Global EBD Medical Aesthetics Market 2025: Strategic Moats, Capital Allocation, and Sector Positioning

Date : 2026-03-24

Reading : 361

The 2025 Global Energy-Based Device (EBD) medical aesthetics market is undergoing a profound structural bifurcation. According to the latest proprietary financial analysis by HDIN Research, the era of capturing market share through pure equipment sales has officially ended. Today, sector dominance is dictated by capital allocation efficiency, the monopolistic power of the "razor-and-blade" consumable model, and the ability to navigate cyclical macro-headwinds.

Our deep-dive audit of nine leading global EBD manufacturers—including Solta Medical (Bausch Health), InMode, Haohai Biological (EndyMed), and Wontech—reveals a stark contrast between highly defensive, cash-rich incumbents and regional players facing severe liquidity and operational bottlenecks.

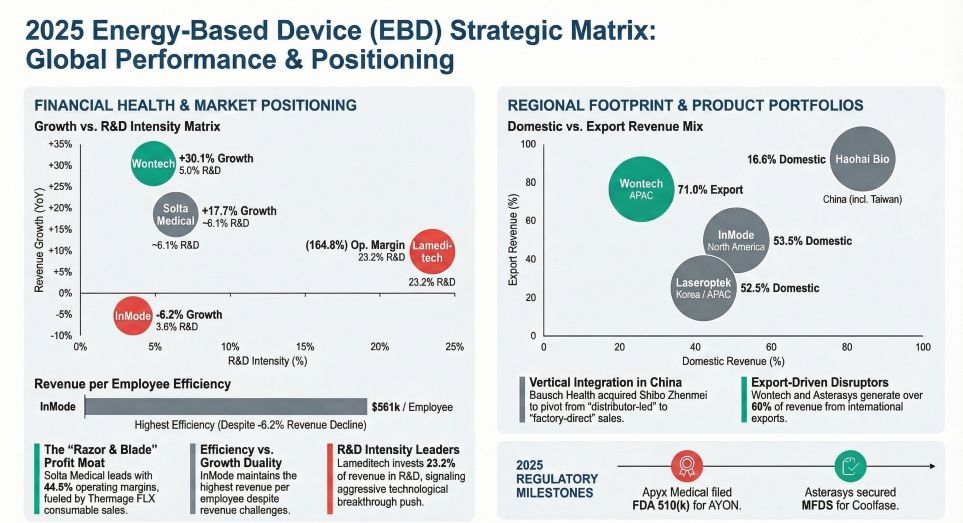

Figure 2025 Energy-Based Device (EBD) Strategic Matrix: Global Performance & Positioning

Capital Allocation Efficiency & Financial Health

Capital Allocation Efficiency & Financial Health

In an environment marked by structural cost pressures and supply chain vulnerabilities, operational efficiency serves as the ultimate defensive moat against macroeconomic volatility.

The Fortified Incumbents: InMode and Haohai Biological demonstrate exceptional cash flow defensibility. InMode operates on a highly lucrative, McKinsey-style high-value model, maintaining a gross margin of 78.5%. Its extreme conservative capital structure, marked by zero debt and massive cash reserves, allowed the company to execute a $127 million share buyback in 2025, transforming high interest rates from a liability into a lucrative yield generator. Similarly, Haohai Biological exhibits a remarkably lean Days Sales Outstanding (DSO) of approximately 40 days and a 196% operating cash flow-to-net-income coverage ratio, highlighting its formidable pricing power and mature distributor credit management in the Chinese market.

Liquidity Constraints & Solvency Risks: Conversely, Apyx Medical is navigating dangerous waters. Straddled with a DSO of 115.8 days and negative operating cash flows, the company's capital structure is highly fragile. Constrained by tight credit agreements and mounting interest expenses, Apyx's inability to rapidly commercialize new technologies poses severe dilution or default risks, underscoring the lethal consequences of poor capital allocation in a capital-intensive sector.

Strategic Pivots: The "Razor-and-Blade" Imperative

The most critical strategic implication of the 2025 data is the absolute necessity of transitioning to a high-margin consumables model. Installed equipment bases are no longer the end goal; they are merely the acquisition channel for recurring consumable revenue.

Solta Medical stands as the industry’s profitability benchmark. By leveraging the monopolistic global positioning of its Thermage FLX system, Solta achieved an anomalous 44.8% departmental operating margin. Crucially, over 75% of its historical revenue stems from consumables (treatment tips), providing unparalleled anti-cyclical stability.

Asian challengers are rapidly adopting this playbook. Wontech, 2025’s growth champion, achieved a 30.1% revenue surge driven by its Oligio RF platform. More importantly, Wontech saw a staggering 149% year-over-year growth in high-frequency consumable tips. This transition not only fuels top-line expansion but fundamentally optimizes the profit structure, proving that the "razor-and-blade" model is the preeminent driver of valuation multiples in the EBD space.

Regional Shifts and Cyclical Headwinds

Global EBD revenue distribution is shifting from "Western Pricing Power" to "APAC Cost-Performance."

Companies like Wontech and Asterasys are aggressively penetrating overseas markets, with Wontech’s international revenue share surging to 71.0%. By offering high-performance alternatives to Western monopoles, these South Korean manufacturers are successfully executing an "import substitution" strategy across Asia and Latin America.

However, cyclical headwinds and regulatory ceilings are tightening. HDIN Research notes that the FDA’s modernized 510(k) pathways, the EU’s MDR, and China’s NMPA reclassification of RF devices as Class III medical devices have drastically extended R&D and commercialization cycles. Haohai Biological, which generates 83.4% of its revenue domestically, is countering these headwinds through deep vertical integration—privatizing Israel's EndyMed and developing proprietary VCSEL laser chips to establish a highly differentiated "device + biologic" (RF and Hyaluronic Acid) synergistic moat.

Financial Transparency and Audit Red Flags

In a maturing market, granular financial data often exposes underlying operational distress. Our 2025 audit trail identified several critical red flags that institutional investors must monitor:

* Revenue Cut-off Errors: BTB Korea’s audit highlighted potential revenue recognition irregularities, a classic warning sign of channel stuffing to mask deteriorating demand.

* Forecast Failures & R&D Overextension: Lameditech missed its 2025 revenue forecasts by nearly 50%. Despite allocating an unsustainable 23.2% of its revenue to R&D, the startup's massive operating losses indicate a broken commercialization engine.

* Goodwill Impairment: Haohai recognized significant asset impairments in 2025, a reminder that premium acquisitions executed during industry upcycles can quickly become balance sheet liabilities during macroeconomic downturns.

HDIN Viewpoint

HDIN Research concludes that the 2026 EBD market will be defined by consolidation, compliance, and consumables. Mid-tier companies failing to transition from pure equipment sales to recurring consumable models will face severe margin compression. Furthermore, as Western giants like Solta Medical and InMode aggressively pivot toward direct-to-consumer distribution in APAC—bypassing traditional proxy models—regional players must either vertically integrate their supply chains or risk obsolescence. Investors are advised to prioritize firms with fortress balance sheets, high consumable attach rates, and AI-integrated platforms that defend against counterfeit consumables.

Presentation Download & Video Analysis

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Our deep-dive audit of nine leading global EBD manufacturers—including Solta Medical (Bausch Health), InMode, Haohai Biological (EndyMed), and Wontech—reveals a stark contrast between highly defensive, cash-rich incumbents and regional players facing severe liquidity and operational bottlenecks.

Figure 2025 Energy-Based Device (EBD) Strategic Matrix: Global Performance & Positioning

Capital Allocation Efficiency & Financial HealthIn an environment marked by structural cost pressures and supply chain vulnerabilities, operational efficiency serves as the ultimate defensive moat against macroeconomic volatility.

The Fortified Incumbents: InMode and Haohai Biological demonstrate exceptional cash flow defensibility. InMode operates on a highly lucrative, McKinsey-style high-value model, maintaining a gross margin of 78.5%. Its extreme conservative capital structure, marked by zero debt and massive cash reserves, allowed the company to execute a $127 million share buyback in 2025, transforming high interest rates from a liability into a lucrative yield generator. Similarly, Haohai Biological exhibits a remarkably lean Days Sales Outstanding (DSO) of approximately 40 days and a 196% operating cash flow-to-net-income coverage ratio, highlighting its formidable pricing power and mature distributor credit management in the Chinese market.

Liquidity Constraints & Solvency Risks: Conversely, Apyx Medical is navigating dangerous waters. Straddled with a DSO of 115.8 days and negative operating cash flows, the company's capital structure is highly fragile. Constrained by tight credit agreements and mounting interest expenses, Apyx's inability to rapidly commercialize new technologies poses severe dilution or default risks, underscoring the lethal consequences of poor capital allocation in a capital-intensive sector.

Strategic Pivots: The "Razor-and-Blade" Imperative

The most critical strategic implication of the 2025 data is the absolute necessity of transitioning to a high-margin consumables model. Installed equipment bases are no longer the end goal; they are merely the acquisition channel for recurring consumable revenue.

Solta Medical stands as the industry’s profitability benchmark. By leveraging the monopolistic global positioning of its Thermage FLX system, Solta achieved an anomalous 44.8% departmental operating margin. Crucially, over 75% of its historical revenue stems from consumables (treatment tips), providing unparalleled anti-cyclical stability.

Asian challengers are rapidly adopting this playbook. Wontech, 2025’s growth champion, achieved a 30.1% revenue surge driven by its Oligio RF platform. More importantly, Wontech saw a staggering 149% year-over-year growth in high-frequency consumable tips. This transition not only fuels top-line expansion but fundamentally optimizes the profit structure, proving that the "razor-and-blade" model is the preeminent driver of valuation multiples in the EBD space.

Regional Shifts and Cyclical Headwinds

Global EBD revenue distribution is shifting from "Western Pricing Power" to "APAC Cost-Performance."

Companies like Wontech and Asterasys are aggressively penetrating overseas markets, with Wontech’s international revenue share surging to 71.0%. By offering high-performance alternatives to Western monopoles, these South Korean manufacturers are successfully executing an "import substitution" strategy across Asia and Latin America.

However, cyclical headwinds and regulatory ceilings are tightening. HDIN Research notes that the FDA’s modernized 510(k) pathways, the EU’s MDR, and China’s NMPA reclassification of RF devices as Class III medical devices have drastically extended R&D and commercialization cycles. Haohai Biological, which generates 83.4% of its revenue domestically, is countering these headwinds through deep vertical integration—privatizing Israel's EndyMed and developing proprietary VCSEL laser chips to establish a highly differentiated "device + biologic" (RF and Hyaluronic Acid) synergistic moat.

Financial Transparency and Audit Red Flags

In a maturing market, granular financial data often exposes underlying operational distress. Our 2025 audit trail identified several critical red flags that institutional investors must monitor:

* Revenue Cut-off Errors: BTB Korea’s audit highlighted potential revenue recognition irregularities, a classic warning sign of channel stuffing to mask deteriorating demand.

* Forecast Failures & R&D Overextension: Lameditech missed its 2025 revenue forecasts by nearly 50%. Despite allocating an unsustainable 23.2% of its revenue to R&D, the startup's massive operating losses indicate a broken commercialization engine.

* Goodwill Impairment: Haohai recognized significant asset impairments in 2025, a reminder that premium acquisitions executed during industry upcycles can quickly become balance sheet liabilities during macroeconomic downturns.

HDIN Viewpoint

HDIN Research concludes that the 2026 EBD market will be defined by consolidation, compliance, and consumables. Mid-tier companies failing to transition from pure equipment sales to recurring consumable models will face severe margin compression. Furthermore, as Western giants like Solta Medical and InMode aggressively pivot toward direct-to-consumer distribution in APAC—bypassing traditional proxy models—regional players must either vertically integrate their supply chains or risk obsolescence. Investors are advised to prioritize firms with fortress balance sheets, high consumable attach rates, and AI-integrated platforms that defend against counterfeit consumables.

Presentation Download & Video Analysis

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com