Global Semiconductor IP Market 2025: AI, Chiplets, and the Battle for Strategic Moats

Date : 2026-03-26

Reading : 438

In 2025, the global semiconductor Intellectual Property (IP) market has decisively pivoted from a fragmented component-supplier model to a platform-centric ecosystem. Driven by the explosive demand for "Physical AI" and Chiplet architectures, top-tier vendors are aggressively fortifying their technological barriers. However, beneath the surface of soaring gross margins, an exclusive analysis by HDIN Research reveals deep bifurcations in capital allocation efficiency, earnings quality, and exposure to geopolitical headwinds.

Figure 2025 Semiconductor lP Strategic Performance Audit: R&D Efficiency and Market Exposure

Sector Positioning: The AI and Chiplet Paradigm Shift

Sector Positioning: The AI and Chiplet Paradigm Shift

The transition toward Artificial Intelligence (AI) and High-Performance Computing (HPC) has redefined sector positioning. It is no longer about isolated functional blocks; survival now mandates ready-made, full-stack platformization.

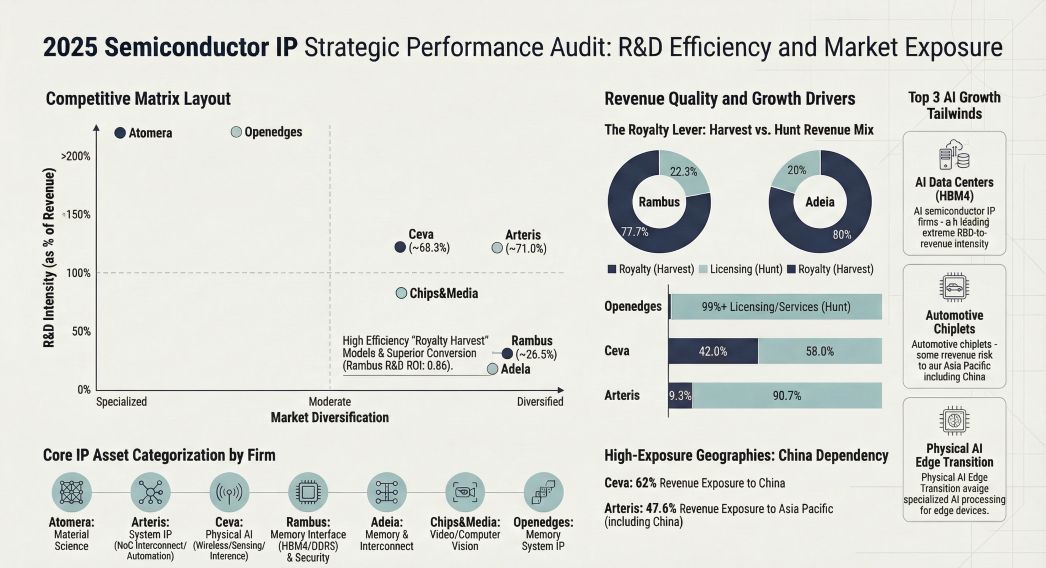

Rambus has successfully leveraged its scale to dominate the AI infrastructure space, with its HBM4, GDDR7, and PCIe 7.0 controllers solving the critical "memory wall" bottleneck for data centers. Conversely, firms like Ceva and Openedges are pushing logic IP to the edge, embedding Neural Processing Units (NPUs) into physical AI architectures. Furthermore, the imperative for Chiplet architectures has elevated interconnect IP to a critical strategic moat. Arteris, through its Next-Gen Network-on-Chip (NoC) technology, has established a formidable ecosystem by deeply integrating with major EDA toolchains (Synopsys, Cadence). This creates exceptionally high technology switching costs; replacing core memory or interconnect subsystems at the RTL stage now risks 12 to 18 months of development delays and millions in mask-retooling costs.

Capital Allocation Efficiency: The R&D ROI Divide

Our analysis of 2025 capital allocation exposes a stark "Pareto Effect" in R&D returns. A clear dividing line exists between companies in the "Royalty Harvest Phase" and those trapped in the "License-Driven Phase."

* High-Conversion Leaders: Rambus demonstrates superior operational efficiency, converting its 26.5% R&D-to-revenue spend into robust product growth with an impressive R&D Return on Investment (ROI) of 0.86. Its deep integration into JEDEC standards allows it to reap long-term standard premiums.

* High-Risk Innovators: Conversely, emerging players are experiencing severe cash burn. Openedges posted a staggering R&D-to-revenue ratio of approximately 237%, heavily betting on 5nm/7nm advanced nodes. Atomera, focusing on MST® material-level IP, presents an even more extreme profile—operating essentially as a high-burn R&D lab with negative gross margins. For these firms, heavy R&D expenditure has yet to cross the chasm into mass-production royalty streams.

Financial Health and Earnings Quality

While semiconductor IP naturally boasts software-like gross margins (often exceeding 80%), true financial health requires rigorous scrutiny of revenue recognition policies and asset valuations.

HDIN Research identifies significant latency and subjectivity risks in current financial reporting. Companies such as Adeia, Ceva, and Rambus frequently utilize point-in-time, upfront revenue recognition for fixed-fee licenses, which can artificially smooth or inflate quarterly milestones. Furthermore, we observe an alarming surge in unbilled receivables and heavy reliance on government R&D subsidies and tax credits (notably for Arteris, Ceva, and Rambus) to mask underlying operational cash flow weaknesses. Finally, aggressive M&A strategies have bloated intangible assets; Adeia's balance sheet, carrying over $300 million in patents and goodwill driven by its litigation-heavy licensing model, is highly vulnerable to impairment if macroeconomic demand softens.

Cyclical Headwinds and Supply Chain Localization

Geopolitical headwinds remain the definitive ceiling on growth. Expanding U.S. export controls targeting advanced compute and supercomputing entities are fracturing the global IP trade.

Firms are responding with divergent localization strategies. Arteris and Chips&Media have established Joint Ventures (JVs) in China to construct compliance firewalls and capture mature-node market share. Meanwhile, Ceva faces acute structural risks, with 62% of its revenue heavily concentrated in the Chinese market without the buffer of a robust localized entity. As hyperscalers (e.g., Google, Amazon) increasingly pivot toward in-housing their custom silicon designs, IP vendors must diversify geographically and technologically to avoid extreme client concentration—a vulnerability starkly illustrated by Atomera, which relies on a single client for 77% of its revenue.

HDIN Viewpoint

The 2025 semiconductor IP sector is undeniably a "winner-takes-all" arena where ecosystem lock-in dictates valuation. HDIN Research cautions strategic decision-makers to look beyond top-line AI buzzwords. Investors and partners must critically assess the true conversion rate of Design-Wins to mass-production variable royalties. Companies heavily reliant on Stock-Based Compensation (SBC) to retain talent, or those inflating margins via aggressive subjective milestone recognition, harbor hidden liquidity risks. Ultimately, vendors capable of delivering end-to-end, foundry-validated Chiplet and HPC platforms—while successfully navigating global trade compliance—will command the pricing power of the next decade.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Semiconductor lP Strategic Performance Audit: R&D Efficiency and Market Exposure

Sector Positioning: The AI and Chiplet Paradigm ShiftThe transition toward Artificial Intelligence (AI) and High-Performance Computing (HPC) has redefined sector positioning. It is no longer about isolated functional blocks; survival now mandates ready-made, full-stack platformization.

Rambus has successfully leveraged its scale to dominate the AI infrastructure space, with its HBM4, GDDR7, and PCIe 7.0 controllers solving the critical "memory wall" bottleneck for data centers. Conversely, firms like Ceva and Openedges are pushing logic IP to the edge, embedding Neural Processing Units (NPUs) into physical AI architectures. Furthermore, the imperative for Chiplet architectures has elevated interconnect IP to a critical strategic moat. Arteris, through its Next-Gen Network-on-Chip (NoC) technology, has established a formidable ecosystem by deeply integrating with major EDA toolchains (Synopsys, Cadence). This creates exceptionally high technology switching costs; replacing core memory or interconnect subsystems at the RTL stage now risks 12 to 18 months of development delays and millions in mask-retooling costs.

Capital Allocation Efficiency: The R&D ROI Divide

Our analysis of 2025 capital allocation exposes a stark "Pareto Effect" in R&D returns. A clear dividing line exists between companies in the "Royalty Harvest Phase" and those trapped in the "License-Driven Phase."

* High-Conversion Leaders: Rambus demonstrates superior operational efficiency, converting its 26.5% R&D-to-revenue spend into robust product growth with an impressive R&D Return on Investment (ROI) of 0.86. Its deep integration into JEDEC standards allows it to reap long-term standard premiums.

* High-Risk Innovators: Conversely, emerging players are experiencing severe cash burn. Openedges posted a staggering R&D-to-revenue ratio of approximately 237%, heavily betting on 5nm/7nm advanced nodes. Atomera, focusing on MST® material-level IP, presents an even more extreme profile—operating essentially as a high-burn R&D lab with negative gross margins. For these firms, heavy R&D expenditure has yet to cross the chasm into mass-production royalty streams.

Financial Health and Earnings Quality

While semiconductor IP naturally boasts software-like gross margins (often exceeding 80%), true financial health requires rigorous scrutiny of revenue recognition policies and asset valuations.

HDIN Research identifies significant latency and subjectivity risks in current financial reporting. Companies such as Adeia, Ceva, and Rambus frequently utilize point-in-time, upfront revenue recognition for fixed-fee licenses, which can artificially smooth or inflate quarterly milestones. Furthermore, we observe an alarming surge in unbilled receivables and heavy reliance on government R&D subsidies and tax credits (notably for Arteris, Ceva, and Rambus) to mask underlying operational cash flow weaknesses. Finally, aggressive M&A strategies have bloated intangible assets; Adeia's balance sheet, carrying over $300 million in patents and goodwill driven by its litigation-heavy licensing model, is highly vulnerable to impairment if macroeconomic demand softens.

Cyclical Headwinds and Supply Chain Localization

Geopolitical headwinds remain the definitive ceiling on growth. Expanding U.S. export controls targeting advanced compute and supercomputing entities are fracturing the global IP trade.

Firms are responding with divergent localization strategies. Arteris and Chips&Media have established Joint Ventures (JVs) in China to construct compliance firewalls and capture mature-node market share. Meanwhile, Ceva faces acute structural risks, with 62% of its revenue heavily concentrated in the Chinese market without the buffer of a robust localized entity. As hyperscalers (e.g., Google, Amazon) increasingly pivot toward in-housing their custom silicon designs, IP vendors must diversify geographically and technologically to avoid extreme client concentration—a vulnerability starkly illustrated by Atomera, which relies on a single client for 77% of its revenue.

HDIN Viewpoint

The 2025 semiconductor IP sector is undeniably a "winner-takes-all" arena where ecosystem lock-in dictates valuation. HDIN Research cautions strategic decision-makers to look beyond top-line AI buzzwords. Investors and partners must critically assess the true conversion rate of Design-Wins to mass-production variable royalties. Companies heavily reliant on Stock-Based Compensation (SBC) to retain talent, or those inflating margins via aggressive subjective milestone recognition, harbor hidden liquidity risks. Ultimately, vendors capable of delivering end-to-end, foundry-validated Chiplet and HPC platforms—while successfully navigating global trade compliance—will command the pricing power of the next decade.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com