reading : 354

The 2025 fiscal year marks a critical inflection point for Playboy, Inc. (PLBY Group). By aggressively dismantling its asset-intensive digital operations in favor of a "Capital-Light" IP licensing model, the company has successfully engineered an adjusted EBITDA turnaround. However, behind this margin expansion lies a fragile capital structure. While operational efficiency and market expansion drove a revenue uptick, HDIN Research notes that extreme customer concentration, impending debt covenants, and internal control deficiencies present significant cyclical and structural headwinds.

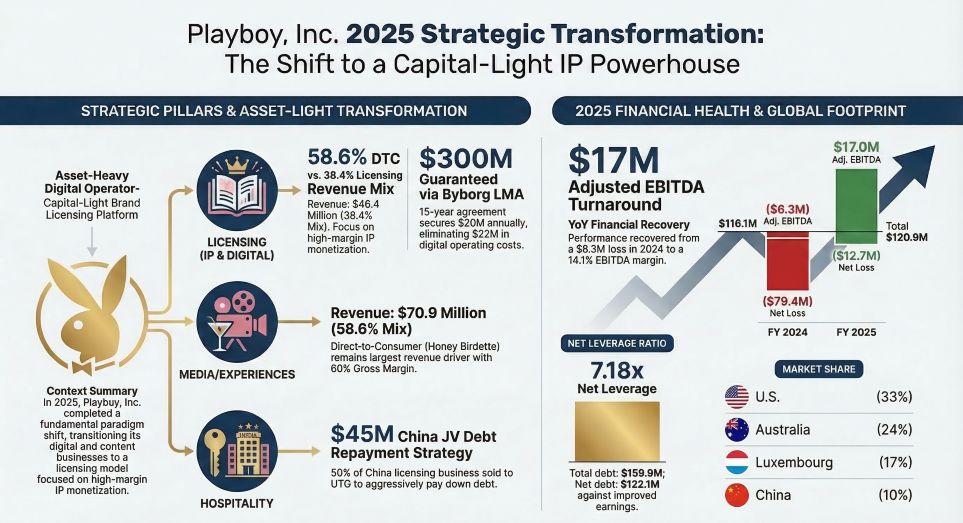

Figure Playboy Inc 2025 Strategic Transformation: The Shift to a Capital-LightIP Powerhouse

Financial Health: The Anatomy of an EBITDA Turnaround

Financial Health: The Anatomy of an EBITDA Turnaround

In FY2025, PLBY Group reported total revenue of $120.9 million, a 4.1% year-over-year increase. This growth was not a product of organic volume expansion, but rather a deliberate business model transformation. The strategic transition to a licensing-first framework drove an 87% surge in brand licensing revenue.

Consequently, the company successfully reversed its operational bleed, posting an Adjusted EBITDA of $17.0 million (up from negative $6.3 million in 2024). The "So What" factor here is profound: by offloading direct operational costs, PLBY's licensing segment now commands gross margins exceeding 90%. When stripping away one-time commission settlements, normalized licensing margins reached a staggering 95%, underscoring the formidable profitability of pure-play IP monetization.

Strategic Pivots: IP Monetization and DTC Optimization

PLBY Group’s survival strategy hinges on restructuring its two core verticals: Brand Licensing and Direct-to-Consumer (DTC).

* The Byborg LMA Masterstroke: The most defining strategic pivot of 2025 was the 15-year Licensing and Management Agreement (LMA) with Byborg Enterprises. By transferring the operational burden of its legacy digital platforms (Playboy Plus, Playboy TV, and Playboy Club), PLBY eliminated $22 million in digital revamping costs. In return, it secured a highly predictable revenue stream—a minimum guaranteed payment of $20 million annually.

* Geographic Arbitrage in DTC: For its Honey Birdette brand, PLBY ruthlessly optimized its physical footprint. By shuttering underperforming Australian storefronts and reallocating capital to the United States, the company realized massive geographic arbitrage. US stores currently generate double the average revenue and twice the EBITDA margin compared to their Australian counterparts, proving that targeted sector positioning yields outsized returns.

* The China Market Restructuring: Recognizing the strategic importance of the Asian market, PLBY terminated its previous JV and forged a new alliance with UTG Brands. This "New China JV" effectively trades a 50% equity stake for a $45 million cash injection—capital that is entirely earmarked for urgent debt reduction.

Assessing the Strategic Moats

While the Capital-Light model has fortified PLBY's balance sheet in the short term, its strategic moats are highly bifurcated. In the luxury intimates space, Honey Birdette's brand equity continues to command a premium pricing moat, effectively absorbing localized inflation.

Conversely, Playboy’s legacy moat in adult digital entertainment has been severely eroded. Disintermediation caused by Web 2.0 User-Generated Content (UGC) platforms, such as OnlyFans, has fundamentally decentralized content creation. By pivoting to the Byborg LMA, PLBY has effectively conceded the platform war, choosing to extract rent from its IP rather than compete in the digital trenches.

Capital Allocation Efficiency and Cyclical Headwinds

Despite the operational turnaround, PLBY’s capital allocation efficiency remains paralyzed by an over-leveraged balance sheet. The company currently operates with a precarious net leverage ratio of 7.18x.

To preserve liquidity, management utilized Payment-in-Kind (PIK) provisions to capitalize $7.2 million in interest expenses. While this preserves near-term cash, it inflates the principal balance of a looming $156.9 million debt wall concentrated in May 2028. Furthermore, macroeconomic inflation presents cyclical headwinds for the DTC segment. Escalating supply chain costs and softening discretionary income threaten to compress the current 60% gross margin of the DTC business, forcing potential discounting strategies that could dilute brand value.

HDIN Viewpoint: The Illusion of Stability

From an institutional perspective, HDIN Research maintains a cautious outlook on PLBY Group's 2025 recovery narrative. The transition to a Capital-Light framework has undoubtedly stopped the bleeding, but the foundation remains structurally compromised.

Our primary concern lies in corporate governance and reporting integrity. The adverse opinion issued by PLBY’s auditors regarding "Material Weaknesses" in internal controls—specifically around asset impairment, inventory valuation, and revenue recognition—suggests that the current financial repair may mask deeper operational opacity. Furthermore, the company has traded operational risk for severe concentration risk; Byborg alone now accounts for 17% of consolidated revenue. Investors and stakeholders must closely monitor the upcoming Q2 2026 leverage covenant test (capped at 9.0x). If the New China JV distributions face execution delays or Byborg falters, PLBY’s liquidity runway will rapidly evaporate.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Playboy Inc 2025 Strategic Transformation: The Shift to a Capital-LightIP Powerhouse

Financial Health: The Anatomy of an EBITDA TurnaroundIn FY2025, PLBY Group reported total revenue of $120.9 million, a 4.1% year-over-year increase. This growth was not a product of organic volume expansion, but rather a deliberate business model transformation. The strategic transition to a licensing-first framework drove an 87% surge in brand licensing revenue.

Consequently, the company successfully reversed its operational bleed, posting an Adjusted EBITDA of $17.0 million (up from negative $6.3 million in 2024). The "So What" factor here is profound: by offloading direct operational costs, PLBY's licensing segment now commands gross margins exceeding 90%. When stripping away one-time commission settlements, normalized licensing margins reached a staggering 95%, underscoring the formidable profitability of pure-play IP monetization.

Strategic Pivots: IP Monetization and DTC Optimization

PLBY Group’s survival strategy hinges on restructuring its two core verticals: Brand Licensing and Direct-to-Consumer (DTC).

* The Byborg LMA Masterstroke: The most defining strategic pivot of 2025 was the 15-year Licensing and Management Agreement (LMA) with Byborg Enterprises. By transferring the operational burden of its legacy digital platforms (Playboy Plus, Playboy TV, and Playboy Club), PLBY eliminated $22 million in digital revamping costs. In return, it secured a highly predictable revenue stream—a minimum guaranteed payment of $20 million annually.

* Geographic Arbitrage in DTC: For its Honey Birdette brand, PLBY ruthlessly optimized its physical footprint. By shuttering underperforming Australian storefronts and reallocating capital to the United States, the company realized massive geographic arbitrage. US stores currently generate double the average revenue and twice the EBITDA margin compared to their Australian counterparts, proving that targeted sector positioning yields outsized returns.

* The China Market Restructuring: Recognizing the strategic importance of the Asian market, PLBY terminated its previous JV and forged a new alliance with UTG Brands. This "New China JV" effectively trades a 50% equity stake for a $45 million cash injection—capital that is entirely earmarked for urgent debt reduction.

Assessing the Strategic Moats

While the Capital-Light model has fortified PLBY's balance sheet in the short term, its strategic moats are highly bifurcated. In the luxury intimates space, Honey Birdette's brand equity continues to command a premium pricing moat, effectively absorbing localized inflation.

Conversely, Playboy’s legacy moat in adult digital entertainment has been severely eroded. Disintermediation caused by Web 2.0 User-Generated Content (UGC) platforms, such as OnlyFans, has fundamentally decentralized content creation. By pivoting to the Byborg LMA, PLBY has effectively conceded the platform war, choosing to extract rent from its IP rather than compete in the digital trenches.

Capital Allocation Efficiency and Cyclical Headwinds

Despite the operational turnaround, PLBY’s capital allocation efficiency remains paralyzed by an over-leveraged balance sheet. The company currently operates with a precarious net leverage ratio of 7.18x.

To preserve liquidity, management utilized Payment-in-Kind (PIK) provisions to capitalize $7.2 million in interest expenses. While this preserves near-term cash, it inflates the principal balance of a looming $156.9 million debt wall concentrated in May 2028. Furthermore, macroeconomic inflation presents cyclical headwinds for the DTC segment. Escalating supply chain costs and softening discretionary income threaten to compress the current 60% gross margin of the DTC business, forcing potential discounting strategies that could dilute brand value.

HDIN Viewpoint: The Illusion of Stability

From an institutional perspective, HDIN Research maintains a cautious outlook on PLBY Group's 2025 recovery narrative. The transition to a Capital-Light framework has undoubtedly stopped the bleeding, but the foundation remains structurally compromised.

Our primary concern lies in corporate governance and reporting integrity. The adverse opinion issued by PLBY’s auditors regarding "Material Weaknesses" in internal controls—specifically around asset impairment, inventory valuation, and revenue recognition—suggests that the current financial repair may mask deeper operational opacity. Furthermore, the company has traded operational risk for severe concentration risk; Byborg alone now accounts for 17% of consolidated revenue. Investors and stakeholders must closely monitor the upcoming Q2 2026 leverage covenant test (capped at 9.0x). If the New China JV distributions face execution delays or Byborg falters, PLBY’s liquidity runway will rapidly evaporate.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com