The Paradigm Shift in Korean PCBs: AI Substrates, Automotive Pivots, and Capital Efficiency in 2025

Date : 2026-03-25

Reading : 950

The global printed circuit board (PCB) supply chain is undergoing a profound structural transformation. Based on a rigorous audit of the 2025 annual reports from 10 leading Korean PCB manufacturers, HDIN Research has identified a stark industry bifurcation. The era of generic capacity expansion has ended; the market is now dictated by a "process premium." Manufacturers are sharply dividing into two camps: IC substrate leaders capitalizing on the artificial intelligence (AI) infrastructure boom, and Flexible PCB (FPCB) manufacturers aggressively pivoting toward automotive electronics to escape smartphone market stagnation.

For institutional investors and corporate strategists, looking beyond top-line revenue is critical. Beneath the surface, the sector exhibits severe disparities in capital allocation efficiency, cash flow generation, and supply chain resilience.

Figure 2025 South Korean PCB Sector: The Great Transition to Al & Automotive Substrates

Sector Positioning and Strategic Moats

Sector Positioning and Strategic Moats

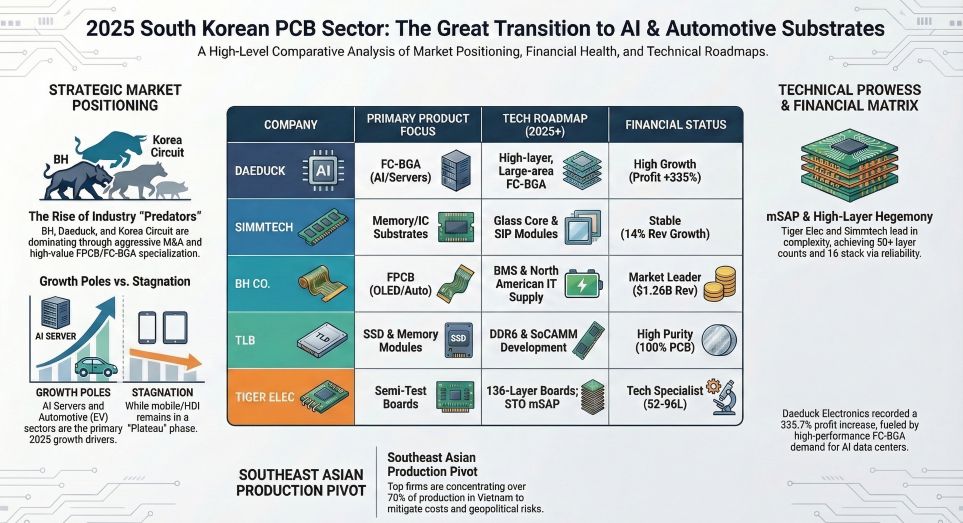

In 2025, pure-play PCB specialization has become a prerequisite for capturing high-margin technological dividends. Companies maintaining near 100% PCB revenue purity, such as Daeduck and Simmtech, are entrenching their strategic moats in the semiconductor packaging space.

* The AI Substrate Dividend: Daeduck is aggressively targeting the Flip Chip Ball Grid Array (FC-BGA) market, essential for AI servers and high-performance computing (HPC). By successfully shifting its product mix toward advanced nodes, Daeduck delivered a staggering 335.7% year-over-year surge in operating profit, effectively neutralizing cyclical headwinds. Similarly, TLB and Korea Circuit are leveraging joint R&D with global memory giants to establish early dominance in next-generation memory standards (SoCAMM and CXL 3.0), creating formidable switching costs for their clients.

* The FPCB Automotive Pivot: For FPCB giants like BH and Newflex, the strategic imperative is securing Tier-1 automotive supplier status. Facing a plateau in mobile devices, these firms are capitalizing on the electrification megatrend. FPCBs are rapidly replacing traditional wire harnesses in Electric Vehicle (EV) Battery Management Systems (BMS), a segment projected to see robust double-digit CAGR. BH has successfully diluted its reliance on mobile displays by generating substantial revenue from automotive components, validating its structural transformation.

Capital Allocation Efficiency and Operational Redirection

A geographic "arms race" for capital expenditure (CAPEX) is fully underway, with Vietnam acting as the indisputable center of gravity for Korean PCB production. However, the efficiency of this capital deployment reveals a tale of two realities.

FPCB manufacturers have achieved remarkable operational leverage through this geographic shift. BH and Newflex are operating their Vietnamese facilities at near-maximum capacity (>90%). Their mature production processes and scale allow them to effectively hedge against raw material inflation and maintain robust margins.

Conversely, IC substrate manufacturers are navigating a costly structural ramp-up phase. Simmtech and TLB are currently operating at roughly 70-75% capacity utilization. This is not indicative of waning demand, but rather the friction associated with upgrading to highly complex manufacturing processes like the Modified Semi-Additive Process (mSAP) and transitioning to high-layer build-up boards. The delayed translation of CAPEX into immediate output underscores the heavy capital burden required to stay relevant in the AI supply chain.

Financial Health and Cyclical Headwinds

While technological advancements paint a bullish long-term picture, the 2025 financial data exposes significant cyclical headwinds and localized financial vulnerabilities.

* Raw Material Inflation: The industry is grappling with severe margin compression due to surging commodity prices. The cost of Potassium Gold Cyanide (PGC)—crucial for surface plating—spiked by 53.7% in 2025, while Copper Clad Laminate (CCL) prices remain elevated due to upstream supply constraints. Furthermore, the industry remains dangerously reliant on a single dominant supplier, Doosan, for high-end CCL materials, presenting a systemic bottleneck.

* Cash Flow vs. Paper Profit: A critical divergence exists in earnings quality. BH exhibits a "high-carat" financial profile, generating robust operating cash flows from its legacy FPCB business to self-fund its EV expansion. In stark contrast, Simmtech triggers a red flag: despite its technological leadership, the company posted a massive negative operating cash flow of -$113.45 million. This indicates that its bottom-line losses are not merely non-cash depreciation, but an actual, severe liquidity drain driven by relentless R&D and equipment requirements.

* The Rigid PCB Value Trap: Manufacturers trapped in the low-end rigid board market, such as Finecircuit, are facing existential threats. Lacking the pricing power to pass inflated copper costs onto their home appliance clients, these firms suffered devastating profit declines and massive forecast misses, signaling a high risk of impending asset impairments.

HDIN Viewpoint: Navigating the 2026 Horizon

From the perspective of HDIN Research, the Korean PCB sector is transitioning from a volume-driven market to an oligopoly of precision engineering. We advise institutional investors to maintain a structural overweight on AI-infrastructure beneficiaries (like Daeduck) and successful EV pivoters, while strictly avoiding the value traps of legacy rigid board manufacturers.

However, an audit-level skepticism is required when assessing the financial health of high-end substrate makers. To smooth earnings amid heavy capital cycles, some premium manufacturers have aggressively extended equipment depreciation schedules to 10 years (compared to the industry standard of 5 years). In an environment where AI and GDDR7 technologies iterate at breakneck speed, this accounting maneuver risks creating a delayed "impairment storm."

Finally, geopolitical supply chain configuration remains the ultimate wildcard. With critical production nodes heavily concentrated in Vietnam, and material sales distribution deeply intertwined with Mainland China and Taiwan, Province of China, any geopolitical friction could rapidly transform current operational leverage into a severe supply chain liability.

Presentation Download & Media Access

To dive deeper into the financial models, capacity utilization matrices, and supply chain dependency charts of the top 10 Korean PCB manufacturers:

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

For institutional investors and corporate strategists, looking beyond top-line revenue is critical. Beneath the surface, the sector exhibits severe disparities in capital allocation efficiency, cash flow generation, and supply chain resilience.

Figure 2025 South Korean PCB Sector: The Great Transition to Al & Automotive Substrates

Sector Positioning and Strategic MoatsIn 2025, pure-play PCB specialization has become a prerequisite for capturing high-margin technological dividends. Companies maintaining near 100% PCB revenue purity, such as Daeduck and Simmtech, are entrenching their strategic moats in the semiconductor packaging space.

* The AI Substrate Dividend: Daeduck is aggressively targeting the Flip Chip Ball Grid Array (FC-BGA) market, essential for AI servers and high-performance computing (HPC). By successfully shifting its product mix toward advanced nodes, Daeduck delivered a staggering 335.7% year-over-year surge in operating profit, effectively neutralizing cyclical headwinds. Similarly, TLB and Korea Circuit are leveraging joint R&D with global memory giants to establish early dominance in next-generation memory standards (SoCAMM and CXL 3.0), creating formidable switching costs for their clients.

* The FPCB Automotive Pivot: For FPCB giants like BH and Newflex, the strategic imperative is securing Tier-1 automotive supplier status. Facing a plateau in mobile devices, these firms are capitalizing on the electrification megatrend. FPCBs are rapidly replacing traditional wire harnesses in Electric Vehicle (EV) Battery Management Systems (BMS), a segment projected to see robust double-digit CAGR. BH has successfully diluted its reliance on mobile displays by generating substantial revenue from automotive components, validating its structural transformation.

Capital Allocation Efficiency and Operational Redirection

A geographic "arms race" for capital expenditure (CAPEX) is fully underway, with Vietnam acting as the indisputable center of gravity for Korean PCB production. However, the efficiency of this capital deployment reveals a tale of two realities.

FPCB manufacturers have achieved remarkable operational leverage through this geographic shift. BH and Newflex are operating their Vietnamese facilities at near-maximum capacity (>90%). Their mature production processes and scale allow them to effectively hedge against raw material inflation and maintain robust margins.

Conversely, IC substrate manufacturers are navigating a costly structural ramp-up phase. Simmtech and TLB are currently operating at roughly 70-75% capacity utilization. This is not indicative of waning demand, but rather the friction associated with upgrading to highly complex manufacturing processes like the Modified Semi-Additive Process (mSAP) and transitioning to high-layer build-up boards. The delayed translation of CAPEX into immediate output underscores the heavy capital burden required to stay relevant in the AI supply chain.

Financial Health and Cyclical Headwinds

While technological advancements paint a bullish long-term picture, the 2025 financial data exposes significant cyclical headwinds and localized financial vulnerabilities.

* Raw Material Inflation: The industry is grappling with severe margin compression due to surging commodity prices. The cost of Potassium Gold Cyanide (PGC)—crucial for surface plating—spiked by 53.7% in 2025, while Copper Clad Laminate (CCL) prices remain elevated due to upstream supply constraints. Furthermore, the industry remains dangerously reliant on a single dominant supplier, Doosan, for high-end CCL materials, presenting a systemic bottleneck.

* Cash Flow vs. Paper Profit: A critical divergence exists in earnings quality. BH exhibits a "high-carat" financial profile, generating robust operating cash flows from its legacy FPCB business to self-fund its EV expansion. In stark contrast, Simmtech triggers a red flag: despite its technological leadership, the company posted a massive negative operating cash flow of -$113.45 million. This indicates that its bottom-line losses are not merely non-cash depreciation, but an actual, severe liquidity drain driven by relentless R&D and equipment requirements.

* The Rigid PCB Value Trap: Manufacturers trapped in the low-end rigid board market, such as Finecircuit, are facing existential threats. Lacking the pricing power to pass inflated copper costs onto their home appliance clients, these firms suffered devastating profit declines and massive forecast misses, signaling a high risk of impending asset impairments.

HDIN Viewpoint: Navigating the 2026 Horizon

From the perspective of HDIN Research, the Korean PCB sector is transitioning from a volume-driven market to an oligopoly of precision engineering. We advise institutional investors to maintain a structural overweight on AI-infrastructure beneficiaries (like Daeduck) and successful EV pivoters, while strictly avoiding the value traps of legacy rigid board manufacturers.

However, an audit-level skepticism is required when assessing the financial health of high-end substrate makers. To smooth earnings amid heavy capital cycles, some premium manufacturers have aggressively extended equipment depreciation schedules to 10 years (compared to the industry standard of 5 years). In an environment where AI and GDDR7 technologies iterate at breakneck speed, this accounting maneuver risks creating a delayed "impairment storm."

Finally, geopolitical supply chain configuration remains the ultimate wildcard. With critical production nodes heavily concentrated in Vietnam, and material sales distribution deeply intertwined with Mainland China and Taiwan, Province of China, any geopolitical friction could rapidly transform current operational leverage into a severe supply chain liability.

Presentation Download & Media Access

To dive deeper into the financial models, capacity utilization matrices, and supply chain dependency charts of the top 10 Korean PCB manufacturers:

* Click the PDF download link under “Related Topics” to access the presentation of this report.

* Click this link to watch the YouTube video.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com