Crimson Wine Group 2025: Navigating Cyclical Headwinds Through Strategic Mergers and Balance Sheet Optimization

Date : 2026-03-24

Reading : 99

Crimson Wine Group (CWG) utilized the 2025 fiscal year as a strategic "clearing period," absorbing cyclical headwinds and non-cash impairments to pave the way for leveraged, scale-driven growth. While macroeconomic pressures and distributor destocking drove an 11% contraction in net sales to $65.1 million, the company’s pristine capital allocation efficiency—highlighted by a pre-acquisition debt-to-equity ratio of just 8.2%—provided the crucial financial runway for its transformative $35.2 million acquisition of the Raeburn brand in early 2026.

Based on our internal financial deconstruction, HDIN Research identifies a distinct structural shift in CWG’s operational philosophy: transitioning from a purely "resource-controlled" model to a dynamic "brand-profitability" engine.

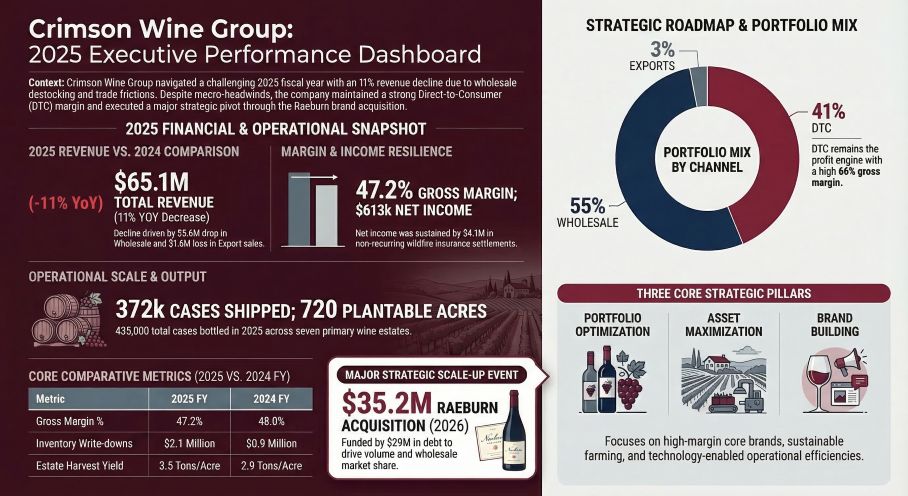

Figure Crimson Wine Group 2025: Executive Performance Dashboard

Financial Health: Absorbing Shocks with Capital Allocation Efficiency

Financial Health: Absorbing Shocks with Capital Allocation Efficiency

CWG’s 2025 profitability metrics reveal a dual narrative of external market friction and internal balance sheet fortification. The 14% decline in wholesale revenue was a direct symptom of broader industry inventory destocking and geopolitical trade frictions in the Canadian market.

To clear financial overhangs, management proactively recognized a $2.1 million inventory impairment and fully impaired $1.3 million in goodwill for the Seghesio and Seven Hills brands. While these non-cash write-downs resulted in a $3.7 million operating loss, the company’s core cash generation remained insulated. The underlying financial resilience is further evidenced by a conservative $15.4 million in total debt at year-end, ensuring that interest coverage remained highly manageable even in a restrictive monetary environment.

Sector Positioning: The DTC Moat vs. Wholesale Vulnerability

In a period defined by margin compression and inflation, CWG’s Direct-to-Consumer (DTC) channel emerged as its primary strategic moat. Representing 41% of total net sales, the DTC segment achieved a commanding 66% gross margin, effectively buffering the structural vulnerabilities of the wholesale channel (which operated at a 40% margin).

By leveraging its proprietary estate assets and expanding its e-commerce infrastructure—which notably achieved positive growth amidst industry contraction—CWG successfully executed a premiumization strategy. The ability to maintain an estimated average net price of $710 per case in the DTC channel demonstrates robust brand equity and a highly loyal consumer base, isolating the company from the pricing race-to-the-bottom seen in lower-tier wine segments.

Strategic Pivots: Capitalizing on M&A and Asset Optimization

Recognizing the limitations of organic growth within a stagnant macro environment, CWG is aggressively re-engineering its asset portfolio. The $35.2 million acquisition of the Raeburn brand in February 2026, funded through cash reserves and a $29 million revolving credit facility, marks a definitive pivot toward M&A-driven scale. This acquisition is designed to complement CWG's existing luxury matrix while injecting much-needed volume into its wholesale distribution network.

Simultaneously, the company is exercising strict financial discipline by divesting underperforming assets. The classification of the Washington-based Double Canyon estate as an "asset held for sale" (valued at $7.7 million) underscores management's commitment to shedding capital-intensive, low-yield operations to free up liquidity.

Industry Outlook: Climate Resilience and Demographic Shifts

The premium wine sector is currently grappling with profound structural shifts, from Gen Z's anti-alcohol awareness to the increasing frequency of extreme climate events. CWG’s 2025 financial results laid bare the agricultural realities of the industry: the company recorded a $1.1 million loss on vineyard asset disposals due to climate-induced productivity declines. Conversely, the bottom line was temporarily buoyed by $4.1 million in non-recurring insurance and legal settlements related to historical wildfires.

To mitigate future climate disruptions, CWG is treating Environmental, Social, and Governance (ESG) initiatives not merely as compliance, but as defensive operational strategy. Capital expenditures are increasingly being channeled into water resilience infrastructure and fire mitigation. Furthermore, to combat shifting demographic preferences, CWG is pivoting its product narrative toward sustainable farming and premium rosé categories to capture the evolving lifestyle demands of younger consumers.

HDIN Viewpoint

From an institutional perspective, HDIN Research issues a Neutral rating on Crimson Wine Group’s near-term outlook. The company boasts an enviable strategic moat through its 720 acres of prime viticultural land and high-margin DTC channels. However, the aggressive leveraging required for the Raeburn acquisition shifts the company's risk profile.

CWG has successfully "cleaned house" in 2025, but the true test lies in 2026. Investors and stakeholders must closely monitor the integration efficiency of the Raeburn asset and the company's ability to navigate emerging corporate governance hurdles, particularly the pending cybersecurity litigation. If management can successfully synthesize Raeburn’s volume with CWG's centralized operational framework, the company is well-positioned to emerge from the current industry trough with amplified market share and enhanced margin elasticity.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Based on our internal financial deconstruction, HDIN Research identifies a distinct structural shift in CWG’s operational philosophy: transitioning from a purely "resource-controlled" model to a dynamic "brand-profitability" engine.

Figure Crimson Wine Group 2025: Executive Performance Dashboard

Financial Health: Absorbing Shocks with Capital Allocation EfficiencyCWG’s 2025 profitability metrics reveal a dual narrative of external market friction and internal balance sheet fortification. The 14% decline in wholesale revenue was a direct symptom of broader industry inventory destocking and geopolitical trade frictions in the Canadian market.

To clear financial overhangs, management proactively recognized a $2.1 million inventory impairment and fully impaired $1.3 million in goodwill for the Seghesio and Seven Hills brands. While these non-cash write-downs resulted in a $3.7 million operating loss, the company’s core cash generation remained insulated. The underlying financial resilience is further evidenced by a conservative $15.4 million in total debt at year-end, ensuring that interest coverage remained highly manageable even in a restrictive monetary environment.

Sector Positioning: The DTC Moat vs. Wholesale Vulnerability

In a period defined by margin compression and inflation, CWG’s Direct-to-Consumer (DTC) channel emerged as its primary strategic moat. Representing 41% of total net sales, the DTC segment achieved a commanding 66% gross margin, effectively buffering the structural vulnerabilities of the wholesale channel (which operated at a 40% margin).

By leveraging its proprietary estate assets and expanding its e-commerce infrastructure—which notably achieved positive growth amidst industry contraction—CWG successfully executed a premiumization strategy. The ability to maintain an estimated average net price of $710 per case in the DTC channel demonstrates robust brand equity and a highly loyal consumer base, isolating the company from the pricing race-to-the-bottom seen in lower-tier wine segments.

Strategic Pivots: Capitalizing on M&A and Asset Optimization

Recognizing the limitations of organic growth within a stagnant macro environment, CWG is aggressively re-engineering its asset portfolio. The $35.2 million acquisition of the Raeburn brand in February 2026, funded through cash reserves and a $29 million revolving credit facility, marks a definitive pivot toward M&A-driven scale. This acquisition is designed to complement CWG's existing luxury matrix while injecting much-needed volume into its wholesale distribution network.

Simultaneously, the company is exercising strict financial discipline by divesting underperforming assets. The classification of the Washington-based Double Canyon estate as an "asset held for sale" (valued at $7.7 million) underscores management's commitment to shedding capital-intensive, low-yield operations to free up liquidity.

Industry Outlook: Climate Resilience and Demographic Shifts

The premium wine sector is currently grappling with profound structural shifts, from Gen Z's anti-alcohol awareness to the increasing frequency of extreme climate events. CWG’s 2025 financial results laid bare the agricultural realities of the industry: the company recorded a $1.1 million loss on vineyard asset disposals due to climate-induced productivity declines. Conversely, the bottom line was temporarily buoyed by $4.1 million in non-recurring insurance and legal settlements related to historical wildfires.

To mitigate future climate disruptions, CWG is treating Environmental, Social, and Governance (ESG) initiatives not merely as compliance, but as defensive operational strategy. Capital expenditures are increasingly being channeled into water resilience infrastructure and fire mitigation. Furthermore, to combat shifting demographic preferences, CWG is pivoting its product narrative toward sustainable farming and premium rosé categories to capture the evolving lifestyle demands of younger consumers.

HDIN Viewpoint

From an institutional perspective, HDIN Research issues a Neutral rating on Crimson Wine Group’s near-term outlook. The company boasts an enviable strategic moat through its 720 acres of prime viticultural land and high-margin DTC channels. However, the aggressive leveraging required for the Raeburn acquisition shifts the company's risk profile.

CWG has successfully "cleaned house" in 2025, but the true test lies in 2026. Investors and stakeholders must closely monitor the integration efficiency of the Raeburn asset and the company's ability to navigate emerging corporate governance hurdles, particularly the pending cybersecurity litigation. If management can successfully synthesize Raeburn’s volume with CWG's centralized operational framework, the company is well-positioned to emerge from the current industry trough with amplified market share and enhanced margin elasticity.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com