The Great Bifurcation: Structural Shifts and Strategic Moats in the 2025 LED Chip Market

Date : 2026-03-25

Reading : 177

The 2025 global LED chip industry is undergoing a ruthless bifurcation, characterized by structural prosperity in niche applications and cyclical headwinds in legacy markets. As traditional general lighting falls victim to price wars and stagnant demand, the battleground has decisively shifted toward high-margin arenas: Mini/Micro LED displays, automotive photonics, and invisible light applications (UV/VCSEL).

Based on HDIN Research’s proprietary financial and operational analysis of three industry bellwethers—Seoul Viosys (SVC), BOE HC SemiTek (HCS), and Focus Lightings (FLT)—it is evident that mere capacity expansion is no longer a viable strategy. Instead, proprietary ecosystems, extreme capital allocation efficiency, and advanced material science are dictating sector leadership.

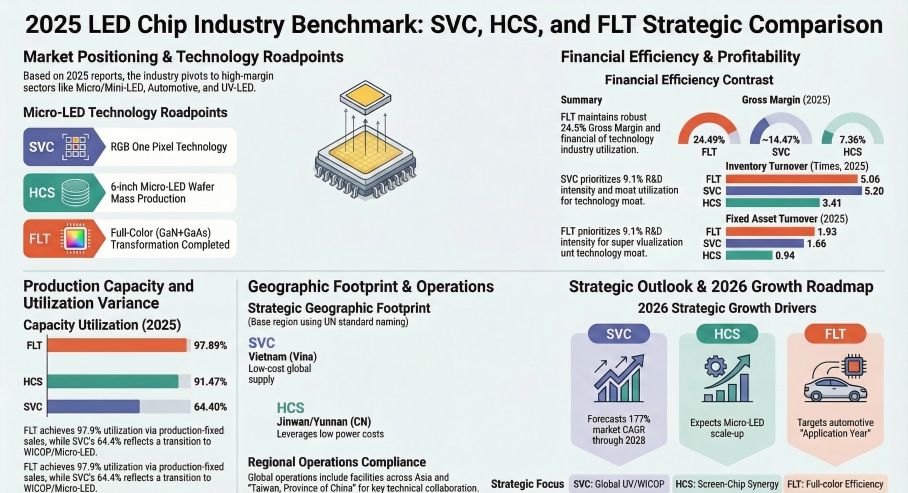

Figure 2025 LED Chip Industry Benchmark: SVC, HCS, and FLT Strategic Comparison

Financial Health and Capital Allocation Efficiency

Financial Health and Capital Allocation Efficiency

A granular look at the fiscal architectures of these three giants reveals starkly divergent capital allocation efficiencies and earnings quality:

* Focus Lightings (FLT) – The Efficiency Play with a Caveat: FLT demonstrates exceptional operational agility, maintaining a near-maximum capacity utilization rate of 97.89% and superior inventory turnover. The company boasts the highest profit quality among the trio, driven by a robust operating cash flow that covers net income by a 2.57x multiple. However, HDIN Research urges analytical prudence: approximately 55% of FLT’s 2025 revenue stems from low-margin precious metal scrap recycling. Stripping out this non-core segment reveals a much leaner semiconductor manufacturing footprint.

* BOE HC SemiTek (HCS) – Heavy CAPEX and Depreciation Drag: While HCS commands the largest consolidated revenue footprint ($752.42M), it is currently navigating severe financial strain. Massive capital expenditures into 6-inch Micro LED wafer fabs (e.g., the Jinwan project) have depressed its fixed asset turnover to 0.94. Consequently, the company is absorbing heavy depreciation and negative operating cash flows. Furthermore, an aggressive 49.29% R&D capitalization rate and high reliance on government subsidies obscure its true organic profitability.

* Seoul Viosys (SVC) – Deep Moats, Immediate Pressures: SVC represents the classic innovator's dilemma. While the company maintains a highly efficient inventory turnover rate (5.20), it remains unprofitable at the net income level as it funds an aggressive R&D pipeline to transition away from traditional packaging to next-generation WICOP (Wafer Level Integrated Chip on PCB) technology.

Strategic Moats and Sector Positioning

To insulate themselves from the "strong supply, weak demand" macro environment, each company is carving out distinct strategic moats:

* Vertical Ecosystem Integration (HCS): Post-acquisition by BOE, HCS has transitioned into a captive market engine. This "Screen-Chip Integration" provides HCS with high demand certainty, allowing it to bypass broader market volatility. With its 6-inch Micro LED lines directly feeding BOE’s display empire, HCS is sacrificing short-term independent margins for long-term ecosystem lock-in.

* Technological Premium & IP Barriers (SVC): SVC’s competitive moat is built on a formidable portfolio of over 7,000 patents covering the full 200nm-1600nm spectrum. By dominating the UV LED and automotive VCSEL markets, SVC successfully evades the commoditization of visible light chips. Its WICOP technology, now integrated into over 100 global automotive models, structurally reduces downstream assembly costs, granting SVC superior pricing power.

* Full-Spectrum Agility (FLT): Operating without the safety net of a conglomerate, FLT relies on hyperspeed market responsiveness. By aggressively expanding into GaAs-based red and yellow MOCVD lines in 2025, FLT has completed its transformation into a full-color supplier. This allows the company to capture counter-cyclical growth in high-yield niches like plant lighting and smart cabin displays.

Cyclical Headwinds and Supply Chain Resilience

The 2025 landscape is fraught with non-financial operating risks. A universal headwind is the surging cost of precious metals (particularly gold), which has aggressively compressed gross margins across the board.

Simultaneously, geopolitical trade barriers are accelerating supply chain decoupling. Chinese manufacturers (HCS and FLT) are aggressively pushing for domestic substitution of critical MOCVD equipment to secure capacity. Conversely, SVC is leveraging its decentralized global footprint—including highly cost-effective manufacturing hubs in Vietnam—to bypass tariff walls and mitigate regional policy risks.

HDIN Viewpoint

At HDIN Research, we assess that the era of scaling standard LED wafers for market share is permanently over. The future belongs to players who can execute a "Patent + Material Science + Downstream Integration" matrix.

Investors must look beyond top-line revenue growth. FLT offers high capital efficiency, but its supply chain risk is heavily skewed by its recycling dependencies. HCS is executing a masterclass in vertical integration, though its current valuation requires high tolerance for short-term earnings dilution and subsidy reliance. Ultimately, structural winners will be those who successfully commercialize Micro LED and automotive photonics while maintaining rigorous cash flow discipline amidst raw material inflation.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Based on HDIN Research’s proprietary financial and operational analysis of three industry bellwethers—Seoul Viosys (SVC), BOE HC SemiTek (HCS), and Focus Lightings (FLT)—it is evident that mere capacity expansion is no longer a viable strategy. Instead, proprietary ecosystems, extreme capital allocation efficiency, and advanced material science are dictating sector leadership.

Figure 2025 LED Chip Industry Benchmark: SVC, HCS, and FLT Strategic Comparison

Financial Health and Capital Allocation EfficiencyA granular look at the fiscal architectures of these three giants reveals starkly divergent capital allocation efficiencies and earnings quality:

* Focus Lightings (FLT) – The Efficiency Play with a Caveat: FLT demonstrates exceptional operational agility, maintaining a near-maximum capacity utilization rate of 97.89% and superior inventory turnover. The company boasts the highest profit quality among the trio, driven by a robust operating cash flow that covers net income by a 2.57x multiple. However, HDIN Research urges analytical prudence: approximately 55% of FLT’s 2025 revenue stems from low-margin precious metal scrap recycling. Stripping out this non-core segment reveals a much leaner semiconductor manufacturing footprint.

* BOE HC SemiTek (HCS) – Heavy CAPEX and Depreciation Drag: While HCS commands the largest consolidated revenue footprint ($752.42M), it is currently navigating severe financial strain. Massive capital expenditures into 6-inch Micro LED wafer fabs (e.g., the Jinwan project) have depressed its fixed asset turnover to 0.94. Consequently, the company is absorbing heavy depreciation and negative operating cash flows. Furthermore, an aggressive 49.29% R&D capitalization rate and high reliance on government subsidies obscure its true organic profitability.

* Seoul Viosys (SVC) – Deep Moats, Immediate Pressures: SVC represents the classic innovator's dilemma. While the company maintains a highly efficient inventory turnover rate (5.20), it remains unprofitable at the net income level as it funds an aggressive R&D pipeline to transition away from traditional packaging to next-generation WICOP (Wafer Level Integrated Chip on PCB) technology.

Strategic Moats and Sector Positioning

To insulate themselves from the "strong supply, weak demand" macro environment, each company is carving out distinct strategic moats:

* Vertical Ecosystem Integration (HCS): Post-acquisition by BOE, HCS has transitioned into a captive market engine. This "Screen-Chip Integration" provides HCS with high demand certainty, allowing it to bypass broader market volatility. With its 6-inch Micro LED lines directly feeding BOE’s display empire, HCS is sacrificing short-term independent margins for long-term ecosystem lock-in.

* Technological Premium & IP Barriers (SVC): SVC’s competitive moat is built on a formidable portfolio of over 7,000 patents covering the full 200nm-1600nm spectrum. By dominating the UV LED and automotive VCSEL markets, SVC successfully evades the commoditization of visible light chips. Its WICOP technology, now integrated into over 100 global automotive models, structurally reduces downstream assembly costs, granting SVC superior pricing power.

* Full-Spectrum Agility (FLT): Operating without the safety net of a conglomerate, FLT relies on hyperspeed market responsiveness. By aggressively expanding into GaAs-based red and yellow MOCVD lines in 2025, FLT has completed its transformation into a full-color supplier. This allows the company to capture counter-cyclical growth in high-yield niches like plant lighting and smart cabin displays.

Cyclical Headwinds and Supply Chain Resilience

The 2025 landscape is fraught with non-financial operating risks. A universal headwind is the surging cost of precious metals (particularly gold), which has aggressively compressed gross margins across the board.

Simultaneously, geopolitical trade barriers are accelerating supply chain decoupling. Chinese manufacturers (HCS and FLT) are aggressively pushing for domestic substitution of critical MOCVD equipment to secure capacity. Conversely, SVC is leveraging its decentralized global footprint—including highly cost-effective manufacturing hubs in Vietnam—to bypass tariff walls and mitigate regional policy risks.

HDIN Viewpoint

At HDIN Research, we assess that the era of scaling standard LED wafers for market share is permanently over. The future belongs to players who can execute a "Patent + Material Science + Downstream Integration" matrix.

Investors must look beyond top-line revenue growth. FLT offers high capital efficiency, but its supply chain risk is heavily skewed by its recycling dependencies. HCS is executing a masterclass in vertical integration, though its current valuation requires high tolerance for short-term earnings dilution and subsidy reliance. Ultimately, structural winners will be those who successfully commercialize Micro LED and automotive photonics while maintaining rigorous cash flow discipline amidst raw material inflation.

Presentation Download & Media Access

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click this link to watch the YouTube video.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com