LivePerson 2025: Strategic Restructuring, Generative AI Moats, and the Liquidity Squeeze

Date : 2026-03-28

Reading : 65

In fiscal year 2025, LivePerson, Inc. (LPSN) executed a drastic corporate restructuring, shedding 35% of its workforce to offset a 22.0% revenue contraction. While this "survival-by-downsizing" strategy successfully narrowed net losses by 50% year-over-year, HDIN Research's latest analysis reveals a precarious balancing act. The company is currently racing to commercialize its Generative AI capabilities before cyclical headwinds, customer attrition, and rigid debt covenants exhaust its financial runway.

Figure LivePerson 2025: Strategic Transformation and Financial Resilience

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

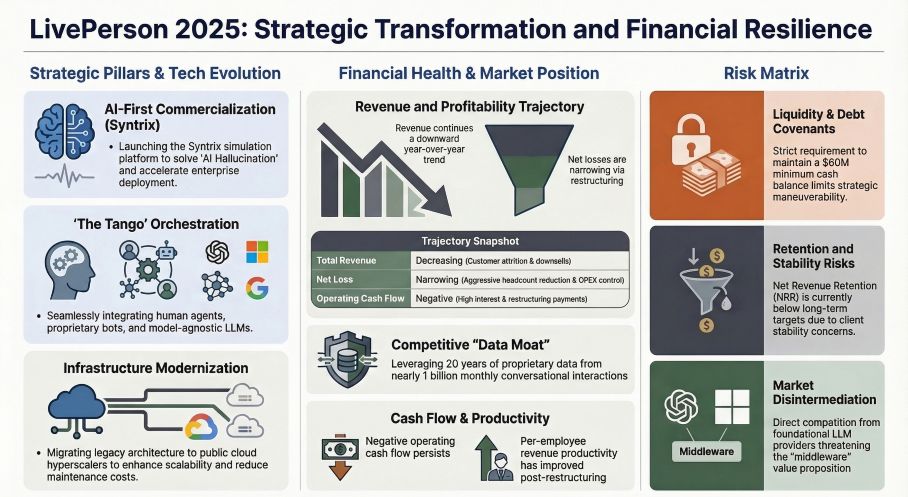

Despite reporting a narrowed net loss of $67.2 million, LivePerson’s bottom-line improvement is heavily distorted by a $27.7 million non-cash gain from a troubled debt restructuring, rather than fundamental operational profitability. Operating cash flow remains in the red, with a $30.4 million net outflow in 2025.

More critically, the company’s capital allocation efficiency is tightly constrained by severe debt covenants. With a mandate to maintain a minimum cash balance of $60 million (excluding 2029 note proceeds) against a total cash reserve of $95 million, LivePerson’s actual discretionary liquidity sits at a highly restrictive $35 million. This tight margin of safety limits the company's ability to aggressively invest in R&D and customer acquisition. Consequently, while total operating expenses were drastically slashed—driving a 20.4% improvement in revenue per employee—the company's "Rule of 40" metric plummeted to a dismal -49.6%, highlighting severe top-line decay and the limitations of cost-cutting as a standalone growth strategy.

Strategic Pivots & Technological Moats

To counter structural revenue declines, LivePerson is accelerating a strategic pivot from traditional seat-based SaaS models toward a consumption- and value-based pricing matrix. The cornerstone of this transition is its Generative AI ecosystem, notably the newly launched *Syntrix* platform—a simulation and evaluation engine designed to eliminate "AI hallucinations" and build trust prior to enterprise deployment.

LivePerson’s true strategic moat lies in its proprietary "The Tango" architecture (seamless human-AI orchestration) and an exclusive data repository of nearly 1 billion monthly conversational interactions spanning two decades. By employing a model-agnostic approach that integrates top-tier Large Language Models (LLMs) from OpenAI, Google, and Microsoft with its proprietary Intent Manager, LivePerson is attempting to embed itself deeply into enterprise workflows via its iHub connectors. Once integrated into enterprise back-end systems like Salesforce, these automated workflows create exceptionally high switching costs.

Industry Outlook & Sector Positioning

The enterprise AI sector is currently experiencing a paradox: high adoption intent coupled with extended procurement cycles due to data privacy and regulatory compliance concerns. LivePerson’s sector positioning reflects this volatility. In FY2025, its Net Revenue Retention (NRR) dropped to an alarming 78% for enterprise and mid-market clients, far below the optimal 105%-115% target. This attrition is primarily driven by counterparty risks—specifically, enterprise clients scaling back renewals or delaying long-term contracts due to concerns over LivePerson’s financial stability.

Geographically, a stark bifurcation has emerged. While the core Americas market contracted by 38.7% due to this crisis of confidence, emerging markets demonstrated resilience. The EMEA and APAC regions grew by 21.4% and 10.6%, respectively, proving that LivePerson's GenAI solutions still command strong market fit where legacy financial reputational damage is less pronounced. However, the overarching threat of disintermediation remains. As native LLM developers enhance their direct-to-enterprise bot capabilities, middleware platforms face intense margin compression.

HDIN Viewpoint

LivePerson is navigating the deepest phase of a restructuring arbitrage. The 2025 fiscal year was an expensive "self-surgery"—excising operational bloat but simultaneously fracturing the revenue base. As an independent market consulting firm, HDIN Research assesses LivePerson’s immediate credit quality as highly vulnerable, bounded by a rigid $60 million liquidity floor and an impending $20.1 million debt maturity in December 2026.

However, from a deep-value perspective, LivePerson retains significant "shell value" as an AI middleware asset. If the company can stabilize its NRR and continue elevating its Average Revenue Per Customer (ARPC)—which organically grew from $625,000 to $680,000 as low-tier clients were shed—its portfolio of 443 patents and exclusive industry data moats could position it as a prime acquisition target. Larger tech conglomerates seeking turnkey, compliant conversational AI infrastructure may find LivePerson's ecosystem highly attractive. The next 12 months will dictate whether LivePerson engineers an organic turnaround or succumbs to strategic industry consolidation.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure LivePerson 2025: Strategic Transformation and Financial Resilience

Financial Health & Capital Allocation EfficiencyDespite reporting a narrowed net loss of $67.2 million, LivePerson’s bottom-line improvement is heavily distorted by a $27.7 million non-cash gain from a troubled debt restructuring, rather than fundamental operational profitability. Operating cash flow remains in the red, with a $30.4 million net outflow in 2025.

More critically, the company’s capital allocation efficiency is tightly constrained by severe debt covenants. With a mandate to maintain a minimum cash balance of $60 million (excluding 2029 note proceeds) against a total cash reserve of $95 million, LivePerson’s actual discretionary liquidity sits at a highly restrictive $35 million. This tight margin of safety limits the company's ability to aggressively invest in R&D and customer acquisition. Consequently, while total operating expenses were drastically slashed—driving a 20.4% improvement in revenue per employee—the company's "Rule of 40" metric plummeted to a dismal -49.6%, highlighting severe top-line decay and the limitations of cost-cutting as a standalone growth strategy.

Strategic Pivots & Technological Moats

To counter structural revenue declines, LivePerson is accelerating a strategic pivot from traditional seat-based SaaS models toward a consumption- and value-based pricing matrix. The cornerstone of this transition is its Generative AI ecosystem, notably the newly launched *Syntrix* platform—a simulation and evaluation engine designed to eliminate "AI hallucinations" and build trust prior to enterprise deployment.

LivePerson’s true strategic moat lies in its proprietary "The Tango" architecture (seamless human-AI orchestration) and an exclusive data repository of nearly 1 billion monthly conversational interactions spanning two decades. By employing a model-agnostic approach that integrates top-tier Large Language Models (LLMs) from OpenAI, Google, and Microsoft with its proprietary Intent Manager, LivePerson is attempting to embed itself deeply into enterprise workflows via its iHub connectors. Once integrated into enterprise back-end systems like Salesforce, these automated workflows create exceptionally high switching costs.

Industry Outlook & Sector Positioning

The enterprise AI sector is currently experiencing a paradox: high adoption intent coupled with extended procurement cycles due to data privacy and regulatory compliance concerns. LivePerson’s sector positioning reflects this volatility. In FY2025, its Net Revenue Retention (NRR) dropped to an alarming 78% for enterprise and mid-market clients, far below the optimal 105%-115% target. This attrition is primarily driven by counterparty risks—specifically, enterprise clients scaling back renewals or delaying long-term contracts due to concerns over LivePerson’s financial stability.

Geographically, a stark bifurcation has emerged. While the core Americas market contracted by 38.7% due to this crisis of confidence, emerging markets demonstrated resilience. The EMEA and APAC regions grew by 21.4% and 10.6%, respectively, proving that LivePerson's GenAI solutions still command strong market fit where legacy financial reputational damage is less pronounced. However, the overarching threat of disintermediation remains. As native LLM developers enhance their direct-to-enterprise bot capabilities, middleware platforms face intense margin compression.

HDIN Viewpoint

LivePerson is navigating the deepest phase of a restructuring arbitrage. The 2025 fiscal year was an expensive "self-surgery"—excising operational bloat but simultaneously fracturing the revenue base. As an independent market consulting firm, HDIN Research assesses LivePerson’s immediate credit quality as highly vulnerable, bounded by a rigid $60 million liquidity floor and an impending $20.1 million debt maturity in December 2026.

However, from a deep-value perspective, LivePerson retains significant "shell value" as an AI middleware asset. If the company can stabilize its NRR and continue elevating its Average Revenue Per Customer (ARPC)—which organically grew from $625,000 to $680,000 as low-tier clients were shed—its portfolio of 443 patents and exclusive industry data moats could position it as a prime acquisition target. Larger tech conglomerates seeking turnkey, compliant conversational AI infrastructure may find LivePerson's ecosystem highly attractive. The next 12 months will dictate whether LivePerson engineers an organic turnaround or succumbs to strategic industry consolidation.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com