Strategic Moats vs. Systemic Bottlenecks: A Deep Dive into Research Frontiers’ (RFI) 2025 Financials and Supply Chain Resilience

Date : 2026-03-28

Reading : 212

Research Frontiers Inc. (RFI) stands at a critical commercial inflection point. While the company’s 2025 financial disclosures confirm that its Suspended Particle Device (SPD) technology has successfully transitioned from niche validation into serialized production in the ultra-luxury automotive sector, deep structural vulnerabilities remain. An asset-light licensing model has insulated RFI from heavy manufacturing capex, yet extreme customer concentration and a symbiotic dependency on a single commercial supplier have created a fragile financial equilibrium. Operational execution, rather than pure patent accumulation, will dictate the company's trajectory in 2026.

Figure Research Frontiers Inc (REFR) 2025: The Strategic Pivot to Serial Production Scaling

Sector Positioning and Strategic Moats

Sector Positioning and Strategic Moats

In the smart glass sector, the technological rivalry between SPD, Electrochromic (EC), and Liquid Crystal (LC) technologies is undergoing a rapid market filtration. The recent financial collapse of major EC players like View Inc. and Halio underscores the severe capital expenditure risks associated with heavy-asset manufacturing in this space.

Conversely, RFI’s asset-light licensing strategy has functioned as a partial financial safe harbor. Technologically, SPD maintains a distinct competitive edge in high-end mobility markets. Unlike EC, which suffers from slow transition times and the "iris effect" (edge-to-center shading), SPD offers near-instantaneous switching, superior optical uniformity, and up to 99.5% visible light blockage.

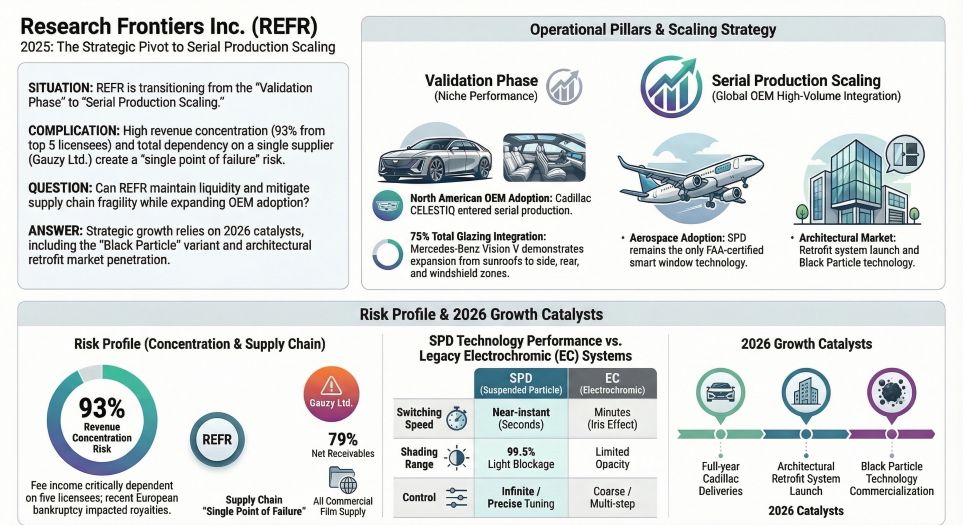

This technological premium has translated into tangible commercial milestones in 2025. The serialized production of the Cadillac CELESTIQ—featuring the largest multi-zone SPD smart glass deployment in a production vehicle—and the integration into the Ferrari Purosangue validate SPD's dominance in the automotive sector. Furthermore, as the only smart window technology securing FAA Supplemental Type Certificates (STC), SPD maintains an undisputed moat in the aerospace industry, equipped in over 40 aircraft models. To sustain this momentum, RFI's 2025 launch of the "Black Particle" variant is a critical strategic pivot designed to resolve legacy aesthetic constraints and accelerate broader OEM adoption.

Financial Health and Capital Allocation Efficiency

Despite robust technological validation, RFI’s 2025 income statement reflects the cyclical headwinds and execution risks inherent to its licensing model. Total fee income contracted by 16% year-over-year to $1,121,248, driven primarily by the bankruptcy of a key European licensee. This disruption highlights a significant "So What" factor: RFI’s revenue quality is highly sensitive to the Minimum Annual Royalties (MAR) mechanism and the financial solvency of downstream partners.

Customer concentration reached extreme levels in 2025, with the top five licensees contributing 93% of total fee income. Consequently, the company's cash flow faced severe liquidity constraints. By the end of 2025, RFI’s cash reserves dwindled to approximately $664,299. Based on an average monthly operating cash burn rate of over $110,000, the company’s financial safety margin was compressed to a mere six months.

While a $1.1 million Private Investment in Public Equity (PIPE) financing in February 2026 extended the operational runway to roughly 18 months, the capital allocation dynamics warrant strict scrutiny. The participation of insiders—including board affiliates and licensee owners—indicates a reliance on "inside-circle" capital injections, reflecting broader challenges in securing low-cost institutional capital on the open market.

Supply Chain: The "Single Point of Failure" Risk

The most glaring vulnerability in RFI’s business architecture is its profound supply chain concentration. Currently, Gauzy Ltd. is the exclusive commercial-scale supplier of the critical SPD film and serves as both a primary licensee and an operational linchpin.

This deep integration has morphed from a standard technology licensing agreement into a state of "operational hosting." From a risk management perspective, this represents a systemic "Single Point of Failure." In 2025, a staggering 79% of RFI’s net accounts receivable were tied to Gauzy and its subsidiaries (a sharp surge from 25% in 2024). This immense concentration dictates that RFI's cash conversion cycle is virtually captive to Gauzy's payment pacing. Furthermore, with Gauzy’s CEO sitting on RFI’s board of directors, the intertwined governance structure complicates independent strategic oversight. Should Gauzy encounter localized geopolitical volatility or internal cash flow bottlenecks, RFI would face an immediate, unhedged disruption to its global commercialization pipeline.

HDIN Viewpoint: Navigating the 2026 Transition

As an independent market consulting firm, HDIN Research assesses that RFI's valuation anchor is fundamentally shifting. For over a decade, the company's value was underwritten by its extensive patent portfolio. However, with early core patents facing expirations beginning in 2026, the defensive moat of pure IP is narrowing.

Moving forward, RFI’s capacity to command its historical 10-15% royalty premiums will depend entirely on execution. The successful commercial scaling of the "Black Particle" variant and the strategic penetration into the ESG-driven architectural retrofit market will be paramount. Ultimately, RFI possesses a world-class technology layer, but institutional investors must closely monitor the firm's ability to diversify its supply chain away from a sole-vendor dependency and translate automotive OEM design wins into robust, predictable cash flows.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Research Frontiers Inc (REFR) 2025: The Strategic Pivot to Serial Production Scaling

Sector Positioning and Strategic MoatsIn the smart glass sector, the technological rivalry between SPD, Electrochromic (EC), and Liquid Crystal (LC) technologies is undergoing a rapid market filtration. The recent financial collapse of major EC players like View Inc. and Halio underscores the severe capital expenditure risks associated with heavy-asset manufacturing in this space.

Conversely, RFI’s asset-light licensing strategy has functioned as a partial financial safe harbor. Technologically, SPD maintains a distinct competitive edge in high-end mobility markets. Unlike EC, which suffers from slow transition times and the "iris effect" (edge-to-center shading), SPD offers near-instantaneous switching, superior optical uniformity, and up to 99.5% visible light blockage.

This technological premium has translated into tangible commercial milestones in 2025. The serialized production of the Cadillac CELESTIQ—featuring the largest multi-zone SPD smart glass deployment in a production vehicle—and the integration into the Ferrari Purosangue validate SPD's dominance in the automotive sector. Furthermore, as the only smart window technology securing FAA Supplemental Type Certificates (STC), SPD maintains an undisputed moat in the aerospace industry, equipped in over 40 aircraft models. To sustain this momentum, RFI's 2025 launch of the "Black Particle" variant is a critical strategic pivot designed to resolve legacy aesthetic constraints and accelerate broader OEM adoption.

Financial Health and Capital Allocation Efficiency

Despite robust technological validation, RFI’s 2025 income statement reflects the cyclical headwinds and execution risks inherent to its licensing model. Total fee income contracted by 16% year-over-year to $1,121,248, driven primarily by the bankruptcy of a key European licensee. This disruption highlights a significant "So What" factor: RFI’s revenue quality is highly sensitive to the Minimum Annual Royalties (MAR) mechanism and the financial solvency of downstream partners.

Customer concentration reached extreme levels in 2025, with the top five licensees contributing 93% of total fee income. Consequently, the company's cash flow faced severe liquidity constraints. By the end of 2025, RFI’s cash reserves dwindled to approximately $664,299. Based on an average monthly operating cash burn rate of over $110,000, the company’s financial safety margin was compressed to a mere six months.

While a $1.1 million Private Investment in Public Equity (PIPE) financing in February 2026 extended the operational runway to roughly 18 months, the capital allocation dynamics warrant strict scrutiny. The participation of insiders—including board affiliates and licensee owners—indicates a reliance on "inside-circle" capital injections, reflecting broader challenges in securing low-cost institutional capital on the open market.

Supply Chain: The "Single Point of Failure" Risk

The most glaring vulnerability in RFI’s business architecture is its profound supply chain concentration. Currently, Gauzy Ltd. is the exclusive commercial-scale supplier of the critical SPD film and serves as both a primary licensee and an operational linchpin.

This deep integration has morphed from a standard technology licensing agreement into a state of "operational hosting." From a risk management perspective, this represents a systemic "Single Point of Failure." In 2025, a staggering 79% of RFI’s net accounts receivable were tied to Gauzy and its subsidiaries (a sharp surge from 25% in 2024). This immense concentration dictates that RFI's cash conversion cycle is virtually captive to Gauzy's payment pacing. Furthermore, with Gauzy’s CEO sitting on RFI’s board of directors, the intertwined governance structure complicates independent strategic oversight. Should Gauzy encounter localized geopolitical volatility or internal cash flow bottlenecks, RFI would face an immediate, unhedged disruption to its global commercialization pipeline.

HDIN Viewpoint: Navigating the 2026 Transition

As an independent market consulting firm, HDIN Research assesses that RFI's valuation anchor is fundamentally shifting. For over a decade, the company's value was underwritten by its extensive patent portfolio. However, with early core patents facing expirations beginning in 2026, the defensive moat of pure IP is narrowing.

Moving forward, RFI’s capacity to command its historical 10-15% royalty premiums will depend entirely on execution. The successful commercial scaling of the "Black Particle" variant and the strategic penetration into the ESG-driven architectural retrofit market will be paramount. Ultimately, RFI possesses a world-class technology layer, but institutional investors must closely monitor the firm's ability to diversify its supply chain away from a sole-vendor dependency and translate automotive OEM design wins into robust, predictable cash flows.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com