2025 Global Advanced Wound Care Market: Navigating Structural Expansion and Policy-Driven Price Resets

Date : 2026-03-23

Reading : 189

The global Advanced Wound Care (AWC) industry is currently operating at the critical intersection of structural demand expansion and cyclical headwinds. Valued at approximately $13.1 billion and growing at a steady 4% annually, the market is being propelled by undeniable demographic shifts, including a global aging population projected to reach 1.9 billion by 2060.

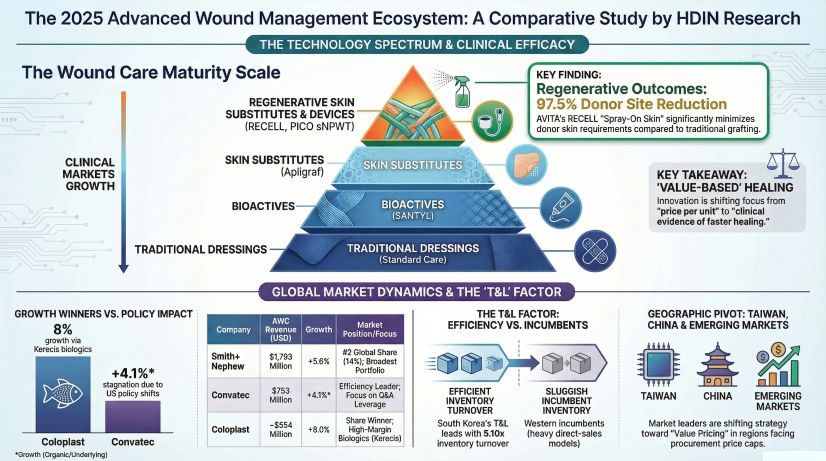

However, beneath this macroeconomic tailwind lies a rapidly shifting regulatory landscape. Based on an exhaustive financial and operational analysis of seven leading players—including Smith & Nephew, Convatec, Coloplast, Organogenesis, Vericel, Avita Medical, and T&L—HDIN Research has identified a fundamental sector repositioning. Profitability in 2025 is no longer driven by sheer volume or legacy channel dominance; it is dictated by capital allocation efficiency, clinical evidence, and the ability to navigate stringent policy ceilings.

Figure The 2025 Advanced Wound Management Ecosystem: A Comparative Study

Strategic Pivots: The Great Migration to Home Care and Biologics

Strategic Pivots: The Great Migration to Home Care and Biologics

A structural migration is underway, shifting the nexus of wound care from the hospital operating room to ambulatory surgery centers (ASCs) and home care settings. This transition is not merely logistical; it represents a strategic moat for companies that can secure patient adherence post-discharge.

* Dominating the Chronic Care Channel: Coloplast has successfully entrenched itself in the community and home setting through its "Chronic Care" model, where over 90% of its sales occur post-discharge. Similarly, Convatec is leveraging its direct-to-patient networks (Home Services Group and 180 Medical) to capture high-margin recurring revenue.

* The Biologics Substitution Effect: The technology paradigm is shifting from traditional physical barriers (foams and alginates) to biological regeneration. The biologics segment is compounding at 6% to 8% annually, vastly outperforming traditional dressings. Coloplast’s strategic acquisition of the Kerecis fish-skin technology yielded a remarkable 24% organic growth in its biologics division in 2025. Meanwhile, Smith & Nephew continues to balance its portfolio, generating $621 million from advanced wound bioactives.

Cyclical Headwinds: Navigating the CMS and VBP Policy Ceilings

While demand metrics are robust, the industry faces severe policy headwinds that are aggressively compressing margins for ill-prepared portfolios.

* The US CMS Reimbursement Shock: The U.S. Centers for Medicare & Medicaid Services (CMS) has fundamentally restructured the economics of skin substitutes by transitioning to a fixed-payment model (approximately $127.14/cm² for 2026). The financial fallout is already visible: Convatec was forced to take a $72 million impairment charge on its InnovaMatrix asset due to plummeting sales. Organogenesis, highly exposed to this segment, is exhibiting severe liquidity warning signs—while reporting positive net income, its operating cash flow turned negative, and accounts receivable spiked by 98%, signaling a dangerous reliance on channel stuffing amid reimbursement uncertainties.

* China’s Volume-Based Procurement (VBP): In the Greater China market (inclusive of operations in Taiwan), VBP initiatives are exerting immense pricing pressure. Giants like Smith & Nephew and Coloplast are pivoting from premium pricing models to "value-based pricing," emphasizing clinical data that proves their products reduce hospital length of stay (LOS) and overall consumable usage to protect their market share.

Capital Allocation Efficiency and Financial Health

A deep dive into the balance sheets reveals a stark bifurcation in supply chain resilience and capital efficiency:

* The Lean Manufacturer: South Korea’s T&L exemplifies peak operational efficiency with an exceptional inventory turnover rate of 5.10x and a remarkably low SG&A ratio of 15.9%. However, as an ODM provider, it remains vulnerable to downstream margin compression passing through from global brand partners.

* The Cash Cow with Legacy Weight: Smith & Nephew stands as a bastion of financial defense, generating a robust $840 million in free cash flow, allowing it to easily fund innovation and return capital to shareholders. Yet, it continues to battle a bloated supply chain, evidenced by a massive 475-day inventory turnover and a $159 million inventory obsolescence charge, highlighting the friction of its ongoing operational restructuring.

* The High-Wire Act: Coloplast delivers an industry-leading EBIT margin of 32.1% in its wound care division but carries structural vulnerability, with goodwill exceeding 121% of its total equity following its aggressive M&A streak. Convatec, while boasting best-in-class administrative cost leverage (G&A down to 6.8%), is currently exhibiting an aggressive capital allocation strategy where shareholder payouts outstrip free cash flow, a potential risk in a high-interest environment.

HDIN Viewpoint: Sector Positioning in a Post-Reform Era

From an institutional perspective, HDIN Research concludes that the era of competing solely on distribution leverage in the Advanced Wound Care sector is definitively over. As CMS price caps and VBP frameworks commoditize legacy products, the ultimate strategic moat is now Clinical Evidence.

Companies that can scientifically prove economic value—such as Avita Medical demonstrating a 36% (5.6 days) reduction in hospital stays utilizing its RECELL system, or Smith & Nephew integrating digital tracking via its LEAF patient monitoring system—will command valuation premiums. Furthermore, players like Vericel and Organogenesis that proactively pursue rigorous Biologics License Application (BLA) pathways are trading short-term R&D burn for long-term pricing immunity. Moving forward, the AWC market will reward those who pair unassailable clinical data with lean, automated manufacturing infrastructures.

Presentation Download & Media Access

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

However, beneath this macroeconomic tailwind lies a rapidly shifting regulatory landscape. Based on an exhaustive financial and operational analysis of seven leading players—including Smith & Nephew, Convatec, Coloplast, Organogenesis, Vericel, Avita Medical, and T&L—HDIN Research has identified a fundamental sector repositioning. Profitability in 2025 is no longer driven by sheer volume or legacy channel dominance; it is dictated by capital allocation efficiency, clinical evidence, and the ability to navigate stringent policy ceilings.

Figure The 2025 Advanced Wound Management Ecosystem: A Comparative Study

Strategic Pivots: The Great Migration to Home Care and BiologicsA structural migration is underway, shifting the nexus of wound care from the hospital operating room to ambulatory surgery centers (ASCs) and home care settings. This transition is not merely logistical; it represents a strategic moat for companies that can secure patient adherence post-discharge.

* Dominating the Chronic Care Channel: Coloplast has successfully entrenched itself in the community and home setting through its "Chronic Care" model, where over 90% of its sales occur post-discharge. Similarly, Convatec is leveraging its direct-to-patient networks (Home Services Group and 180 Medical) to capture high-margin recurring revenue.

* The Biologics Substitution Effect: The technology paradigm is shifting from traditional physical barriers (foams and alginates) to biological regeneration. The biologics segment is compounding at 6% to 8% annually, vastly outperforming traditional dressings. Coloplast’s strategic acquisition of the Kerecis fish-skin technology yielded a remarkable 24% organic growth in its biologics division in 2025. Meanwhile, Smith & Nephew continues to balance its portfolio, generating $621 million from advanced wound bioactives.

Cyclical Headwinds: Navigating the CMS and VBP Policy Ceilings

While demand metrics are robust, the industry faces severe policy headwinds that are aggressively compressing margins for ill-prepared portfolios.

* The US CMS Reimbursement Shock: The U.S. Centers for Medicare & Medicaid Services (CMS) has fundamentally restructured the economics of skin substitutes by transitioning to a fixed-payment model (approximately $127.14/cm² for 2026). The financial fallout is already visible: Convatec was forced to take a $72 million impairment charge on its InnovaMatrix asset due to plummeting sales. Organogenesis, highly exposed to this segment, is exhibiting severe liquidity warning signs—while reporting positive net income, its operating cash flow turned negative, and accounts receivable spiked by 98%, signaling a dangerous reliance on channel stuffing amid reimbursement uncertainties.

* China’s Volume-Based Procurement (VBP): In the Greater China market (inclusive of operations in Taiwan), VBP initiatives are exerting immense pricing pressure. Giants like Smith & Nephew and Coloplast are pivoting from premium pricing models to "value-based pricing," emphasizing clinical data that proves their products reduce hospital length of stay (LOS) and overall consumable usage to protect their market share.

Capital Allocation Efficiency and Financial Health

A deep dive into the balance sheets reveals a stark bifurcation in supply chain resilience and capital efficiency:

* The Lean Manufacturer: South Korea’s T&L exemplifies peak operational efficiency with an exceptional inventory turnover rate of 5.10x and a remarkably low SG&A ratio of 15.9%. However, as an ODM provider, it remains vulnerable to downstream margin compression passing through from global brand partners.

* The Cash Cow with Legacy Weight: Smith & Nephew stands as a bastion of financial defense, generating a robust $840 million in free cash flow, allowing it to easily fund innovation and return capital to shareholders. Yet, it continues to battle a bloated supply chain, evidenced by a massive 475-day inventory turnover and a $159 million inventory obsolescence charge, highlighting the friction of its ongoing operational restructuring.

* The High-Wire Act: Coloplast delivers an industry-leading EBIT margin of 32.1% in its wound care division but carries structural vulnerability, with goodwill exceeding 121% of its total equity following its aggressive M&A streak. Convatec, while boasting best-in-class administrative cost leverage (G&A down to 6.8%), is currently exhibiting an aggressive capital allocation strategy where shareholder payouts outstrip free cash flow, a potential risk in a high-interest environment.

HDIN Viewpoint: Sector Positioning in a Post-Reform Era

From an institutional perspective, HDIN Research concludes that the era of competing solely on distribution leverage in the Advanced Wound Care sector is definitively over. As CMS price caps and VBP frameworks commoditize legacy products, the ultimate strategic moat is now Clinical Evidence.

Companies that can scientifically prove economic value—such as Avita Medical demonstrating a 36% (5.6 days) reduction in hospital stays utilizing its RECELL system, or Smith & Nephew integrating digital tracking via its LEAF patient monitoring system—will command valuation premiums. Furthermore, players like Vericel and Organogenesis that proactively pursue rigorous Biologics License Application (BLA) pathways are trading short-term R&D burn for long-term pricing immunity. Moving forward, the AWC market will reward those who pair unassailable clinical data with lean, automated manufacturing infrastructures.

Presentation Download & Media Access

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com