Unitree Robotics at an Inflection Point: Scaling Humanoid AI Amidst Supply Chain and Geopolitical Headwinds

Date : 2026-03-23

Reading : 629

Unitree Robotics has officially crossed the chasm from an agile, R&D-driven startup to a dominant force in the global embodied AI market. In 2025, the company achieved a critical milestone: humanoid robots surpassed quadruped models as the primary growth engine, commanding over 51% of total revenue. However, as Unitree aggressively expands its balance sheet to scale its proprietary UnifoLM AI model, it faces a complex matrix of cyclical headwinds, geopolitical trade barriers, and intellectual property friction.

Based on our deep-dive analysis of Unitree’s financial architecture and operational data, HDIN Research unpacks the strategic implications behind the company's hyper-growth and the underlying "red flags" that institutional investors must monitor.

Figure Unitree Robotics 2025: From Quadruped Pioneer to Global Humanoid Leader

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

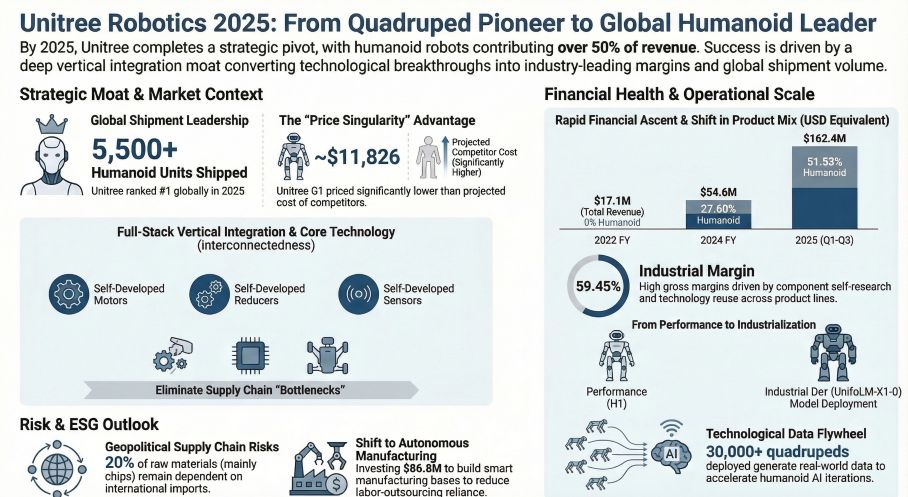

Unitree’s financial trajectory is characterized by explosive top-line growth and a disciplined pivot toward heavy-asset manufacturing. In the first three quarters of 2025, revenue surged by 335% year-over-year. More importantly, the company achieved an elite gross margin of 59.45%. This is not merely a reflection of premium pricing; it is the direct dividend of a vertically integrated supply chain. By engineering 100% of its joint motors and planetary reducers in-house, Unitree has effectively insulated its Bill of Materials (BOM) from third-party markups.

From a capital allocation perspective, Unitree is utilizing its substantial planned IPO capital to fundamentally restructure its operational footprint. The strategic decision to allocate massive capital expenditures (CAPEX) toward a self-owned "smart manufacturing base" signals a definitive end to its reliance on labor outsourcing. While this heavy-asset pivot inherently raises the company's breakeven point, it is a necessary evolution to resolve capacity bottlenecks and support a projected manufacturing scale of tens of thousands of humanoid units by 2027-2028. Furthermore, while the $48.57 million in share-based compensation recorded in 2025 heavily depressed short-term GAAP net profit, it successfully locked in the core R&D talent required to sustain its technological moat.

Strategic Moats & Sector Positioning

Unitree's competitive positioning is anchored by its "hardware-first, ecosystem-locked" commercial loop. The company delivered over 5,500 humanoid robots globally in 2025, claiming the #1 market share position.

The "So What" of this volume lies in the Data Flywheel Effect. Unlike competitors trapped in prolonged laboratory testing or bespoke high-cost models, Unitree utilized its extreme cost-efficiency—pricing the G1 humanoid at a disruptive $11,826—to achieve massive market penetration in academic and early-industrial sectors. Every unit deployed actively feeds real-world, non-structured data back into Unitree’s UnifoLM (World Model-Action/Vision-Language-Action) training architecture. Combined with its unparalleled open-source footprint (over 43 active GitHub projects), Unitree is quietly establishing the default developer ecosystem for the global robotics industry.

Furthermore, its extraordinary Accounts Receivable (AR) turnover rate of 24.03x underscores a definitive "seller's market" advantage. Unitree's ability to mandate pre-payments reflects immense pricing power and deep customer dependency across its global clientele.

Cyclical Headwinds & Geopolitical "Red Flags"

Despite its formidable market positioning, our analysis identifies several critical vulnerabilities that could constrain future margin expansion:

* Supply Chain & Export Control Vulnerabilities: While Unitree excels in mechanical vertical integration, approximately 20% of its raw materials—specifically core high-end electronic components—are imported. With overseas markets historically accounting for over 35% of revenue, the company is acutely exposed to US tariff volatility and the looming threat of being added to restrictive entity lists. A sudden supply chain decoupling could severely disrupt its full-stack manufacturing rhythm.

* Legal "Entanglement" Risks: Continuous, targeted patent infringement litigation (such as the protracted Luweimei disputes) poses a persistent operational distraction. Even with favorable court rulings, "entanglement" litigation can complicate IPO vetting processes and create compliance hurdles for downstream retail channels.

* Data Security & AI Compliance: As embodied AI transitions from controlled labs to dynamic, real-world industrial and consumer environments, Unitree must navigate an increasingly fractured global regulatory landscape regarding geospatial data mapping and privacy compliance.

HDIN Viewpoint: The Institutional Perspective

At HDIN Research, we view Unitree’s current dominance as a triumph of dimensional strategy. Rather than competing purely on absolute physical capabilities against legacy giants, Unitree aggressively optimized the cost-to-performance ratio, effectively creating the "consumer electronics" equivalent of humanoid robotics.

A critical organizational enabler of this agility is the founder's super-voting rights structure (controlling nearly 69% of voting power). This allows the executive team to execute rapid strategic pivots—such as the 9-month product iteration from the H1 to the G1—without yielding to short-term capital market pressures. Moving forward, the ultimate test of Unitree's valuation will not be hardware volume, but the successful standardization and monetization of its industrial-grade AI model, *UnifoLM-X1-0*, on actual factory floors.

Presentation Download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Based on our deep-dive analysis of Unitree’s financial architecture and operational data, HDIN Research unpacks the strategic implications behind the company's hyper-growth and the underlying "red flags" that institutional investors must monitor.

Figure Unitree Robotics 2025: From Quadruped Pioneer to Global Humanoid Leader

Financial Health & Capital Allocation EfficiencyUnitree’s financial trajectory is characterized by explosive top-line growth and a disciplined pivot toward heavy-asset manufacturing. In the first three quarters of 2025, revenue surged by 335% year-over-year. More importantly, the company achieved an elite gross margin of 59.45%. This is not merely a reflection of premium pricing; it is the direct dividend of a vertically integrated supply chain. By engineering 100% of its joint motors and planetary reducers in-house, Unitree has effectively insulated its Bill of Materials (BOM) from third-party markups.

From a capital allocation perspective, Unitree is utilizing its substantial planned IPO capital to fundamentally restructure its operational footprint. The strategic decision to allocate massive capital expenditures (CAPEX) toward a self-owned "smart manufacturing base" signals a definitive end to its reliance on labor outsourcing. While this heavy-asset pivot inherently raises the company's breakeven point, it is a necessary evolution to resolve capacity bottlenecks and support a projected manufacturing scale of tens of thousands of humanoid units by 2027-2028. Furthermore, while the $48.57 million in share-based compensation recorded in 2025 heavily depressed short-term GAAP net profit, it successfully locked in the core R&D talent required to sustain its technological moat.

Strategic Moats & Sector Positioning

Unitree's competitive positioning is anchored by its "hardware-first, ecosystem-locked" commercial loop. The company delivered over 5,500 humanoid robots globally in 2025, claiming the #1 market share position.

The "So What" of this volume lies in the Data Flywheel Effect. Unlike competitors trapped in prolonged laboratory testing or bespoke high-cost models, Unitree utilized its extreme cost-efficiency—pricing the G1 humanoid at a disruptive $11,826—to achieve massive market penetration in academic and early-industrial sectors. Every unit deployed actively feeds real-world, non-structured data back into Unitree’s UnifoLM (World Model-Action/Vision-Language-Action) training architecture. Combined with its unparalleled open-source footprint (over 43 active GitHub projects), Unitree is quietly establishing the default developer ecosystem for the global robotics industry.

Furthermore, its extraordinary Accounts Receivable (AR) turnover rate of 24.03x underscores a definitive "seller's market" advantage. Unitree's ability to mandate pre-payments reflects immense pricing power and deep customer dependency across its global clientele.

Cyclical Headwinds & Geopolitical "Red Flags"

Despite its formidable market positioning, our analysis identifies several critical vulnerabilities that could constrain future margin expansion:

* Supply Chain & Export Control Vulnerabilities: While Unitree excels in mechanical vertical integration, approximately 20% of its raw materials—specifically core high-end electronic components—are imported. With overseas markets historically accounting for over 35% of revenue, the company is acutely exposed to US tariff volatility and the looming threat of being added to restrictive entity lists. A sudden supply chain decoupling could severely disrupt its full-stack manufacturing rhythm.

* Legal "Entanglement" Risks: Continuous, targeted patent infringement litigation (such as the protracted Luweimei disputes) poses a persistent operational distraction. Even with favorable court rulings, "entanglement" litigation can complicate IPO vetting processes and create compliance hurdles for downstream retail channels.

* Data Security & AI Compliance: As embodied AI transitions from controlled labs to dynamic, real-world industrial and consumer environments, Unitree must navigate an increasingly fractured global regulatory landscape regarding geospatial data mapping and privacy compliance.

HDIN Viewpoint: The Institutional Perspective

At HDIN Research, we view Unitree’s current dominance as a triumph of dimensional strategy. Rather than competing purely on absolute physical capabilities against legacy giants, Unitree aggressively optimized the cost-to-performance ratio, effectively creating the "consumer electronics" equivalent of humanoid robotics.

A critical organizational enabler of this agility is the founder's super-voting rights structure (controlling nearly 69% of voting power). This allows the executive team to execute rapid strategic pivots—such as the 9-month product iteration from the H1 to the G1—without yielding to short-term capital market pressures. Moving forward, the ultimate test of Unitree's valuation will not be hardware volume, but the successful standardization and monetization of its industrial-grade AI model, *UnifoLM-X1-0*, on actual factory floors.

Presentation Download:

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com