MedTech Moats: A Strategic Financial Analysis of IceCure Medical and Sensus Healthcare in 2025

Date : 2026-03-23

Reading : 137

In the rapidly evolving landscape of minimally invasive oncology and dermatological radiotherapy, technology alone does not guarantee commercial survival. A comparative analysis of the 2025 annual reports for IceCure Medical (ICCM) and Sensus Healthcare (SRTS) reveals a stark divergence in sector positioning. While Sensus demonstrates superior capital allocation efficiency and defensive cash flow resilience, IceCure possesses highly disruptive, FDA-validated technology but is currently navigating severe liquidity headwinds. For institutional investors, the narrative is clear: Sensus is capitalizing on a transition to recurring revenue, whereas IceCure is racing against a ticking financial clock to commercialize its breakthrough breast cancer ablation platform.

Figure 2025 Fiscal Face-Off: lceCure Medical vs Sensus Healthcare

Capital Allocation Efficiency and Financial Health

Capital Allocation Efficiency and Financial Health

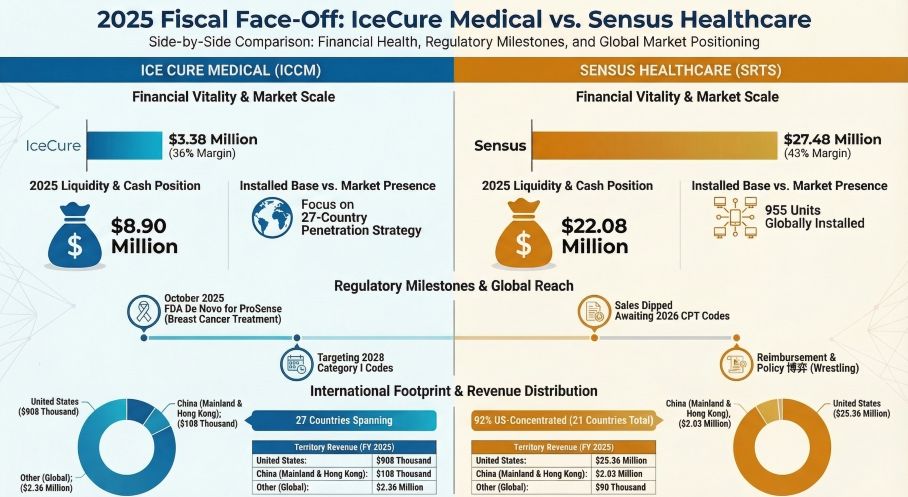

The 2025 financial metrics highlight a massive gulf in operational maturity between the two entities. Sensus generated $27.48 million in revenue—approximately 8.1 times that of IceCure ($3.38 million). More critically, Sensus achieved a per-capita organizational output of $458,033, dwarfing IceCure’s $48,971.

The "So What" factor here lies in the quality of earnings and balance sheet fortitude. Although Sensus reported a nominal net loss, its robust accounts receivable recovery ($13.65 million) translated into positive operating cash flow of $0.53 million. With $22.08 million in cash equivalents, a debt-to-asset ratio of just 9.3%, and zero drawn bank borrowings, Sensus exhibits a highly resilient financial structure. Conversely, IceCure is battling an existential crisis. Driven by heavy R&D expenditures to secure regulatory access, IceCure burned through $14.57 million in operating cash, triggering a formal "going concern" warning as its cash reserves dwindled to $4.7 million by early 2026.

Strategic Moats: The "Razor and Blade" Evolution

Both companies are fiercely engineering high-switching-cost business models, but they are executing at different stages of the commercial lifecycle.

IceCure has successfully established a pure "razor-and-blade" matrix, with high-margin cryoprobe consumables and services accounting for 61% of its revenue. While this structural mix validates strong long-term customer stickiness, the current low revenue base cannot absorb the company’s intensive R&D and market education costs.

Sensus, historically reliant on one-off capital equipment sales (SRT-100 systems), is aggressively pivoting to a service-oriented recurring revenue model. By leveraging its "Fair Deal Agreement," Sensus effectively lowers the upfront procurement barrier for dermatology clinics through revenue-sharing mechanics. This strategic pivot shifts the company from pure equipment vendor to embedded clinical partner, securing long-term operational leverage. Furthermore, both firms are investing heavily in multi-probe capabilities and cloud digitization (e.g., Sensus Link) to capture complex clinical workflows and deepen their competitive moats.

Cyclical Headwinds and Regulatory Roadblocks

The MedTech industry's growth ceiling is ultimately dictated by reimbursement policies, and both companies are currently caught in the crosshairs of payer dynamics.

Sensus experienced a sharp 34.3% YoY revenue contraction in 2025. This was not a failure of clinical demand, but rather a classic cyclical headwind: clinics delayed procurement in anticipation of new CMS CPT reimbursement codes taking effect in January 2026. This exposes the company's vulnerability to policy-driven purchasing pauses. Furthermore, Sensus faces concentration risk, with 92.3% of its revenue derived from North America and 52% from a single client.

IceCure faces a different reimbursement hurdle: the "coding transition chasm." Although its ProSense system achieved a monumental FDA De Novo classification for early-stage breast cancer and inclusion in the ASBrS clinical guidelines, it currently relies on a temporary Category III CPT code. The arduous wait for a permanent Category I code (expected around 2028) severely restricts immediate institutional adoption. Additionally, as an Israel-based entity, IceCure’s supply chain is highly sensitive to Middle Eastern geopolitical volatility and strict domestic IP transfer regulations. Globally, both companies must also navigate margin-compression risks in crucial overseas markets like China, driven by the expanding scope of Volume-Based Procurement (VBP) policies.

HDIN Viewpoint: Sector Positioning

From the perspective of HDIN Research, these two equities offer completely asymmetric risk-reward profiles. Sensus Healthcare is a defensive play. The company is actively utilizing its pristine balance sheet to weather temporary reimbursement volatility and transition into a higher-margin, asset-light service model. The primary metric to watch is the velocity of its order book rebound following the implementation of the 2026 CPT codes, alongside careful monitoring of its rising inventory levels.

IceCure Medical, conversely, is a high-risk, high-reward commercialization play. The clinical validation of its liquid nitrogen (LN2) cryoablation technology is unassailable, offering a true minimally invasive alternative to lumpectomies. However, the company's financial risk is flashing red. Its survival—and the realization of its underlying asset value—hinges entirely on its ability to secure non-dilutive bridge financing or strategic partnerships before its liquidity dries up. For IceCure, market access has been won; the battle for capital survival has just begun.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Fiscal Face-Off: lceCure Medical vs Sensus Healthcare

Capital Allocation Efficiency and Financial HealthThe 2025 financial metrics highlight a massive gulf in operational maturity between the two entities. Sensus generated $27.48 million in revenue—approximately 8.1 times that of IceCure ($3.38 million). More critically, Sensus achieved a per-capita organizational output of $458,033, dwarfing IceCure’s $48,971.

The "So What" factor here lies in the quality of earnings and balance sheet fortitude. Although Sensus reported a nominal net loss, its robust accounts receivable recovery ($13.65 million) translated into positive operating cash flow of $0.53 million. With $22.08 million in cash equivalents, a debt-to-asset ratio of just 9.3%, and zero drawn bank borrowings, Sensus exhibits a highly resilient financial structure. Conversely, IceCure is battling an existential crisis. Driven by heavy R&D expenditures to secure regulatory access, IceCure burned through $14.57 million in operating cash, triggering a formal "going concern" warning as its cash reserves dwindled to $4.7 million by early 2026.

Strategic Moats: The "Razor and Blade" Evolution

Both companies are fiercely engineering high-switching-cost business models, but they are executing at different stages of the commercial lifecycle.

IceCure has successfully established a pure "razor-and-blade" matrix, with high-margin cryoprobe consumables and services accounting for 61% of its revenue. While this structural mix validates strong long-term customer stickiness, the current low revenue base cannot absorb the company’s intensive R&D and market education costs.

Sensus, historically reliant on one-off capital equipment sales (SRT-100 systems), is aggressively pivoting to a service-oriented recurring revenue model. By leveraging its "Fair Deal Agreement," Sensus effectively lowers the upfront procurement barrier for dermatology clinics through revenue-sharing mechanics. This strategic pivot shifts the company from pure equipment vendor to embedded clinical partner, securing long-term operational leverage. Furthermore, both firms are investing heavily in multi-probe capabilities and cloud digitization (e.g., Sensus Link) to capture complex clinical workflows and deepen their competitive moats.

Cyclical Headwinds and Regulatory Roadblocks

The MedTech industry's growth ceiling is ultimately dictated by reimbursement policies, and both companies are currently caught in the crosshairs of payer dynamics.

Sensus experienced a sharp 34.3% YoY revenue contraction in 2025. This was not a failure of clinical demand, but rather a classic cyclical headwind: clinics delayed procurement in anticipation of new CMS CPT reimbursement codes taking effect in January 2026. This exposes the company's vulnerability to policy-driven purchasing pauses. Furthermore, Sensus faces concentration risk, with 92.3% of its revenue derived from North America and 52% from a single client.

IceCure faces a different reimbursement hurdle: the "coding transition chasm." Although its ProSense system achieved a monumental FDA De Novo classification for early-stage breast cancer and inclusion in the ASBrS clinical guidelines, it currently relies on a temporary Category III CPT code. The arduous wait for a permanent Category I code (expected around 2028) severely restricts immediate institutional adoption. Additionally, as an Israel-based entity, IceCure’s supply chain is highly sensitive to Middle Eastern geopolitical volatility and strict domestic IP transfer regulations. Globally, both companies must also navigate margin-compression risks in crucial overseas markets like China, driven by the expanding scope of Volume-Based Procurement (VBP) policies.

HDIN Viewpoint: Sector Positioning

From the perspective of HDIN Research, these two equities offer completely asymmetric risk-reward profiles. Sensus Healthcare is a defensive play. The company is actively utilizing its pristine balance sheet to weather temporary reimbursement volatility and transition into a higher-margin, asset-light service model. The primary metric to watch is the velocity of its order book rebound following the implementation of the 2026 CPT codes, alongside careful monitoring of its rising inventory levels.

IceCure Medical, conversely, is a high-risk, high-reward commercialization play. The clinical validation of its liquid nitrogen (LN2) cryoablation technology is unassailable, offering a true minimally invasive alternative to lumpectomies. However, the company's financial risk is flashing red. Its survival—and the realization of its underlying asset value—hinges entirely on its ability to secure non-dilutive bridge financing or strategic partnerships before its liquidity dries up. For IceCure, market access has been won; the battle for capital survival has just begun.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com