Value Reconstruction Over Scale: Unpacking the 2025 Structural Pivot of South Korea’s Chemical Giants

Date : 2026-03-24

Reading : 168

The South Korean petrochemical and materials sector has officially reached a critical inflection point in 2025. Squeezed by high global interest rates and structural overcapacity, the era of relying on sheer production volume for profitability has ended. Based on a comprehensive review of the 2025 annual reports of top industry players, HDIN Research reveals a stark bifurcation in the market: companies tethered to legacy commodity chemicals are facing severe liquidity crises, while those executing aggressive capital allocation toward high-barrier strategic moats are successfully insulating themselves from cyclical headwinds.

The underlying data suggests that operational efficiency, targeted capital expenditures (CAPEX), and supply chain agility are now the ultimate determinants of survival.

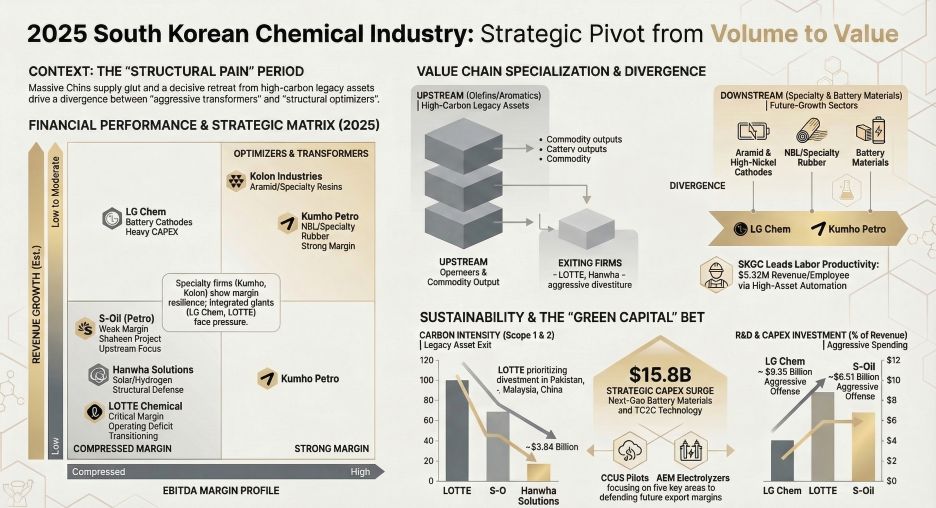

Figure 2025 South Korean Chemical industry: Strategic Pivot from Volume to Value

Capital Allocation Efficiency and Earnings Quality Divergence

Capital Allocation Efficiency and Earnings Quality Divergence

In a macroeconomic environment plagued by demand stagnation in construction and consumer electronics, financial leverage and cash flow generation have exposed massive discrepancies in corporate resilience.

Kumho Petrochemical emerges as a benchmark for capital efficiency. By maintaining an ultra-low debt-to-equity ratio of 36.4% and an exceptional Operating Cash Flow to Net Income (OCF/NI) ratio of 198%, the company’s profits are entirely backed by actual cash inflows. Furthermore, an industry-leading inventory turnover rate of 21.45 times demonstrates superior supply chain agility, effectively insulating the firm from inventory depreciation amidst volatile raw material pricing.

Conversely, players with high cyclical exposure are deploying defensive accounting maneuvers. Lotte Chemical and LG Chemical (Petrochemical Division) reported staggering operating losses in 2025. Lotte Chemical, hindered by negative interest coverage, has initiated a classic "Big Bath" strategy—recognizing massive asset and goodwill impairments (including over $220 million related to Lotte Energy Materials). While this aggressive write-down cleanses the balance sheet for future quarters, it underscores severe short-term liquidity anxiety.

Sector Positioning: Building Strategic Moats vs. Defensive Contraction

The 2025 CAPEX trajectories illustrate a definitive shift from broad-based expansion to targeted technological dominance. HDIN Research categorizes these strategic pivots into three distinct models:

* The Aggressive Transformers: S-Oil is executing the largest CAPEX initiative in its history with the $6.5 billion Shaheen Project. By integrating TC2C technology to convert crude directly into chemical feedstocks, S-Oil is fundamentally rewriting its cost-curve advantage. Similarly, LG Chemical is cementing a "chain-linked" moat by binding its battery materials (high-nickel cathodes) directly to North American automotive OEMs.

* The Specialty Niche Defenders: Companies like Kolon Industries and Lotte Fine Chemical are proving that high-margin technical barriers outlast volume plays. Kolon’s capacity doubling in Aramid (super fibers) and Lotte Fine Chemical’s 46% domestic market share in cellulose products grant them absolute pricing power, shielding them from the commodity bloodbath.

* The Structural Optimizers: Lotte Chemical is executing a defensive contraction, divesting non-core legacy assets (such as its Pakistan PTA plant and Malaysian synthetic rubber business) to reallocate scarce capital toward its Indonesian (LCI) mega-project and advanced composites.

Navigating Geopolitical and Cyclical Headwinds

The most pronounced systemic risk identified in 2025 is the "China Factor." China has structurally transitioned from the world's largest importer to a net exporter of base chemicals. This massive capacity injection has crushed historical price spreads for polyethylene (PE) and polypropylene (PP), transforming a cyclical dip into a long-term structural ceiling.

Simultaneously, global policy frameworks are reshaping trade routes. The impending European Carbon Border Adjustment Mechanism (CBAM) implementation in 2026 acts as a hard policy ceiling, forcing legacy high-carbon assets into obsolescence. Meanwhile, uncertainties surrounding the U.S. Inflation Reduction Act (IRA) and potential reciprocal tariffs are driving capital flight toward localized production. For example, Kolon Industries is expanding its footprint in Vietnam to hedge against Chinese competition, while SK Innovation and Hanwha Solutions are aggressively localizing battery and solar capacities in the Americas.

The HDIN Viewpoint: Look Beyond the Top Line

As an independent consulting firm, HDIN Research advises stakeholders to exercise extreme caution regarding top-line revenue growth that masks underlying cash bleed.

The 2025 financial disclosures present clear audit red flags for investors. For instance, while SK Innovation boasts revenue growth via its BlueOval SK battery joint venture, the operation is characterized by a "cash-burn" model—reporting over $3 billion in net losses heavily reliant on external financing. Similarly, Hanwha Solutions' reliance on a labyrinthine structure of 228 Special Purpose Vehicles (SPVs) significantly diminishes corporate transparency, demanding a higher risk premium from the market.

The ultimate takeaway for 2025 is clear: the South Korean chemical sector is undergoing a painful but necessary value reconstruction. The winners of the next decade will not be the companies with the largest ethylene crackers, but rather those who possess the agility to divest toxic legacy assets and secure monopolistic positions in next-generation battery materials, hydrogen value chains, and fine chemicals.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

The underlying data suggests that operational efficiency, targeted capital expenditures (CAPEX), and supply chain agility are now the ultimate determinants of survival.

Figure 2025 South Korean Chemical industry: Strategic Pivot from Volume to Value

Capital Allocation Efficiency and Earnings Quality DivergenceIn a macroeconomic environment plagued by demand stagnation in construction and consumer electronics, financial leverage and cash flow generation have exposed massive discrepancies in corporate resilience.

Kumho Petrochemical emerges as a benchmark for capital efficiency. By maintaining an ultra-low debt-to-equity ratio of 36.4% and an exceptional Operating Cash Flow to Net Income (OCF/NI) ratio of 198%, the company’s profits are entirely backed by actual cash inflows. Furthermore, an industry-leading inventory turnover rate of 21.45 times demonstrates superior supply chain agility, effectively insulating the firm from inventory depreciation amidst volatile raw material pricing.

Conversely, players with high cyclical exposure are deploying defensive accounting maneuvers. Lotte Chemical and LG Chemical (Petrochemical Division) reported staggering operating losses in 2025. Lotte Chemical, hindered by negative interest coverage, has initiated a classic "Big Bath" strategy—recognizing massive asset and goodwill impairments (including over $220 million related to Lotte Energy Materials). While this aggressive write-down cleanses the balance sheet for future quarters, it underscores severe short-term liquidity anxiety.

Sector Positioning: Building Strategic Moats vs. Defensive Contraction

The 2025 CAPEX trajectories illustrate a definitive shift from broad-based expansion to targeted technological dominance. HDIN Research categorizes these strategic pivots into three distinct models:

* The Aggressive Transformers: S-Oil is executing the largest CAPEX initiative in its history with the $6.5 billion Shaheen Project. By integrating TC2C technology to convert crude directly into chemical feedstocks, S-Oil is fundamentally rewriting its cost-curve advantage. Similarly, LG Chemical is cementing a "chain-linked" moat by binding its battery materials (high-nickel cathodes) directly to North American automotive OEMs.

* The Specialty Niche Defenders: Companies like Kolon Industries and Lotte Fine Chemical are proving that high-margin technical barriers outlast volume plays. Kolon’s capacity doubling in Aramid (super fibers) and Lotte Fine Chemical’s 46% domestic market share in cellulose products grant them absolute pricing power, shielding them from the commodity bloodbath.

* The Structural Optimizers: Lotte Chemical is executing a defensive contraction, divesting non-core legacy assets (such as its Pakistan PTA plant and Malaysian synthetic rubber business) to reallocate scarce capital toward its Indonesian (LCI) mega-project and advanced composites.

Navigating Geopolitical and Cyclical Headwinds

The most pronounced systemic risk identified in 2025 is the "China Factor." China has structurally transitioned from the world's largest importer to a net exporter of base chemicals. This massive capacity injection has crushed historical price spreads for polyethylene (PE) and polypropylene (PP), transforming a cyclical dip into a long-term structural ceiling.

Simultaneously, global policy frameworks are reshaping trade routes. The impending European Carbon Border Adjustment Mechanism (CBAM) implementation in 2026 acts as a hard policy ceiling, forcing legacy high-carbon assets into obsolescence. Meanwhile, uncertainties surrounding the U.S. Inflation Reduction Act (IRA) and potential reciprocal tariffs are driving capital flight toward localized production. For example, Kolon Industries is expanding its footprint in Vietnam to hedge against Chinese competition, while SK Innovation and Hanwha Solutions are aggressively localizing battery and solar capacities in the Americas.

The HDIN Viewpoint: Look Beyond the Top Line

As an independent consulting firm, HDIN Research advises stakeholders to exercise extreme caution regarding top-line revenue growth that masks underlying cash bleed.

The 2025 financial disclosures present clear audit red flags for investors. For instance, while SK Innovation boasts revenue growth via its BlueOval SK battery joint venture, the operation is characterized by a "cash-burn" model—reporting over $3 billion in net losses heavily reliant on external financing. Similarly, Hanwha Solutions' reliance on a labyrinthine structure of 228 Special Purpose Vehicles (SPVs) significantly diminishes corporate transparency, demanding a higher risk premium from the market.

The ultimate takeaway for 2025 is clear: the South Korean chemical sector is undergoing a painful but necessary value reconstruction. The winners of the next decade will not be the companies with the largest ethylene crackers, but rather those who possess the agility to divest toxic legacy assets and secure monopolistic positions in next-generation battery materials, hydrogen value chains, and fine chemicals.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com