Global Agricultural Machinery Outlook 2026: Navigating Cyclical Headwinds and the Transition to Digital Moats

Date : 2026-03-20

Reading : 168

The global agricultural machinery sector is currently navigating the trough of a pronounced downcycle, characterized by a sharp contraction in North America, mild stabilization in Europe, and structural bifurcation across the Asia-Pacific. As the industry transitions from a paradigm of "incremental mechanical growth" to "intelligent ecosystem replacement," original equipment manufacturers (OEMs) face a complex matrix of macroeconomic pressures.

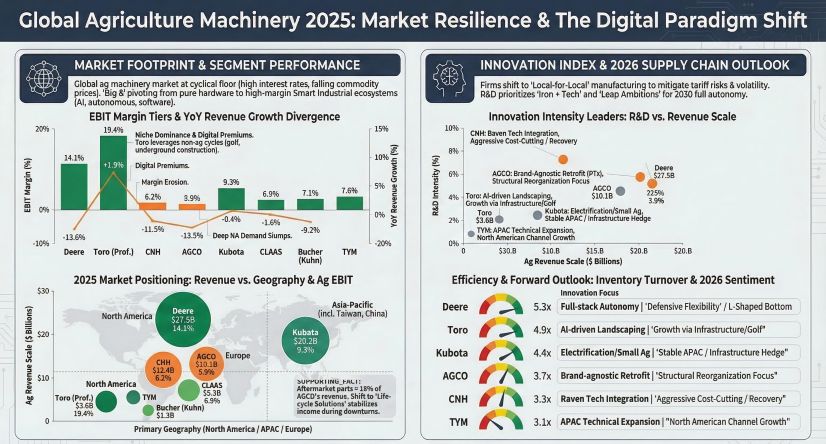

Based on our comprehensive analysis of 2025 fiscal disclosures from industry leaders—including Deere & Company, CNH Industrial, AGCO, CLAAS, Kubota, Bucher Industries, and The Toro Company—HDIN Research has identified a critical shift in how global heavyweights are defending their margins. The strategic playbook has officially pivoted from aggressive capacity expansion to defensive capital preservation and structural technology acquisition.

Figure Global Agriculture Machinery 2025: Market Resilience & The Digital Paradigm Shift

Here is our strategic breakdown of the cyclical headwinds, capital allocation efficiencies, and financial risk radars shaping the industry through 2026.

Here is our strategic breakdown of the cyclical headwinds, capital allocation efficiencies, and financial risk radars shaping the industry through 2026.

Cyclical Headwinds and the "L-Shaped" Trough

The operating environment for 2026 points toward an "L-shaped" stabilization rather than a rapid "V-shaped" recovery. The sector is currently battling a convergence of macroeconomic suppressors:

* The Squeeze on Farm Incomes: Sustained weakness in global crop prices (specifically wheat, corn, and soybeans) coupled with prolonged high interest rates has severely depressed farmer purchasing power.

* Supply Chain and Tariff Friction: Geopolitical fragmentation continues to inflate input ceilings. The shadow of retaliatory tariffs is eroding gross margins directly, with Deere alone facing an estimated $600 million direct tariff impact in 2025.

* The Destocking Dilemma: A severe channel destocking phase is the primary operational headwind. Historic highs in used equipment inventories are actively cannibalizing new machinery demand. Consequently, OEMs are forced to elevate sales incentive provisions to flush dealer channels, placing downward pressure on near-term profitability.

Capital Allocation Efficiency and Strategic Pivots

In response to top-line erosion, capital allocation logic among industry giants has diverged, highlighting distinct approaches to building strategic moats.

* Structural Transformation vs. Defensive Contraction: AGCO has exhibited aggressive portfolio restructuring, divesting its lower-margin Grain & Protein business to funnel capital directly into its PTx Trimble joint venture, prioritizing high-margin software and service revenues. Conversely, CNH Industrial has adopted a defensive posture, executing large-scale restructuring and workforce reductions to lower structural costs and repair its balance sheet amid a 33% plunge in North American high-horsepower tractor demand.

* The Counter-Cyclical Power of Diversification: Companies with robust non-agricultural portfolios demonstrated superior capital allocation efficiency. The Toro Company leveraged its highly profitable Professional Segment (driven by golf, landscaping, and underground construction) to offset agricultural weakness. Similarly, Kubota’s Water and Environment division provided a stable cash-flow buffer. These non-ag cash cows are not merely revenue diversifications; they serve as critical R&D funding mechanisms, allowing core technologies—like autonomous algorithms and hydraulic architectures—to be amortized across multiple industrial platforms.

Financial Risk Radar: Navigating Balance Sheet Vulnerabilities

As the market softens, HDIN Research advises stakeholders to look beyond top-line revenue and scrutinize asset quality. The current downcycle exposes several reporting vulnerabilities:

* Captive Finance and Residual Value Risks: As the prices of used agricultural machinery fall, the residual values of leased assets within OEM financial services divisions are highly susceptible to impairment. Furthermore, rising default rates in emerging markets, such as South America, demand close monitoring of whether OEMs are adequately provisioning for credit losses or delaying them to artificially sustain operating margins.

* The Commercial Reality of Tech Valuations: Over the past few years, OEMs acquired precision agriculture startups at massive premiums. The current tightening liquidity environment is forcing brutal commercial revaluations. CNH’s $172 million non-cash in-process R&D impairment related to Raven, and AGCO’s significant goodwill impairments for its tech units, signal that the commercialization of acquired autonomous technologies is facing friction.

* Cash Flow vs. Net Income Deviations: High-quality earnings are currently defined by cash conversion. Industry leaders like Deere and Toro have generated operating cash flows that significantly outpace net income by aggressively managing working capital and scaling back share repurchases to preserve liquidity.

Sector Positioning: The Race for Autonomous "Moats"

The hardware arms race is effectively over; the new competitive moat is forged in silicon, AI, and recurring software revenue. Regulatory pressures, such as California’s CARB zero-emission mandates and European Stage V emissions, are establishing a hard floor for compliance R&D, forcing OEMs to simultaneously fund green powertrains and autonomy.

Sector positioning is currently splitting into two distinct tech commercialization paths:

1. The "Full-Stack" Ecosystem: Deere remains the benchmark for the "Solutions as a Service" (SaaS) model. By deeply integrating hardware with its Operations Center™, it restricts ecosystem leakage and builds unprecedented customer stickiness, targeting a fully autonomous farming lifecycle by 2030.

2. The Brand-Agnostic Retrofit: AGCO is mounting a formidable challenge in the aftermarket space. Through its PTx brand, it is capturing the massive installed base of legacy machinery—regardless of the original manufacturer—by providing high-margin autonomous and precision retrofits, a highly resilient strategy during periods of depressed new-equipment CapEx.

HDIN Viewpoint

The ultimate battleground for the global agricultural machinery sector in 2026 will not be won by the manufacturer capable of engineering the heaviest iron, but by the entity that most efficiently transforms that iron into a digital terminal.

As the industry endures this L-shaped trough, HDIN Research assesses that survival and subsequent market outperformance will hinge on optimizing the conversion rate between legacy "cash cow" divisions and precision-ag "growth experiments." Investors and industry strategists must look past temporary sales volume dips and focus strictly on OEMs that are successfully migrating their business models from selling singular hardware units to monetizing verifiable, subscription-based agronomic outcomes.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Based on our comprehensive analysis of 2025 fiscal disclosures from industry leaders—including Deere & Company, CNH Industrial, AGCO, CLAAS, Kubota, Bucher Industries, and The Toro Company—HDIN Research has identified a critical shift in how global heavyweights are defending their margins. The strategic playbook has officially pivoted from aggressive capacity expansion to defensive capital preservation and structural technology acquisition.

Figure Global Agriculture Machinery 2025: Market Resilience & The Digital Paradigm Shift

Here is our strategic breakdown of the cyclical headwinds, capital allocation efficiencies, and financial risk radars shaping the industry through 2026.Cyclical Headwinds and the "L-Shaped" Trough

The operating environment for 2026 points toward an "L-shaped" stabilization rather than a rapid "V-shaped" recovery. The sector is currently battling a convergence of macroeconomic suppressors:

* The Squeeze on Farm Incomes: Sustained weakness in global crop prices (specifically wheat, corn, and soybeans) coupled with prolonged high interest rates has severely depressed farmer purchasing power.

* Supply Chain and Tariff Friction: Geopolitical fragmentation continues to inflate input ceilings. The shadow of retaliatory tariffs is eroding gross margins directly, with Deere alone facing an estimated $600 million direct tariff impact in 2025.

* The Destocking Dilemma: A severe channel destocking phase is the primary operational headwind. Historic highs in used equipment inventories are actively cannibalizing new machinery demand. Consequently, OEMs are forced to elevate sales incentive provisions to flush dealer channels, placing downward pressure on near-term profitability.

Capital Allocation Efficiency and Strategic Pivots

In response to top-line erosion, capital allocation logic among industry giants has diverged, highlighting distinct approaches to building strategic moats.

* Structural Transformation vs. Defensive Contraction: AGCO has exhibited aggressive portfolio restructuring, divesting its lower-margin Grain & Protein business to funnel capital directly into its PTx Trimble joint venture, prioritizing high-margin software and service revenues. Conversely, CNH Industrial has adopted a defensive posture, executing large-scale restructuring and workforce reductions to lower structural costs and repair its balance sheet amid a 33% plunge in North American high-horsepower tractor demand.

* The Counter-Cyclical Power of Diversification: Companies with robust non-agricultural portfolios demonstrated superior capital allocation efficiency. The Toro Company leveraged its highly profitable Professional Segment (driven by golf, landscaping, and underground construction) to offset agricultural weakness. Similarly, Kubota’s Water and Environment division provided a stable cash-flow buffer. These non-ag cash cows are not merely revenue diversifications; they serve as critical R&D funding mechanisms, allowing core technologies—like autonomous algorithms and hydraulic architectures—to be amortized across multiple industrial platforms.

Financial Risk Radar: Navigating Balance Sheet Vulnerabilities

As the market softens, HDIN Research advises stakeholders to look beyond top-line revenue and scrutinize asset quality. The current downcycle exposes several reporting vulnerabilities:

* Captive Finance and Residual Value Risks: As the prices of used agricultural machinery fall, the residual values of leased assets within OEM financial services divisions are highly susceptible to impairment. Furthermore, rising default rates in emerging markets, such as South America, demand close monitoring of whether OEMs are adequately provisioning for credit losses or delaying them to artificially sustain operating margins.

* The Commercial Reality of Tech Valuations: Over the past few years, OEMs acquired precision agriculture startups at massive premiums. The current tightening liquidity environment is forcing brutal commercial revaluations. CNH’s $172 million non-cash in-process R&D impairment related to Raven, and AGCO’s significant goodwill impairments for its tech units, signal that the commercialization of acquired autonomous technologies is facing friction.

* Cash Flow vs. Net Income Deviations: High-quality earnings are currently defined by cash conversion. Industry leaders like Deere and Toro have generated operating cash flows that significantly outpace net income by aggressively managing working capital and scaling back share repurchases to preserve liquidity.

Sector Positioning: The Race for Autonomous "Moats"

The hardware arms race is effectively over; the new competitive moat is forged in silicon, AI, and recurring software revenue. Regulatory pressures, such as California’s CARB zero-emission mandates and European Stage V emissions, are establishing a hard floor for compliance R&D, forcing OEMs to simultaneously fund green powertrains and autonomy.

Sector positioning is currently splitting into two distinct tech commercialization paths:

1. The "Full-Stack" Ecosystem: Deere remains the benchmark for the "Solutions as a Service" (SaaS) model. By deeply integrating hardware with its Operations Center™, it restricts ecosystem leakage and builds unprecedented customer stickiness, targeting a fully autonomous farming lifecycle by 2030.

2. The Brand-Agnostic Retrofit: AGCO is mounting a formidable challenge in the aftermarket space. Through its PTx brand, it is capturing the massive installed base of legacy machinery—regardless of the original manufacturer—by providing high-margin autonomous and precision retrofits, a highly resilient strategy during periods of depressed new-equipment CapEx.

HDIN Viewpoint

The ultimate battleground for the global agricultural machinery sector in 2026 will not be won by the manufacturer capable of engineering the heaviest iron, but by the entity that most efficiently transforms that iron into a digital terminal.

As the industry endures this L-shaped trough, HDIN Research assesses that survival and subsequent market outperformance will hinge on optimizing the conversion rate between legacy "cash cow" divisions and precision-ag "growth experiments." Investors and industry strategists must look past temporary sales volume dips and focus strictly on OEMs that are successfully migrating their business models from selling singular hardware units to monetizing verifiable, subscription-based agronomic outcomes.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com