HeartFlow FY2025 Analysis: Commercial Scalability, AI Moats, and Platform Transition

Date : 2026-03-25

Reading : 228

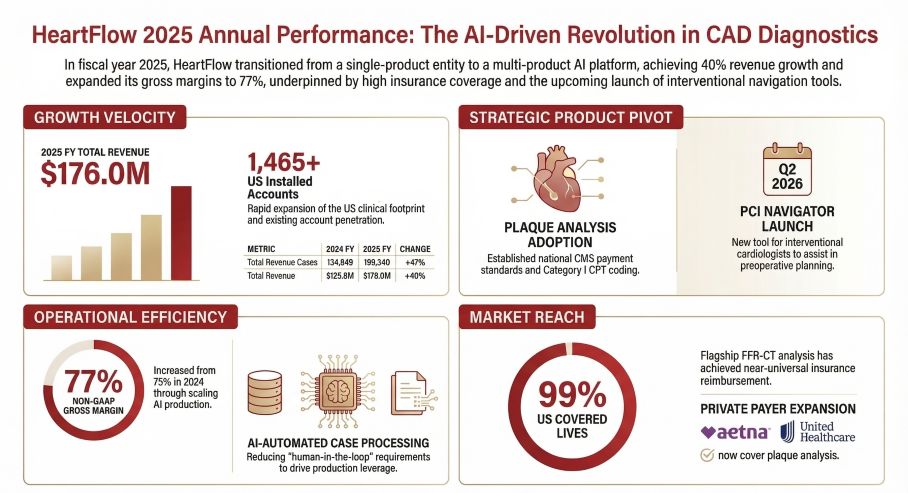

HeartFlow, Inc. has reached a critical inflection point in its commercialization journey. In Fiscal Year 2025, the company delivered a 40% year-over-year revenue surge to $176 million, proving the market viability of its cardiovascular AI software. However, beneath the top-line hyper-growth lies a complex narrative of structural margin optimization battling high cash burn, alongside an urgent strategic pivot from a single-product monopoly to a multi-tool diagnostic platform. According to HDIN Research, while HeartFlow’s proprietary AI and clinical data have forged formidable strategic moats, profitability remains heavily contingent on navigating cyclical headwinds, pricing pressures, and looming regulatory scrutiny.

Figure HeartFlow 2025 Annual Performance: The Al-Driven Revolution in CAD Diagnostics

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

HeartFlow’s FY2025 financial performance highlights the dual forces of high growth and sustained operational losses. Revenue growth was primarily driven by deeper utilization within its established base of over 1,465 U.S. accounts, rather than mere horizontal expansion. This shift indicates a maturing market presence where Customer Acquisition Cost (CAC) to Lifetime Value (LTV) ratios are significantly improving.

Operational efficiency played a pivotal role in expanding gross margins from 75% to 77%. This 200-basis-point lift is a direct result of third-generation AI algorithms enhancing "human-in-the-loop" productivity, substantially reducing manual intervention costs per scan. However, this margin expansion was partially offset by escalating third-party cloud hosting fees (AWS), illustrating the ongoing infrastructure cost burden inherent in processing high-fidelity 3D imaging at scale.

From a capital allocation perspective, the company remains in an aggressive "technology race" phase. With R&D consuming 37% of revenue and SG&A at 76%, the company reported a widened net loss of $117 million. Despite a cumulative deficit reaching $1.1 billion, HeartFlow’s liquidity remains robust, fortified by a post-IPO cash reserve of $280 million, ensuring adequate runway for near-term strategic deployments.

Sector Positioning & Strategic Moats

HeartFlow’s sector positioning is anchored by an overwhelming first-mover advantage. Currently, 98% of its revenue is generated from a single flagship product: the FFR-CT Analysis. The company operates on a highly sticky, usage-driven "pay-per-click" business model that directly correlates with clinical workflow volumes, offering a quasi-recurring revenue stream.

The company's strategic moats are built on two unassailable pillars:

1. Clinical Evidence and Reimbursement: FFR-CT has evolved from a supplementary tool to a defining standard for coronary artery disease (CAD) diagnosis, earning Class 2a/1A recommendations from the AHA and ACC. This clinical endorsement translates into a 99% commercial and Medicare coverage rate in the U.S., a formidable barrier to entry for emerging AI challengers like Cleerly and Elucid.

2. Proprietary Data Assets: With over 160 million human-annotated CCTA images and real-world data from 365,000 patients, HeartFlow possesses an irreplaceable training dataset that newer entrants cannot replicate purely through capital injection.

However, the competitive landscape is defined by a delicate "co-opetition" dynamic. HeartFlow lacks hardware ownership and relies entirely on imaging generated by traditional CT giants (Siemens Healthineers, GE Healthcare, Philips). As these legacy hardware manufacturers increasingly integrate proprietary AI workstations, HeartFlow faces the latent threat of vertical integration and technological decoupling.

Strategic Pivots & Cyclical Headwinds

To mitigate its reliance on a single product, HeartFlow is aggressively orchestrating a platform transition—evolving into a comprehensive suite that includes RoadMap, FFR-CT, and Plaque Analysis. A monumental milestone was achieved with the establishment of a unified Category I CPT code for AI-driven coronary plaque analysis, set to activate Medicare reimbursement in January 2026. This will likely serve as the primary catalyst for the company's next growth cycle.

Despite these advancements, HeartFlow faces significant cyclical headwinds and operational risks. Through the aggregation of 198,340 billed cases in FY2025, HDIN Research calculates an Average Selling Price (ASP) of approximately $887.54 per case. The discrepancy between case volume growth (+47%) and revenue growth (+40%) reveals downward pressure on ASP, driven by volume rebates and a strategic shift toward lower-margin clinic accounts.

Furthermore, the company must navigate severe regulatory red flags. A recent Department of Justice (DOJ) civil investigation regarding the Anti-Kickback Statute and False Claims Act casts a shadow over its compliance framework. Concurrently, a proposed 15% CMS payment rate reduction for FFR-CT in the 2026 OPPS draft poses a direct threat to future gross margins.

HDIN Viewpoint

HDIN Research views HeartFlow as the undisputed pioneer in non-invasive cardiovascular diagnostics, possessing unparalleled clinical validation and data supremacy. However, the company's current valuation faces a distinct overhang due to the DOJ investigation and its heavy reliance on FFR-CT.

The true inflection point for HeartFlow will not just be top-line revenue growth, but its ability to successfully commercialize and bundle its newer pipeline products, specifically the Plaque Analysis and the upcoming PCI Navigator (slated for 2026). Investors and strategic stakeholders must closely monitor the company's ASP stabilization and the translation of its high-cost R&D into tangible, margin-expanding clinical tools to assess when—and if—it can cross the threshold into profitability.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure HeartFlow 2025 Annual Performance: The Al-Driven Revolution in CAD Diagnostics

Financial Health & Capital Allocation EfficiencyHeartFlow’s FY2025 financial performance highlights the dual forces of high growth and sustained operational losses. Revenue growth was primarily driven by deeper utilization within its established base of over 1,465 U.S. accounts, rather than mere horizontal expansion. This shift indicates a maturing market presence where Customer Acquisition Cost (CAC) to Lifetime Value (LTV) ratios are significantly improving.

Operational efficiency played a pivotal role in expanding gross margins from 75% to 77%. This 200-basis-point lift is a direct result of third-generation AI algorithms enhancing "human-in-the-loop" productivity, substantially reducing manual intervention costs per scan. However, this margin expansion was partially offset by escalating third-party cloud hosting fees (AWS), illustrating the ongoing infrastructure cost burden inherent in processing high-fidelity 3D imaging at scale.

From a capital allocation perspective, the company remains in an aggressive "technology race" phase. With R&D consuming 37% of revenue and SG&A at 76%, the company reported a widened net loss of $117 million. Despite a cumulative deficit reaching $1.1 billion, HeartFlow’s liquidity remains robust, fortified by a post-IPO cash reserve of $280 million, ensuring adequate runway for near-term strategic deployments.

Sector Positioning & Strategic Moats

HeartFlow’s sector positioning is anchored by an overwhelming first-mover advantage. Currently, 98% of its revenue is generated from a single flagship product: the FFR-CT Analysis. The company operates on a highly sticky, usage-driven "pay-per-click" business model that directly correlates with clinical workflow volumes, offering a quasi-recurring revenue stream.

The company's strategic moats are built on two unassailable pillars:

1. Clinical Evidence and Reimbursement: FFR-CT has evolved from a supplementary tool to a defining standard for coronary artery disease (CAD) diagnosis, earning Class 2a/1A recommendations from the AHA and ACC. This clinical endorsement translates into a 99% commercial and Medicare coverage rate in the U.S., a formidable barrier to entry for emerging AI challengers like Cleerly and Elucid.

2. Proprietary Data Assets: With over 160 million human-annotated CCTA images and real-world data from 365,000 patients, HeartFlow possesses an irreplaceable training dataset that newer entrants cannot replicate purely through capital injection.

However, the competitive landscape is defined by a delicate "co-opetition" dynamic. HeartFlow lacks hardware ownership and relies entirely on imaging generated by traditional CT giants (Siemens Healthineers, GE Healthcare, Philips). As these legacy hardware manufacturers increasingly integrate proprietary AI workstations, HeartFlow faces the latent threat of vertical integration and technological decoupling.

Strategic Pivots & Cyclical Headwinds

To mitigate its reliance on a single product, HeartFlow is aggressively orchestrating a platform transition—evolving into a comprehensive suite that includes RoadMap, FFR-CT, and Plaque Analysis. A monumental milestone was achieved with the establishment of a unified Category I CPT code for AI-driven coronary plaque analysis, set to activate Medicare reimbursement in January 2026. This will likely serve as the primary catalyst for the company's next growth cycle.

Despite these advancements, HeartFlow faces significant cyclical headwinds and operational risks. Through the aggregation of 198,340 billed cases in FY2025, HDIN Research calculates an Average Selling Price (ASP) of approximately $887.54 per case. The discrepancy between case volume growth (+47%) and revenue growth (+40%) reveals downward pressure on ASP, driven by volume rebates and a strategic shift toward lower-margin clinic accounts.

Furthermore, the company must navigate severe regulatory red flags. A recent Department of Justice (DOJ) civil investigation regarding the Anti-Kickback Statute and False Claims Act casts a shadow over its compliance framework. Concurrently, a proposed 15% CMS payment rate reduction for FFR-CT in the 2026 OPPS draft poses a direct threat to future gross margins.

HDIN Viewpoint

HDIN Research views HeartFlow as the undisputed pioneer in non-invasive cardiovascular diagnostics, possessing unparalleled clinical validation and data supremacy. However, the company's current valuation faces a distinct overhang due to the DOJ investigation and its heavy reliance on FFR-CT.

The true inflection point for HeartFlow will not just be top-line revenue growth, but its ability to successfully commercialize and bundle its newer pipeline products, specifically the Plaque Analysis and the upcoming PCI Navigator (slated for 2026). Investors and strategic stakeholders must closely monitor the company's ASP stabilization and the translation of its high-cost R&D into tangible, margin-expanding clinical tools to assess when—and if—it can cross the threshold into profitability.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com