Intuitive Machines: The Strategic Paradigm Shift from Payload Delivery to Space Infrastructure IaaS

Date : 2026-03-25

Reading : 118

Intuitive Machines, Inc. (IM) is navigating a critical inflection point, transitioning from a cyclical, milestone-dependent space contractor to a continuous "Infrastructure-as-a-Service" (IaaS) operator. According to the latest analysis by HDIN Research, while the company recorded a net loss of $106.8 million on $210.06 million in revenue for fiscal year 2025, these top-line metrics mask a profound structural transformation. By aggressively executing vertical integration through the acquisitions of KinetX and Lanteris, IM is constructing a formidable strategic moat across the low Earth orbit (LEO), geosynchronous equatorial orbit (GEO), and cislunar economy.

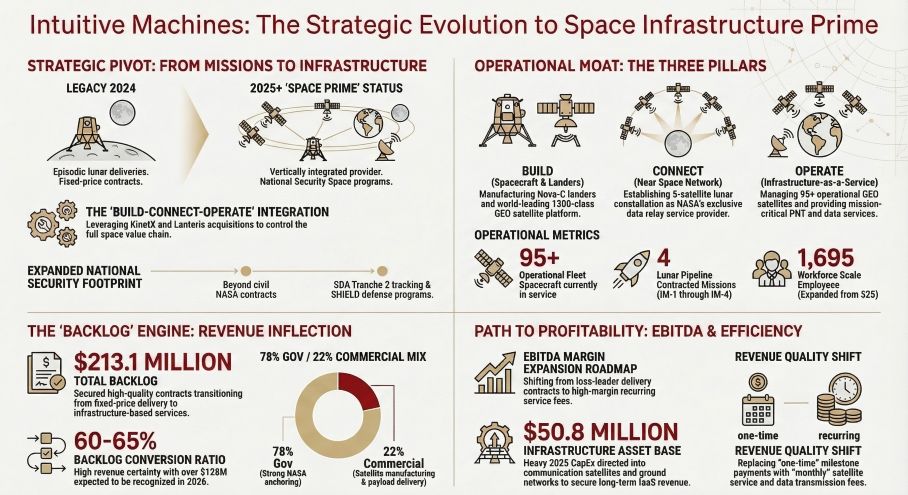

Figure Intuitive Machines: The Strategic Evolution to Space Infrastructure Prime

Strategic Pivots: The "Build-Connect-Operate" Ecosystem

Strategic Pivots: The "Build-Connect-Operate" Ecosystem

The core operational thesis of Intuitive Machines is no longer limited to high-risk, single-mission lander deliveries. The company has explicitly reorganized its capabilities into a "Build-Connect-Operate" framework.

Rather than merely acting as an aerospace manufacturer, IM is building an infrastructure balance sheet. In 2025, the company capitalized $50.8 million in Construction in Progress (CIP) specifically targeted at communications satellites and ground network assets. This capital allocation efficiency signifies a strategic pivot toward generating high-margin, recurring service fees. The acquisition of Lanteris supercharges this transition by integrating the proven 1300-class commercial satellite bus (with over 95 satellites in orbit), allowing IM to shift its revenue recognition from erratic task-jumping to stable, annualized satellite service contracts.

Financial Health & Capital Allocation Efficiency

IM’s 2025 revenue declined by 8% year-over-year, primarily due to the cyclical headwind of NASA canceling the OSAM project, which erased approximately $71.9 million from the OMES III contract. However, the quality of its $213.1 million contract backlog is undergoing a fundamental upgrade. The backlog is highly liquid, with an estimated 60% to 65% expected to convert into revenue within the next 24 months, leaning heavily toward high-certainty projects like the Near Space Network (NSN).

To support its aggressive vertical integration, IM fortified its liquidity through a $175 million private placement and $345 million in convertible notes, leaving it with a robust $582.6 million in cash reserves. However, management's capital allocation efficiency will be rigorously tested. The aggressive scaling of its workforce—from 525 to 1,695 employees following the M&A activities—and the projected non-cash depreciation of its newly capitalized satellite assets will exert short-term pressure on operating margins.

Sector Positioning and Cyclical Headwinds

Within the lunar economy, IM commands a "hub-level" sector positioning. Its near-monopoly status as the sole awardee for NASA's NSN cislunar data relay services establishes a definitive gateway for all future orbital communications.

Despite this unparalleled market share, HDIN Research notes several cyclical headwinds and operational vulnerabilities. IM's customer concentration remains precariously high, with NASA accounting for 78% of 2025 revenue, leaving the firm exposed to federal budget volatility. Furthermore, the company faces severe single-point supply chain bottlenecks—most notably its 100% reliance on SpaceX for launch services. Delays in external launch schedules could trigger cascading deferrals for the IM-3 and IM-4 lunar missions. Additionally, pending Department of Justice (DOJ) reviews regarding Lanteris's cybersecurity compliance under the False Claims Act introduce lingering regulatory risks that require continuous monitoring.

HDIN Viewpoint: The IaaS Turning Point

From an institutional perspective, HDIN Research views 2026 as the definitive turning point for Intuitive Machines' recurring revenue model. The company has successfully completed the metamorphosis from a project-based engineering firm to a space platform operator.

However, investors must exercise caution regarding the accounting dynamics of the company's legacy contracts. Both the IM-3 and IM-4 missions are currently operating in a "loss position," with IM recording a $20.1 million contract loss provision for IM-3 in 2025 alone. This was a calculated strategic loss—management intentionally adjusted the IM-3 schedule to align with the deployment of its proprietary NSN satellites. While this validates IM’s prioritization of long-term network infrastructure over short-term payload milestones, the ultimate test of its sector positioning will be its ability to dilute its reliance on NASA by penetrating the commercial satellite communications market. If commercial IaaS adoption lags, the heavy capital expenditures of 2025 may translate into future asset impairment risks.

Presentation download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Intuitive Machines: The Strategic Evolution to Space Infrastructure Prime

Strategic Pivots: The "Build-Connect-Operate" EcosystemThe core operational thesis of Intuitive Machines is no longer limited to high-risk, single-mission lander deliveries. The company has explicitly reorganized its capabilities into a "Build-Connect-Operate" framework.

Rather than merely acting as an aerospace manufacturer, IM is building an infrastructure balance sheet. In 2025, the company capitalized $50.8 million in Construction in Progress (CIP) specifically targeted at communications satellites and ground network assets. This capital allocation efficiency signifies a strategic pivot toward generating high-margin, recurring service fees. The acquisition of Lanteris supercharges this transition by integrating the proven 1300-class commercial satellite bus (with over 95 satellites in orbit), allowing IM to shift its revenue recognition from erratic task-jumping to stable, annualized satellite service contracts.

Financial Health & Capital Allocation Efficiency

IM’s 2025 revenue declined by 8% year-over-year, primarily due to the cyclical headwind of NASA canceling the OSAM project, which erased approximately $71.9 million from the OMES III contract. However, the quality of its $213.1 million contract backlog is undergoing a fundamental upgrade. The backlog is highly liquid, with an estimated 60% to 65% expected to convert into revenue within the next 24 months, leaning heavily toward high-certainty projects like the Near Space Network (NSN).

To support its aggressive vertical integration, IM fortified its liquidity through a $175 million private placement and $345 million in convertible notes, leaving it with a robust $582.6 million in cash reserves. However, management's capital allocation efficiency will be rigorously tested. The aggressive scaling of its workforce—from 525 to 1,695 employees following the M&A activities—and the projected non-cash depreciation of its newly capitalized satellite assets will exert short-term pressure on operating margins.

Sector Positioning and Cyclical Headwinds

Within the lunar economy, IM commands a "hub-level" sector positioning. Its near-monopoly status as the sole awardee for NASA's NSN cislunar data relay services establishes a definitive gateway for all future orbital communications.

Despite this unparalleled market share, HDIN Research notes several cyclical headwinds and operational vulnerabilities. IM's customer concentration remains precariously high, with NASA accounting for 78% of 2025 revenue, leaving the firm exposed to federal budget volatility. Furthermore, the company faces severe single-point supply chain bottlenecks—most notably its 100% reliance on SpaceX for launch services. Delays in external launch schedules could trigger cascading deferrals for the IM-3 and IM-4 lunar missions. Additionally, pending Department of Justice (DOJ) reviews regarding Lanteris's cybersecurity compliance under the False Claims Act introduce lingering regulatory risks that require continuous monitoring.

HDIN Viewpoint: The IaaS Turning Point

From an institutional perspective, HDIN Research views 2026 as the definitive turning point for Intuitive Machines' recurring revenue model. The company has successfully completed the metamorphosis from a project-based engineering firm to a space platform operator.

However, investors must exercise caution regarding the accounting dynamics of the company's legacy contracts. Both the IM-3 and IM-4 missions are currently operating in a "loss position," with IM recording a $20.1 million contract loss provision for IM-3 in 2025 alone. This was a calculated strategic loss—management intentionally adjusted the IM-3 schedule to align with the deployment of its proprietary NSN satellites. While this validates IM’s prioritization of long-term network infrastructure over short-term payload milestones, the ultimate test of its sector positioning will be its ability to dilute its reliance on NASA by penetrating the commercial satellite communications market. If commercial IaaS adoption lags, the heavy capital expenditures of 2025 may translate into future asset impairment risks.

Presentation download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com