TeamViewer 2025 Strategic Pivot: Transitioning from Remote Tool to Autonomous Endpoint Management Platform

Date : 2026-03-25

Reading : 152

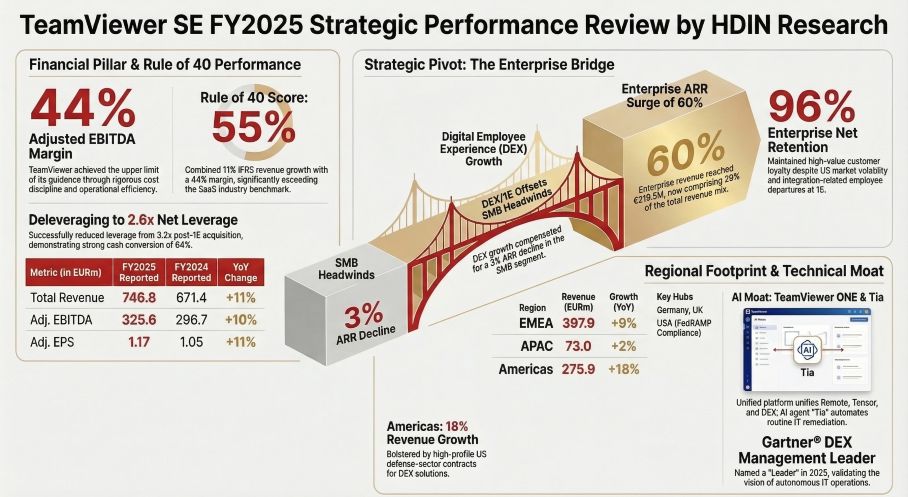

In 2025, TeamViewer reached a critical inflection point. According to HDIN Research's latest analysis, the company successfully transitioned from a legacy remote connectivity tool to a comprehensive Autonomous Endpoint Management (AEM) platform. Driven by the strategic acquisition of 1E and the deployment of its proprietary AI agent, "Tia," TeamViewer delivered an 11% revenue expansion to $844.3 million. However, beyond the top-line growth, the underlying data reveals a profound structural realignment: a massive surge in enterprise adoption juxtaposed against a deliberate, stabilizing calibration of its legacy mid-market base.

Figure TeamViewer SE FY2025 Strategic Performance Review

Structural Realignment: The Enterprise Surge vs. SMB Calibration

Structural Realignment: The Enterprise Surge vs. SMB Calibration

TeamViewer’s 2025 revenue distribution illustrates a textbook example of "sustaining the core while scaling the edge." The Enterprise segment emerged as the primary growth engine, with revenue jumping 45% to $248.2 million and Annual Recurring Revenue (ARR) surging by an unprecedented 60%. This hyper-growth is a direct result of successfully integrating 1E’s Digital Employee Experience (DEX) capabilities, which allowed TeamViewer to penetrate highly complex corporate IT environments.

Conversely, the Small and Medium Business (SMB) segment—historically the company's cash cow—saw revenue inch up by only 1%, alongside a 3% contraction in ARR. Rather than a sign of operational decay, HDIN Research assesses this as a calculated strategic pivot. Management proactively abandoned aggressive short-term price hikes and forced conversions to prioritize ecosystem stability, reduce churn, and cultivate a healthier pipeline for future cross-selling.

Strategic Moats and IT/OT Convergence

The software landscape is fraught with application-layer competitors like Zoom or Microsoft Teams, but TeamViewer has successfully insulated itself by building infrastructure-level strategic moats. The consolidation of isolated products into the unified "TeamViewer ONE" platform establishes a unique value proposition centered on IT/OT (Information Technology / Operational Technology) convergence.

TeamViewer’s competitive edge lies in its ability to manage non-standardized OT assets—such as industrial robotics, manufacturing control systems, and healthcare devices—capabilities that standard enterprise collaboration tools cannot replicate. Furthermore, the introduction of the "Tia" AI agent facilitates a "Shift-Left" strategy. By synthesizing 1E’s real-time observability data with millions of historical expert sessions, Tia autonomously diagnoses and executes remediation scripts before system failures impact the end-user, fundamentally shifting TeamViewer from a reactive support tool to a proactive management infrastructure.

Capital Allocation Efficiency and Balance Sheet Headwinds

While the operational transformation is robust, it has required significant balance sheet sacrifices. The 1E acquisition materially altered TeamViewer’s capital structure, pushing the Net Leverage Ratio from a conservative 1.3x up to 2.6x, alongside a spike in net financial debt to $1.019 billion.

Consequently, capital allocation efficiency has become the management's absolute priority. TeamViewer halted its aggressive share buyback program in 2025 to channel robust levered free cash flow ($235.5 million) entirely toward deleveraging. Looking ahead, management has instituted a strict M&A freeze for 2026, mandating a pure-play organic growth strategy to drive leverage down to a target of 2.3x.

HDIN Viewpoint: Digesting Acquisitions Amidst Macro Cyclicality

HDIN Research views TeamViewer’s 2025 fiscal year as a necessary period of "margin sacrifice for platform evolution." Despite the integration costs of a loss-making entity like 1E, the company exhibited exceptional cost discipline by maintaining a high Adjusted EBITDA margin of 44%.

However, cyclical headwinds remain a prominent risk factor. Delays in large-scale governmental procurement (notably influenced by US policy shifts) and a sluggish European macroeconomic environment contributed to a slight dip in the Enterprise Net Retention Rate (NRR) to 96%. For 2026, the critical metric for institutional investors will not be explosive top-line growth—which management conservatively guides at 0% to 3%—but rather the operational synergy realized from 1E. If AI-driven value-adds like DEX Essentials can successfully defend the SMB baseline and validate the surging goodwill on the balance sheet, TeamViewer is exceptionally well-positioned to dominate the next generation of DWM (Digital Workplace Management) ecosystems.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure TeamViewer SE FY2025 Strategic Performance Review

Structural Realignment: The Enterprise Surge vs. SMB CalibrationTeamViewer’s 2025 revenue distribution illustrates a textbook example of "sustaining the core while scaling the edge." The Enterprise segment emerged as the primary growth engine, with revenue jumping 45% to $248.2 million and Annual Recurring Revenue (ARR) surging by an unprecedented 60%. This hyper-growth is a direct result of successfully integrating 1E’s Digital Employee Experience (DEX) capabilities, which allowed TeamViewer to penetrate highly complex corporate IT environments.

Conversely, the Small and Medium Business (SMB) segment—historically the company's cash cow—saw revenue inch up by only 1%, alongside a 3% contraction in ARR. Rather than a sign of operational decay, HDIN Research assesses this as a calculated strategic pivot. Management proactively abandoned aggressive short-term price hikes and forced conversions to prioritize ecosystem stability, reduce churn, and cultivate a healthier pipeline for future cross-selling.

Strategic Moats and IT/OT Convergence

The software landscape is fraught with application-layer competitors like Zoom or Microsoft Teams, but TeamViewer has successfully insulated itself by building infrastructure-level strategic moats. The consolidation of isolated products into the unified "TeamViewer ONE" platform establishes a unique value proposition centered on IT/OT (Information Technology / Operational Technology) convergence.

TeamViewer’s competitive edge lies in its ability to manage non-standardized OT assets—such as industrial robotics, manufacturing control systems, and healthcare devices—capabilities that standard enterprise collaboration tools cannot replicate. Furthermore, the introduction of the "Tia" AI agent facilitates a "Shift-Left" strategy. By synthesizing 1E’s real-time observability data with millions of historical expert sessions, Tia autonomously diagnoses and executes remediation scripts before system failures impact the end-user, fundamentally shifting TeamViewer from a reactive support tool to a proactive management infrastructure.

Capital Allocation Efficiency and Balance Sheet Headwinds

While the operational transformation is robust, it has required significant balance sheet sacrifices. The 1E acquisition materially altered TeamViewer’s capital structure, pushing the Net Leverage Ratio from a conservative 1.3x up to 2.6x, alongside a spike in net financial debt to $1.019 billion.

Consequently, capital allocation efficiency has become the management's absolute priority. TeamViewer halted its aggressive share buyback program in 2025 to channel robust levered free cash flow ($235.5 million) entirely toward deleveraging. Looking ahead, management has instituted a strict M&A freeze for 2026, mandating a pure-play organic growth strategy to drive leverage down to a target of 2.3x.

HDIN Viewpoint: Digesting Acquisitions Amidst Macro Cyclicality

HDIN Research views TeamViewer’s 2025 fiscal year as a necessary period of "margin sacrifice for platform evolution." Despite the integration costs of a loss-making entity like 1E, the company exhibited exceptional cost discipline by maintaining a high Adjusted EBITDA margin of 44%.

However, cyclical headwinds remain a prominent risk factor. Delays in large-scale governmental procurement (notably influenced by US policy shifts) and a sluggish European macroeconomic environment contributed to a slight dip in the Enterprise Net Retention Rate (NRR) to 96%. For 2026, the critical metric for institutional investors will not be explosive top-line growth—which management conservatively guides at 0% to 3%—but rather the operational synergy realized from 1E. If AI-driven value-adds like DEX Essentials can successfully defend the SMB baseline and validate the surging goodwill on the balance sheet, TeamViewer is exceptionally well-positioned to dominate the next generation of DWM (Digital Workplace Management) ecosystems.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com