Demant vs. GN Store Nord 2025: Strategic Moats, Capital Allocation, and the AI Edge in Hearing Healthcare

Date : 2026-03-23

Reading : 399

In 2025, the global hearing healthcare sector faced intersecting macroeconomic headwinds and rapid technological shifts. HDIN Research’s latest comparative analysis of industry giants Demant and GN Store Nord (GN) reveals a profound strategic divergence. While both companies navigate cyclical pressures and supply chain volatility, their distinct approaches to capital allocation, artificial intelligence (AI) integration, and channel management are redefining the sector's strategic moats.

Rather than merely competing on product features, Demant and GN are playing fundamentally different games: one is building an impenetrable vertical healthcare fortress, while the other is pioneering a cross-ecosystem, AI-driven audio network.

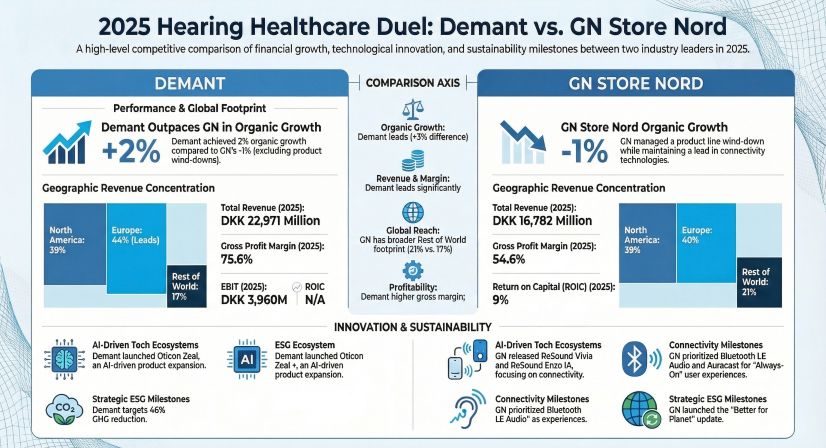

Figure 2025 Hearing Healthcare Duel: Demant vs. GN Store Nord

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

The 2025 financial data underscores two radically different business models, highlighting a trade-off between margin defense and operational agility.

* Demant’s Vertical Dominance: Demant reported total revenue of DKK 22,971 million (+2.5% organic growth), boasting a stellar gross margin of 75.6%. This margin superiority is driven by its massive retail footprint (Hearing Care), which accounts for 47% of its revenue. However, this vertical integration creates a highly labor-intensive structure; human resource costs consume 43.8% of Demant’s revenue. From a capital allocation perspective, Demant relies heavily on M&A, utilizing a DKK 6.28 billion capital expenditure primarily to acquire the KIND clinic network. This aggressive expansion pushed its gearing multiple to 3.4x, significantly above its target range, elevating its goodwill impairment risks.

* GN’s Asset-Light Agility: Conversely, GN reported DKK 16,782 million in revenue, experiencing a 6.7% contraction primarily due to cyclical headwinds in its Enterprise and Gaming divisions. Despite a lower gross margin of 54.6%, GN operates a highly efficient, labor-light model, with HR costs at just 25.5% of revenue and an impressive revenue-per-FTE of DKK 2.29 million (more than double Demant’s). GN prioritized deleveraging in 2025, successfully refinancing its debt and utilizing a non-competitive, partnership-based distribution model after divesting its proprietary retail assets in 2024.

The "So What" Factor: Demant is trading operational agility and balance sheet flexibility for ultimate control over the end-user clinical journey. GN, meanwhile, is absorbing short-term macroeconomic volatility in consumer tech to maintain a lean, highly scalable enterprise structure.

Supply Chain Resilience and Working Capital

A deeper look at working capital metrics reveals contrasting operational strengths in response to 2025's global tariff threats and macro uncertainties.

* GN demonstrated superior physical supply chain fluidity, achieving an inventory turnover rate of 2.51x compared to Demant's 1.51x. To proactively hedge against impending US tariffs and supply chain bottlenecks, GN executed a highly agile relocation of 31 production lines across multiple countries.

* However, Demant exhibits absolute dominance in channel credit management. Demant's Days Sales Outstanding (DSO) stands at a rapid 59.8 days, whereas GN's DSO lags at 95.3 days.

The "So What" Factor: GN’s supply chain is optimized for hardware velocity, which is critical for its consumer and enterprise tech portfolios. Demant’s rapid cash conversion cycle reflects the pricing power and direct-to-consumer leverage it commands through its proprietary audiology networks and diagnostic equipment lock-ins.

Technological Moats: AI and Ecosystem Positioning

Both companies are aggressively investing in AI, Bluetooth® LE Audio, and Auracast™ standardization, but their R&D philosophies highlight divergent technological endgames. GN’s total R&D intensity reached an aggressive 11.1% of revenue, compared to Demant’s 6.1%.

* Demant (Clinical Precision): With the launch of the *Oticon Zeal*, Demant utilizes Deep Neural Networks (DNN) to master "sound scene understanding." The strategic goal is purely clinical: using AI to lower the barrier to entry for first-time users by automating complex acoustic adjustments, thereby driving early-stage market penetration.

* GN (Behavioral Simulation & Ecosystems): GN’s technological vision is more expansive. Its *ReSound Vivia* introduces "Intelligent Focus," an AI model that simulates human behavior by prioritizing sound based on where the user is looking, rather than just volume. Furthermore, GN leverages significant R&D spillover from its Jabra (Enterprise) and SteelSeries (Gaming) divisions. GN's ultimate vision is to transform the hearing aid into a GenAI gateway—an edge-computing terminal capable of local AI inference and seamless integration with broader digital workspaces.

HDIN Viewpoint: Sector Positioning and the Path Forward

From the perspective of HDIN Research, the 2025 performance of Demant and GN perfectly illustrates the bifurcation of the hearing technology market.

Demant represents the ultimate "Defensive Healthcare Play." By controlling the entire patient journey—from Diagnostics (high barrier to entry) to Hearing Aids (wholesale) and Hearing Care (retail)—Demant insulates itself from consumer electronics cycles. Its primary risk lies in balance sheet execution: it must rapidly deleverage and successfully integrate the KIND acquisition to justify its nearly 50% goodwill asset ratio.

GN represents the "Hybrid Tech-Medical Play." While currently penalized by cyclical headwinds in enterprise IT budgets and consumer gaming, GN possesses a highly scalable, cross-disciplinary audio infrastructure. By remaining asset-light and focusing heavily on GenAI and LE Audio, GN is best positioned if the industry accelerates its transition from traditional medical devices to integrated, smart wearable ecosystems.

Ultimately, the industry's secular growth—driven by global aging demographics—remains robust. The winner of the next decade will be determined by whether the market values clinical retail monopolization or open-ecosystem technological interoperability.

Presentation Download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Rather than merely competing on product features, Demant and GN are playing fundamentally different games: one is building an impenetrable vertical healthcare fortress, while the other is pioneering a cross-ecosystem, AI-driven audio network.

Figure 2025 Hearing Healthcare Duel: Demant vs. GN Store Nord

Financial Health & Capital Allocation EfficiencyThe 2025 financial data underscores two radically different business models, highlighting a trade-off between margin defense and operational agility.

* Demant’s Vertical Dominance: Demant reported total revenue of DKK 22,971 million (+2.5% organic growth), boasting a stellar gross margin of 75.6%. This margin superiority is driven by its massive retail footprint (Hearing Care), which accounts for 47% of its revenue. However, this vertical integration creates a highly labor-intensive structure; human resource costs consume 43.8% of Demant’s revenue. From a capital allocation perspective, Demant relies heavily on M&A, utilizing a DKK 6.28 billion capital expenditure primarily to acquire the KIND clinic network. This aggressive expansion pushed its gearing multiple to 3.4x, significantly above its target range, elevating its goodwill impairment risks.

* GN’s Asset-Light Agility: Conversely, GN reported DKK 16,782 million in revenue, experiencing a 6.7% contraction primarily due to cyclical headwinds in its Enterprise and Gaming divisions. Despite a lower gross margin of 54.6%, GN operates a highly efficient, labor-light model, with HR costs at just 25.5% of revenue and an impressive revenue-per-FTE of DKK 2.29 million (more than double Demant’s). GN prioritized deleveraging in 2025, successfully refinancing its debt and utilizing a non-competitive, partnership-based distribution model after divesting its proprietary retail assets in 2024.

The "So What" Factor: Demant is trading operational agility and balance sheet flexibility for ultimate control over the end-user clinical journey. GN, meanwhile, is absorbing short-term macroeconomic volatility in consumer tech to maintain a lean, highly scalable enterprise structure.

Supply Chain Resilience and Working Capital

A deeper look at working capital metrics reveals contrasting operational strengths in response to 2025's global tariff threats and macro uncertainties.

* GN demonstrated superior physical supply chain fluidity, achieving an inventory turnover rate of 2.51x compared to Demant's 1.51x. To proactively hedge against impending US tariffs and supply chain bottlenecks, GN executed a highly agile relocation of 31 production lines across multiple countries.

* However, Demant exhibits absolute dominance in channel credit management. Demant's Days Sales Outstanding (DSO) stands at a rapid 59.8 days, whereas GN's DSO lags at 95.3 days.

The "So What" Factor: GN’s supply chain is optimized for hardware velocity, which is critical for its consumer and enterprise tech portfolios. Demant’s rapid cash conversion cycle reflects the pricing power and direct-to-consumer leverage it commands through its proprietary audiology networks and diagnostic equipment lock-ins.

Technological Moats: AI and Ecosystem Positioning

Both companies are aggressively investing in AI, Bluetooth® LE Audio, and Auracast™ standardization, but their R&D philosophies highlight divergent technological endgames. GN’s total R&D intensity reached an aggressive 11.1% of revenue, compared to Demant’s 6.1%.

* Demant (Clinical Precision): With the launch of the *Oticon Zeal*, Demant utilizes Deep Neural Networks (DNN) to master "sound scene understanding." The strategic goal is purely clinical: using AI to lower the barrier to entry for first-time users by automating complex acoustic adjustments, thereby driving early-stage market penetration.

* GN (Behavioral Simulation & Ecosystems): GN’s technological vision is more expansive. Its *ReSound Vivia* introduces "Intelligent Focus," an AI model that simulates human behavior by prioritizing sound based on where the user is looking, rather than just volume. Furthermore, GN leverages significant R&D spillover from its Jabra (Enterprise) and SteelSeries (Gaming) divisions. GN's ultimate vision is to transform the hearing aid into a GenAI gateway—an edge-computing terminal capable of local AI inference and seamless integration with broader digital workspaces.

HDIN Viewpoint: Sector Positioning and the Path Forward

From the perspective of HDIN Research, the 2025 performance of Demant and GN perfectly illustrates the bifurcation of the hearing technology market.

Demant represents the ultimate "Defensive Healthcare Play." By controlling the entire patient journey—from Diagnostics (high barrier to entry) to Hearing Aids (wholesale) and Hearing Care (retail)—Demant insulates itself from consumer electronics cycles. Its primary risk lies in balance sheet execution: it must rapidly deleverage and successfully integrate the KIND acquisition to justify its nearly 50% goodwill asset ratio.

GN represents the "Hybrid Tech-Medical Play." While currently penalized by cyclical headwinds in enterprise IT budgets and consumer gaming, GN possesses a highly scalable, cross-disciplinary audio infrastructure. By remaining asset-light and focusing heavily on GenAI and LE Audio, GN is best positioned if the industry accelerates its transition from traditional medical devices to integrated, smart wearable ecosystems.

Ultimately, the industry's secular growth—driven by global aging demographics—remains robust. The winner of the next decade will be determined by whether the market values clinical retail monopolization or open-ecosystem technological interoperability.

Presentation Download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com