Bumble 2025 Strategic Pivot: Sacrificing Scale for Profitability in a Maturing Dating Market

Date : 2026-03-24

Reading : 83

For Bumble Inc., fiscal year 2025 marked a definitive inflection point, transitioning the company from a phase of aggressive user acquisition into a period of strategic retrenchment and profitability repair. An independent analysis by HDIN Research, based on Bumble’s 2025 Form 10-K, reveals a fundamental paradigm shift: management is actively trading top-line growth for bottom-line efficiency. By pivoting away from costly performance marketing toward organic brand growth and AI-driven engagement, Bumble successfully pushed its Adjusted EBITDA margins to a historic high, even as total revenue and user bases contracted.

Here is our deep-dive analysis into the strategic implications behind Bumble’s 2025 financial and operational restructuring.

Figure Bumble Inc 2025 Performance: Shifting to a High-Value Ecosystem

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

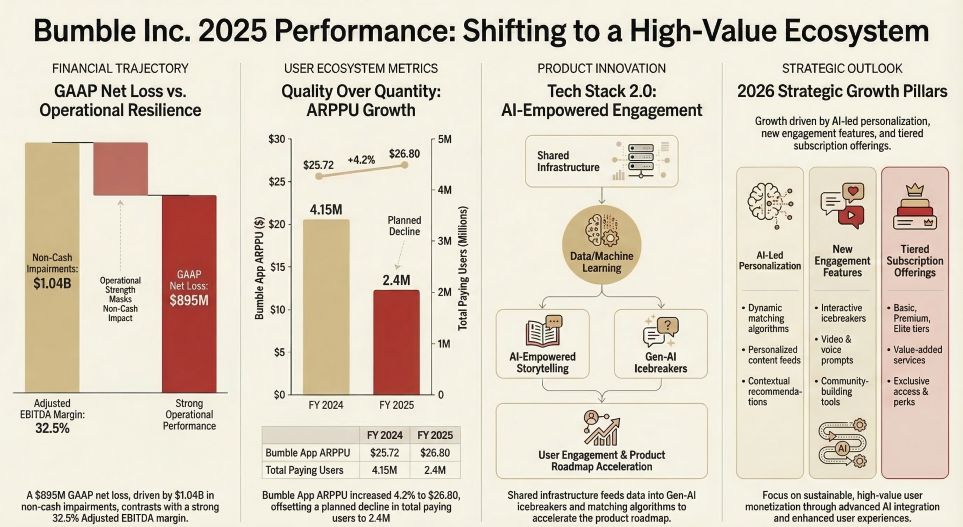

On the surface, Bumble’s 2025 income statement presents a stark contradiction: massive GAAP losses running parallel to record-breaking operational efficiency. Total revenue declined by 9.9% year-over-year to $966 million, driven primarily by an 11.5% drop in total paying users (down to 3.67 million). Furthermore, the company recorded a staggering GAAP net loss of $895 million.

However, looking through the lens of capital allocation efficiency, the narrative shifts. The GAAP loss was heavily distorted by a $1.039 billion non-cash impairment charge related to goodwill and intangible assets. This massive write-down signals a necessary financial clearing of historical M&A missteps—specifically, the aggressive acquisitions of the Fruitz and Official apps, which were divested and shuttered, respectively, in 2025.

Simultaneously, management executed a draconian cost-restructuring program, including a 30% global workforce reduction and a 36.7% slash in selling and marketing expenses. The "So What" factor here is profound: by purging low-LTV (Life-Time Value) users acquired through expensive paid channels, Bumble elevated its Adjusted EBITDA to $314 million, pushing margins from 28.4% in 2024 to a record 32.5%. Furthermore, Free Cash Flow (FCF) doubled to $239 million (a 76.1% FCF conversion rate), granting the company the liquidity to execute a $185.7 million buyout of its Tax Receivable Agreement (TRA)—effectively neutralizing a major historical liability.

Strategic Pivots: Endogenous Tech Over Exogenous Expansion

Bumble’s 2025 capital expenditure footprint highlights a deliberate shift from exogenous expansion toward endogenous technological moats. While physical CapEx shrank to just $11.68 million, product development and R&D expenses defied the broader cost-cutting trend, growing to $121.5 million.

This divergence in spending structure indicates that Bumble is going all-in on Artificial Intelligence as its primary operational lever. The strategic integration of generative AI is no longer a backend auxiliary function but a core frontend differentiator:

* Interaction Revolution: The rollout of "AI Icebreakers" utilizes generative AI to auto-generate context-aware opening lines based on user profiles, directly addressing the friction of initiating conversations.

* Industrialized Community Safety: Bumble became an industry pioneer in automated cyberflashing protection, utilizing machine learning algorithms to proactively blur explicit images and flag offensive messages in real-time. This fortifies its "Women-first" brand moat.

* Sector Expansion: Recognizing the cyclical headwind of "churn by design" in the dating sector (where successful matches result in lost subscribers), Bumble spun out its BFF (Bumble For Friends) platform into a standalone app. This marks a strategic push into the broader, less saturated non-romantic social networking space.

Sector Positioning and Cyclical Headwinds

Bumble operates in a sector currently battered by macroeconomic headwinds and platform monopolies. Global inflationary pressures have suppressed discretionary consumer spending, directly threatening subscription models. Additionally, the company remains heavily burdened by the 30% revenue-sharing fees imposed by the Apple and Google app stores, which act as a structural ceiling on profit margins.

Despite these cyclical headwinds, Bumble’s core sector positioning demonstrated remarkable resilience. While the Bumble App saw a 13.3% decline in paying users, its Average Revenue Per Paying User (ARPPU) actually grew by 4.2% to $26.80. This inverse relationship underscores the formidable pricing power of Bumble’s "Women-first" ecosystem. By maintaining a safer, highly curated community, the platform successfully retains a core demographic of high-net-worth users willing to absorb premium subscription pricing, even as fringe users churn out.

HDIN Viewpoint: The Perils of a Shrinking Core

From an institutional perspective, HDIN Research views Bumble’s 2025 transformation with cautious optimism laced with significant strategic skepticism. The realization of a 32.5% Adjusted EBITDA margin is commendable, but the underlying mechanics—slashing marketing budgets by nearly 37% in an inherently high-churn industry—carry immense long-term risk.

In a hyper-competitive landscape dominated by Match Group and encroaching free alternatives like Facebook Dating, organic brand growth alone may not be sufficient to replenish the top of the funnel. If Bumble fails to stabilize its double-digit decline in paying users by 2026, the current margin expansion will ultimately be exposed as a "false prosperity" built on a shrinking operational footprint.

Furthermore, investors must remain vigilant regarding the company’s corporate governance structure. Bumble remains a "controlled company," with Blackstone and the Founder holding 86.5% of the voting power despite controlling only 14.1% of the economic interest. This dual-class structure severely limits the ability of public shareholders to influence the trajectory of this high-stakes strategic pivot. Moving forward, Bumble’s valuation will hinge not on further cost extractions, but on whether its AI investments and BFF market penetration can successfully ignite a sustainable, organic second curve of growth.

Presentation download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Here is our deep-dive analysis into the strategic implications behind Bumble’s 2025 financial and operational restructuring.

Figure Bumble Inc 2025 Performance: Shifting to a High-Value Ecosystem

Financial Health & Capital Allocation EfficiencyOn the surface, Bumble’s 2025 income statement presents a stark contradiction: massive GAAP losses running parallel to record-breaking operational efficiency. Total revenue declined by 9.9% year-over-year to $966 million, driven primarily by an 11.5% drop in total paying users (down to 3.67 million). Furthermore, the company recorded a staggering GAAP net loss of $895 million.

However, looking through the lens of capital allocation efficiency, the narrative shifts. The GAAP loss was heavily distorted by a $1.039 billion non-cash impairment charge related to goodwill and intangible assets. This massive write-down signals a necessary financial clearing of historical M&A missteps—specifically, the aggressive acquisitions of the Fruitz and Official apps, which were divested and shuttered, respectively, in 2025.

Simultaneously, management executed a draconian cost-restructuring program, including a 30% global workforce reduction and a 36.7% slash in selling and marketing expenses. The "So What" factor here is profound: by purging low-LTV (Life-Time Value) users acquired through expensive paid channels, Bumble elevated its Adjusted EBITDA to $314 million, pushing margins from 28.4% in 2024 to a record 32.5%. Furthermore, Free Cash Flow (FCF) doubled to $239 million (a 76.1% FCF conversion rate), granting the company the liquidity to execute a $185.7 million buyout of its Tax Receivable Agreement (TRA)—effectively neutralizing a major historical liability.

Strategic Pivots: Endogenous Tech Over Exogenous Expansion

Bumble’s 2025 capital expenditure footprint highlights a deliberate shift from exogenous expansion toward endogenous technological moats. While physical CapEx shrank to just $11.68 million, product development and R&D expenses defied the broader cost-cutting trend, growing to $121.5 million.

This divergence in spending structure indicates that Bumble is going all-in on Artificial Intelligence as its primary operational lever. The strategic integration of generative AI is no longer a backend auxiliary function but a core frontend differentiator:

* Interaction Revolution: The rollout of "AI Icebreakers" utilizes generative AI to auto-generate context-aware opening lines based on user profiles, directly addressing the friction of initiating conversations.

* Industrialized Community Safety: Bumble became an industry pioneer in automated cyberflashing protection, utilizing machine learning algorithms to proactively blur explicit images and flag offensive messages in real-time. This fortifies its "Women-first" brand moat.

* Sector Expansion: Recognizing the cyclical headwind of "churn by design" in the dating sector (where successful matches result in lost subscribers), Bumble spun out its BFF (Bumble For Friends) platform into a standalone app. This marks a strategic push into the broader, less saturated non-romantic social networking space.

Sector Positioning and Cyclical Headwinds

Bumble operates in a sector currently battered by macroeconomic headwinds and platform monopolies. Global inflationary pressures have suppressed discretionary consumer spending, directly threatening subscription models. Additionally, the company remains heavily burdened by the 30% revenue-sharing fees imposed by the Apple and Google app stores, which act as a structural ceiling on profit margins.

Despite these cyclical headwinds, Bumble’s core sector positioning demonstrated remarkable resilience. While the Bumble App saw a 13.3% decline in paying users, its Average Revenue Per Paying User (ARPPU) actually grew by 4.2% to $26.80. This inverse relationship underscores the formidable pricing power of Bumble’s "Women-first" ecosystem. By maintaining a safer, highly curated community, the platform successfully retains a core demographic of high-net-worth users willing to absorb premium subscription pricing, even as fringe users churn out.

HDIN Viewpoint: The Perils of a Shrinking Core

From an institutional perspective, HDIN Research views Bumble’s 2025 transformation with cautious optimism laced with significant strategic skepticism. The realization of a 32.5% Adjusted EBITDA margin is commendable, but the underlying mechanics—slashing marketing budgets by nearly 37% in an inherently high-churn industry—carry immense long-term risk.

In a hyper-competitive landscape dominated by Match Group and encroaching free alternatives like Facebook Dating, organic brand growth alone may not be sufficient to replenish the top of the funnel. If Bumble fails to stabilize its double-digit decline in paying users by 2026, the current margin expansion will ultimately be exposed as a "false prosperity" built on a shrinking operational footprint.

Furthermore, investors must remain vigilant regarding the company’s corporate governance structure. Bumble remains a "controlled company," with Blackstone and the Founder holding 86.5% of the voting power despite controlling only 14.1% of the economic interest. This dual-class structure severely limits the ability of public shareholders to influence the trajectory of this high-stakes strategic pivot. Moving forward, Bumble’s valuation will hinge not on further cost extractions, but on whether its AI investments and BFF market penetration can successfully ignite a sustainable, organic second curve of growth.

Presentation download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com